Shares of Dollar General Corporation (NYSE: DG) fell over 1% on Tuesday. The stock has dropped 11% over the past three months. The discount store chain saw sales increase year-over-year in the first quarter of 2024, helped by growth in customer traffic and strength in consumables. At the same time, the discretionary category continues to see pressure and shrink remains a significant headwind to margins.

Search for value

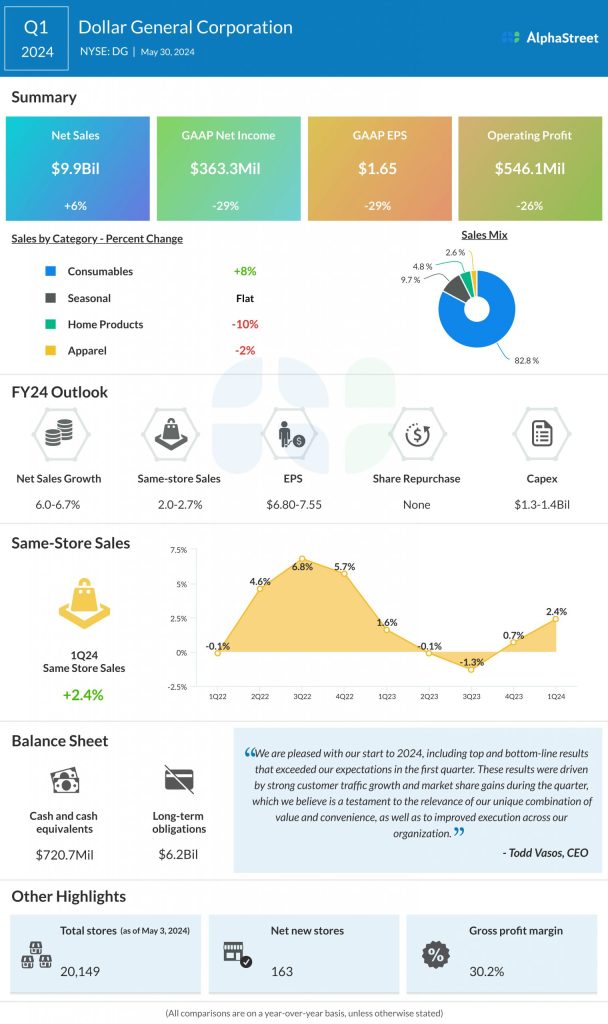

Dollar General’s net sales grew 6.1% to $9.9 billion in the first quarter of 2024 compared to the same period a year ago, as the company saw accelerated market share growth in both dollars and units in the consumables category as well as market share growth in dollars in non-consumables.

Same-store sales grew 2.4% in the quarter, helped by a growth of more than 4% in customer traffic, but this was partly offset by a drop in average transaction amount, driven mainly by fewer items per basket. Robust gains in the consumables category was the sole driver of comp sales growth but this momentum was partly offset by continued softness in the discretionary category.

As mentioned on the company’s quarterly conference call, consumers continue to seek value in their purchases as they lean more towards private brands and pick up items that are at or below the $1 price point. There is also more demand for discounted items. Looking ahead, consumers are expected to be price sensitive throughout the year and give utmost importance to value with regards to their purchases.

Shrink – a persistent challenge

Dollar General’s earnings declined 29.5% to $1.65 in Q1 2024. Gross margin decreased 145 basis points to 30.2%, due to higher levels of shrink, higher discounts, consumables accounting for a larger part of sales, and lower inventory mark-ups.

Shrink remains a significant challenge for the company and it is implementing several measures across its supply chain, merchandising, and within stores to tackle this issue. These include reducing the amount of inventory carried, removing high-shrink SKUs, and eliminating self-checkout in most of its stores.

The retailer has converted around 12,000 stores away from self-checkout thus far. It anticipates this action will help bring forth a reduction in shrink during the second half of 2024 with a more material positive impact in 2025. Moving forward, it plans to limit the self-checkout option to just a few stores that have higher volume and are in low-shrink locations.

More store remodels

On its call, Dollar General said it updated the plans for its real estate projects in 2024. The company now expects to remodel around 1,620 stores during the year versus its previous expectation of 1,500 remodels. It is also reducing the planned number of its new stores to 730 from 800. It expects to relocate 85 stores. This brings its total real estate project count to around 2,435 from the previous number of 2,385.

Outlook

Dollar General expects to see higher pressure from sales mix, discounts and shrink in 2024. For the second quarter of 2024, the company expects comp sales to increase in the low 2% range and EPS to be approx. $1.70-1.85.

For the full year, net sales are expected to grow around 6.0-6.7%. Same-store sales are expected to grow 2.0-2.7%. EPS is expected to range between $6.80-7.55.