Shares of Tyson Foods, Inc. (NYSE: TSN) stayed green on Wednesday. The stock has dropped 3% over the past three months. The food company is slated to report its first quarter 2025 earnings results on Monday, February 3, before market opens. Here’s a look at what to expect from the earnings report:

Revenue

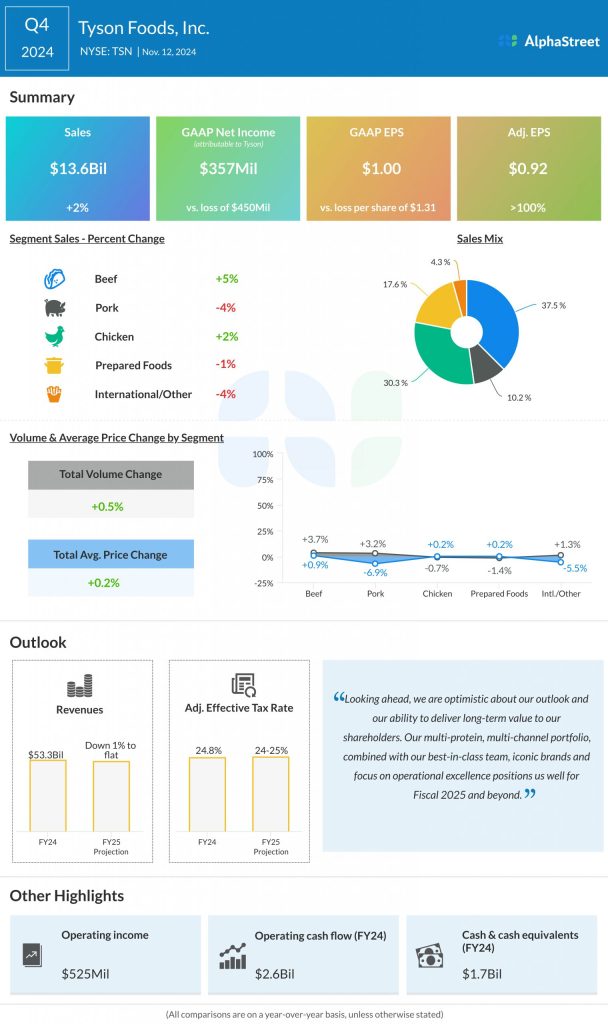

Analysts are projecting revenue of $13.46 billion for Tyson in the first quarter of 2025. This indicates a rise of 1% from the same period a year ago. In the fourth quarter of 2024, sales increased around 2% year-over-year to $13.56 billion.

Earnings

The consensus estimate for earnings in Q1 2025 is $0.88 per share, which compares to adjusted EPS of $0.69 reported in Q1 2024. In Q4 2024, adjusted EPS more than doubled YoY to $0.92.

Points to note

Tyson is expected to benefit from its multi-protein, multi-channel portfolio and the strength of its brands. The company is working on expanding household penetration and market opportunities through brand-building investments and product innovation. It is also working on expanding distribution for its top-performing products. These efforts are expected to yield benefits.

In Q4, sales growth was driven mainly by the beef and chicken segments. Chicken saw sales growth despite a slight drop in volume. The segment also recorded significant profit growth. Sales growth in Beef was driven mainly by volume but profits declined due to compressed spreads.

The Prepared Foods segment was impacted by lower retail volume but volumes outside of retail are seeing growth. Lower raw material costs and operational efficiencies have helped drive profits in this segment. The Pork segment saw revenues drop due to lower pricing, even as volumes increased. Improved operational execution helped drive a rise in profits for this division.

The company’s efforts in modernizing operations, generating cost savings, and building its digital capabilities are expected help drive efficiencies and growth.