Shares of Alaska Air Group (NYSE: ALK) plunged 10% on Tuesday after the company reported its second quarter 2023 earnings results. Although the airliner beat revenue and earnings estimates, the Street was not impressed with its revenue guidance for the third quarter. Here’s a look at Alaska’s expectations for the near term:

Revenue

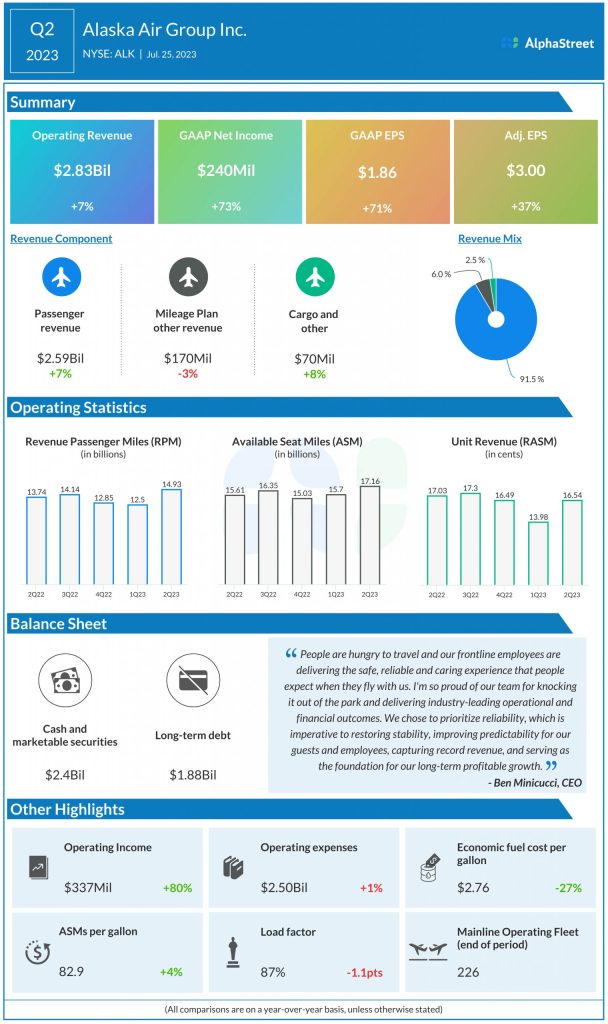

Alaska’s total operating revenue in Q2 2023 increased 7% year-over-year to $2.83 billion, beating estimates of $2.77 billion. For the third quarter of 2023, the company expects total revenue to be flat to up 3% compared to the prior-year period. For the full year of 2023, total revenue is estimated to grow 8-10% year-over-year.

Earnings

In Q2, Alaska’s GAAP net income grew over 70% to $240 million, or $1.86 per share, compared to last year. Adjusted EPS rose 37% to $3.00, surpassing projections of $2.68. For full-year 2023, EPS is expected to range between $5.50-7.50.

Costs

In Q2 2023, cost per available seat mile, excluding fuel and special items, (CASMex) was up 2% year-over-year. For Q3 2023, CASM-ex is expected to be down 0-2% YoY. For FY2023, CASMex is expected to be down 1-3% YoY. Economic fuel cost per gallon is estimated to be $2.70-2.80 in Q3.

Other metrics

Alaska expects adjusted pre-tax margin to range between 14-16% in Q3 2023 and 9-12% for FY2023. Capacity is estimated to be up 10-13% in Q3 and up 11-13% in FY2023. Capital expenditures are estimated to be around $1.8 billion for FY2023.