Shares of Macy’s, Inc. (NYSE: M) were up over 1% on Friday. The stock has gained 9% over the past one month. Earlier this week, the retailer delivered first quarter 2024 earnings results that were down from the year-ago period but still better than expected. Despite operating in a dynamic economic environment, the company remains optimistic on driving growth as it continues to execute its Bold New Chapter strategy.

Tough macro climate

As mentioned on its quarterly conference call, Macy’s customers across all nameplates are benefiting from strong wage and job growth but persistent inflationary pressures are weighing on them. For this reason, the company believes its customers will continue to remain cautious with regards to their discretionary spending.

Bold New Chapter

Macy’s Bold New Chapter strategy has three pillars – strengthen the Macy’s nameplate, accelerate luxury growth, and simplify and modernize end-to-end operations. On its call, the company said that it is on or ahead of plan across all three pillars.

Macy’s is working on consolidating capacity, increasing automation, and reducing costs across its network. At its Macy’s nameplate, comparable sales were down 0.4% on an owned-plus-licensed-plus-marketplace basis in the first quarter. Go-forward locations comparable sales were up 0.1% on an owned-plus-licensed basis. The first 50 locations comparable sales were up 3.4% on an owned-plus-licensed basis.

The company has been gaining positive response to its omnichannel initiatives at the Macy’s nameplate. In addition, full price and planned promotional sell-throughs of new and expanded assortments have been strong.

As stated on the quarterly call, the company’s private brand apparel initiative is moving forward as planned, with the completion of the majority of brand exits and the launch of several new ones. In the near term, private brand sales volumes are expected to be lower than historic levels and then to see a pickup later in the year.

In luxury, Bloomingdale’s comparable sales were up 0.3% on an owned-plus-licensed-plus-marketplace basis, and Bluemercury comparable sales were up 4.3% on an owned basis in Q1. The company is seeing strength in the apparel and beauty categories at these nameplates.

Q1 results

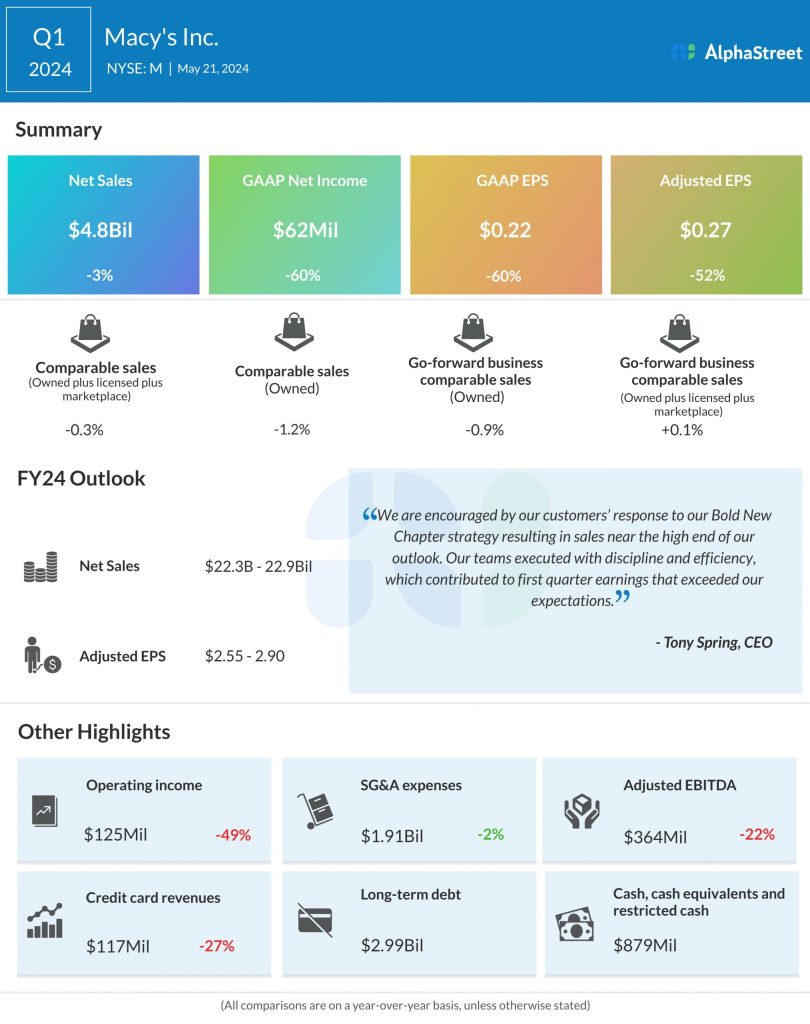

In the first quarter of 2024, Macy’s net sales decreased 2.7% year-over-year to $4.85 billion. Comparable sales were down 1.2% on an owned basis and down 0.3% on an owned-plus-licensed-plus-marketplace basis. Adjusted EPS declined 52% to $0.27.

Outlook

For the second quarter of 2024, Macy’s expects net sales in the range of $4.97 billion to $5.1 billion. Adjusted EPS is expected to be $0.25-0.33. For the full year of 2024, net sales are projected to be $22.3-22.9 billion and adjusted EPS is expected to be $2.55-2.90.