Shares of Alaska Air Group Inc. (NYSE: ALK) were up 3% on Monday. The stock has dropped 18% year-to-date and 21% over the past 12 months. Last week, the airline reported its third quarter 2022 earnings results which beat expectations. Here’s a look at Alaska’s expectations for the rest of the year:

Revenue and profitability

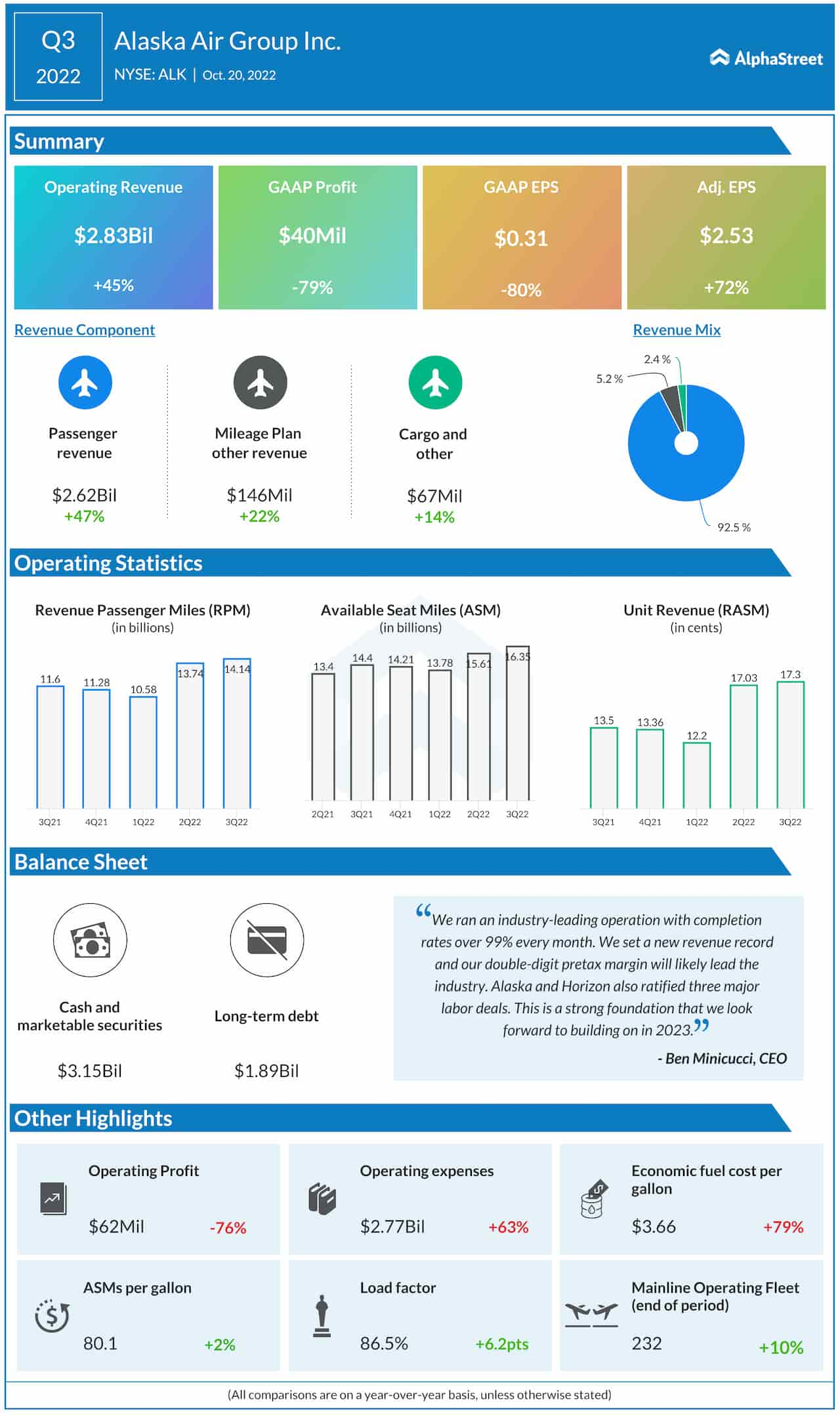

Alaska reported total operating revenues of $2.83 billion in Q3 2022, up 45% compared to Q3 2021 and up 18% compared to Q3 2019. The top line growth was driven by a rise in passenger revenue which was up 47% year-over-year and up 18% compared to 2019. Unit revenues were up 28% YoY and 27% versus 2019, helped by strong pricing and robust demand. For the fourth quarter of 2022, Alaska expects total revenue to be up 12-15% compared to the same period in 2019.

The company reported adjusted EPS of $2.53 in Q3, which was up 72% year-over-year. Adjusted pre-tax margin was 15.6% for the quarter. For the full year of 2022, Alaska expects adjusted pre-tax margin to range between 6-9%.

Capacity and demand

Capacity in the third quarter of 2022 was up 13.3% YoY and down 7% compared to 2019. Load factor exceeded 2019 levels and increased sequentially every month to come in at 86.5% for the full quarter. Business travel volumes have remained around 75-80% recovered from 2019 levels. Despite a slower recovery in corporate demand across the West Coast, Alaska’s business recovery is in line with its peers. In addition, although corporate travel is seeing a slower recovery, the airline is benefiting from more personal travel by employees thanks to the hybrid work model.

For the fourth quarter of 2022, Alaska expects capacity to be down 7-10% versus 2019. The company expects its go-forward capacity to be most constrained in Q4 as it retires 45 aircraft across its total fleet by the end of January. This guidance implies Q4 unit revenue performance of approx. 24% versus 2019. Bookings remain healthy as demand for holiday travel remains steady. Passenger load factor is expected to range between 83-86% in Q4 while yields are currently anticipated to be around 20% higher compared to Q4 2019. For the full year of 2022, capacity is expected to be down 8-9% versus 2019.

Costs

In Q3 2022, cost per ASM excluding fuel and special items (CASM-ex) was up 9.1% year-over-year and up 19% compared to Q3 2019. The company expects its absolute costs to increase from the third to fourth quarter, driven by new labor agreements and expected strong pay-outs for its performance-based pay program.

CASM-ex is expected to be up 20-23% in the fourth quarter of 2022 compared to the same period in 2019. Fuel price per gallon is expected to range between $3.50-3.70 in Q4. For the full year of 2022, CASM-ex is estimated to be up 19-20% compared to 2019.

Click here to read the full transcript of Alaska Air Group’s Q3 2022 earnings conference call