Like most healthcare-related businesses, Abbott Laboratories (NYSE: ABT) has been operating near full capacity for quite some time, with its diagnostics segment registering strong sales growth aided by the high demand for COVID-19 test kits. Typically, the company’s diversified business model comes in handy whenever it is challenged by unexpected events.

Despite the high volatility and market selloff, Abbott’s stock managed to stay above the $100-market so far this year. This week, it traded down 22% from the all-time highs registered around six months ago. But the pullback has created a unique buying opportunity for investors looking for long-term engagement and good yield.

Positive Outlook

ABT has long been an investors’ favorite, especially among income investors due to the company’s impressive track record of creating shareholder value. Currently, there are multiple factors working in its favor, such as low risk, reasonable valuation, and a strong balance sheet. The healthy cash flow should enable the medical device maker to take forward its growth plans with ease and also to return value to shareholders.

Read management/analysts’ comments on Abbott’s Q1 2022 results

Market watchers, in general, are bullish on Abbott’s diversified product portfolio and successful business model. Going by the current trend, it is very likely that the stock would soon change course and hit the recovery path. In short, it seems now is the right time to own ABT.

From Abbott’s Q1 2022 earnings conference call:

“In the U.S., we received FDA approval for Aveir, our leadless pacemaker to treat patients with slow heart rhythms. In Japan, expanded reimbursement for Libre will now cover all people with diabetes who use insulin at least once a day. Cardio-MEMS received an expanded indication in the U.S. to treat more patients suffering from earlier stages of heart failure. And we received U.S. FDA clearance for the latest generation of our EnSite X System, which provides a 360-degree view of the heart for improved cardiac mapping.”

Over the past several years, the company enhanced its profit consistently and the numbers topped expectations throughout the pandemic period. A similar pattern is visible in top-line performance also.

Financial Performance

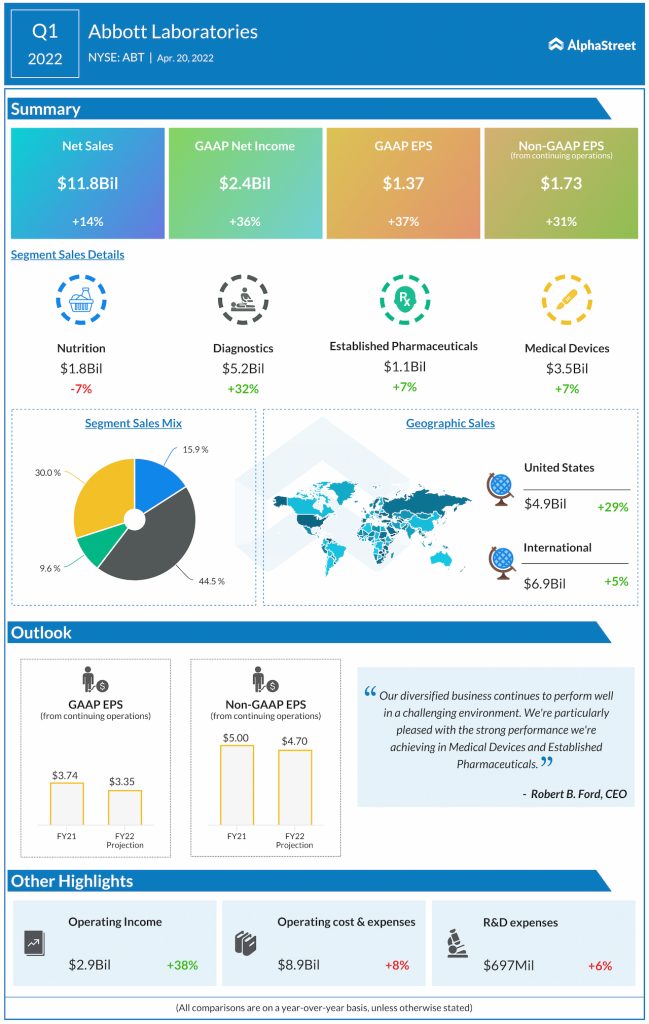

The main operating segments of Diagnostics and Medical Devices performed well in the early months of the fiscal year, driving up first-quarter revenues to $11.8 billion. All the operating segments, excluding Nutrition, witnessed sales growth. As a result, earnings grew by a third to $1.73 per share. The management expects the momentum would continue in the current quarter.

The diagnostics segment’s contribution has grown to nearly half of total revenues, while margins continue to expand reflecting the company’s superior operating efficiency. Abbott will be publishing second-quarter results on July 20 before the opening bell. The consensus estimate is for a 5% decrease in earnings to $1.17 per share on revenues of $10.25 billion, which is up 5%.

ANGO Stock: Is it the right time to invest in AngioDynamics now?

Meanwhile, the recent recall of baby formula produced at one of the company’s US plants has left the market speculating about the future of the Nutrition business, which has experienced a slowdown since then. Abbott’s stock faced high volatility in recent months and all along maintained a modest downtrend. It began Thursday’s session higher but lost momentum as trading progressed.