Yum! Brands, Inc. (NYSE: YUM) owns some of the most popular food brands and serves customers in almost every part of the world. Over the years, the company’s leading segments of KFC, Pizza Hut, and Taco Bell have thrived on the global scale of the business and extensive franchise network. The brand power also enabled Yum! Brands to stay broadly unaffected by the COVID-related restrictions, thanks to the widespread adoption of its digital platform.

The Stock

In the first half of the year, the effects of the market selloff were felt in the performance of YUM also, which maintained a downtrend after peaking in the final weeks of 2021. The weakness also reflects investors’ concerns over the company’s not-so-impressive earnings performance in the last few quarters – three misses in a row.

YUM! Brands Q2 2022 Earnings Call Transcript

To some extent, the top line faces pressure from the company’s exit from the Russian market, in response to the political tension in the region, and the continued slowdown in China where pandemic restrictions are still in place. While it is advisable to stay alert to the short-term risks, YUM’s past performance shows it has always rewarded long-term investors. Considering the rapid improvement in the COVID situation and the company’s competitive dividend, it would a good idea to buy the stock now and hold it forever.

From Yum! Brands’ Q2 2022 earnings conference call:

“We’re pleased with the continued growth in our digital business with sales of nearly $6 billion, fueled by the adoption of our global platforms and capabilities. Our unmatched global scale and digital capabilities are key differentiators in the restaurant industry, and these competitive advantages enable us to thrive in any environment… As Yum China shared on its earnings call last week, COVID-related restrictions continued throughout the quarter, significantly impacting second-quarter results.”

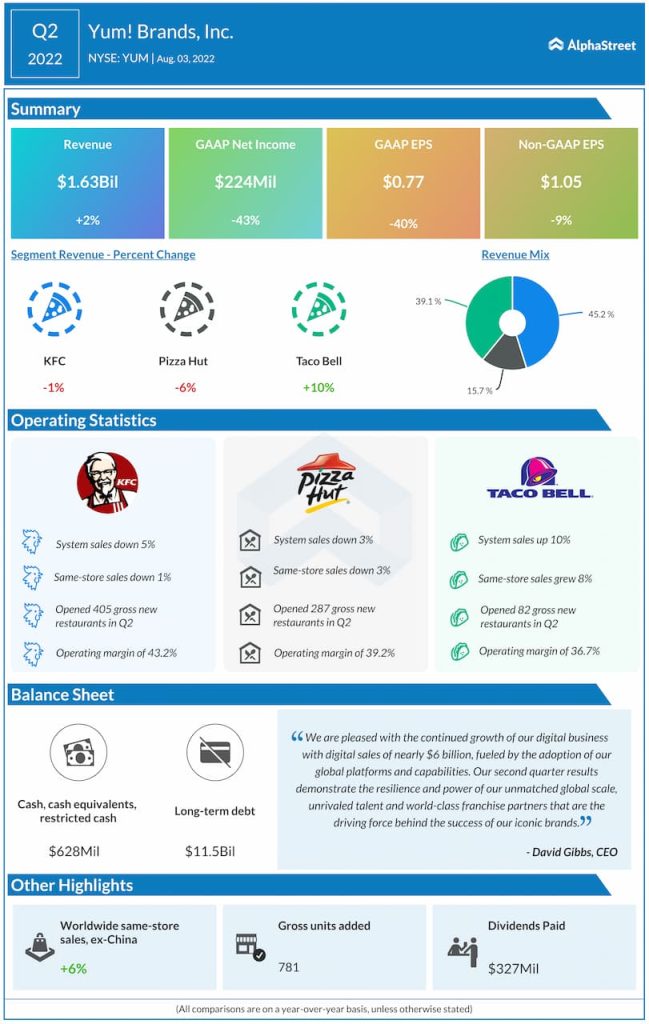

Financial Performance

In what could be a trend reversal, Yum! Brands’ earnings missed estimates for three consecutive quarters after beating regularly in the trailing quarters. The revenue performance was not much different from the bottom-line trend. However, it is estimated that the continuing adoption of the company’s digital platform and expansion of the store network would ease the strain on sales.

In the second quarter, an increase in sales at Taco Bell outlets more than offset weakness in the KFC and Pizza Hut brands. As a result, total revenues moved up 2% to about $1.63 billion. Meanwhile, adjusted earnings decreased 9% annually to $1.05 per share. The top line came in line with the market’s projection while earnings fell short of expectations.

MCD Earnings: McDonald’s comp sales up 10% in Q2; earnings beat

Yum! Brands’ stock has mostly traded below its 52-week average in recent months, all along experiencing volatility. The shares ended the last trading session lower, extending their recent weakness.