It is estimated that the size of the global chip manufacturing equipment market would nearly double from the current levels to about $142 billion in the next eight years. Applied Materials, Inc. (NASDAQ: AMAT), a leading semiconductor technology provider to foundries, witnessed a spike in orders during the pandemic as the widespread chip shortage forced companies to expand capacity, thereby lifting the demand for manufacturing equipment.

After staying on an upward spiral for a long time, the company’s stock hit a record high early this year but lost momentum later as markets suffered a heavy selloff. However, its impact on AMAT was moderate compared to the broad market, which shows that investors are still optimistic about the company’s prospects.

Read management/analysts’ comments on quarterly earnings

Complementing the positive investor sentiment, market watchers have set a bullish target price on the stock – they expect a 44% increase over the next twelve months, breaching the 52-week average price. After the recent decline, the valuation is quite attractive now.

Road Ahead

Currently, Applied Materials has a huge backlog of orders, which would have a positive effect on sales in the coming quarters. Encouraged by the boom in the chip market, the management has expressed hope that 2022 and 2023 will be growth years for the company.

Like others in the semiconductor industry, the Santa Clara-based company’s operations have been affected by supply chain headwinds. But the tech firm’s efforts to ease the pressure on production, and stable demand for its products and services can offset the negative impact to a large extent. The management expects the technology inflection would enable the company to outgrow the semiconductor market in the coming years.

From Applied Materials’ Q2 2022 earnings call transcript:

“The picture for 2022 is clear. We have the orders booked, a full build plan, and a large and growing backlog. We believe unconstrained demand for wafer fab equipment would be $100 billion or more. The key question is how quickly supply issues can be mitigated and how much the industry will actually be able to ship this year. The primary focus for our customers is now securing supply for 2023.”

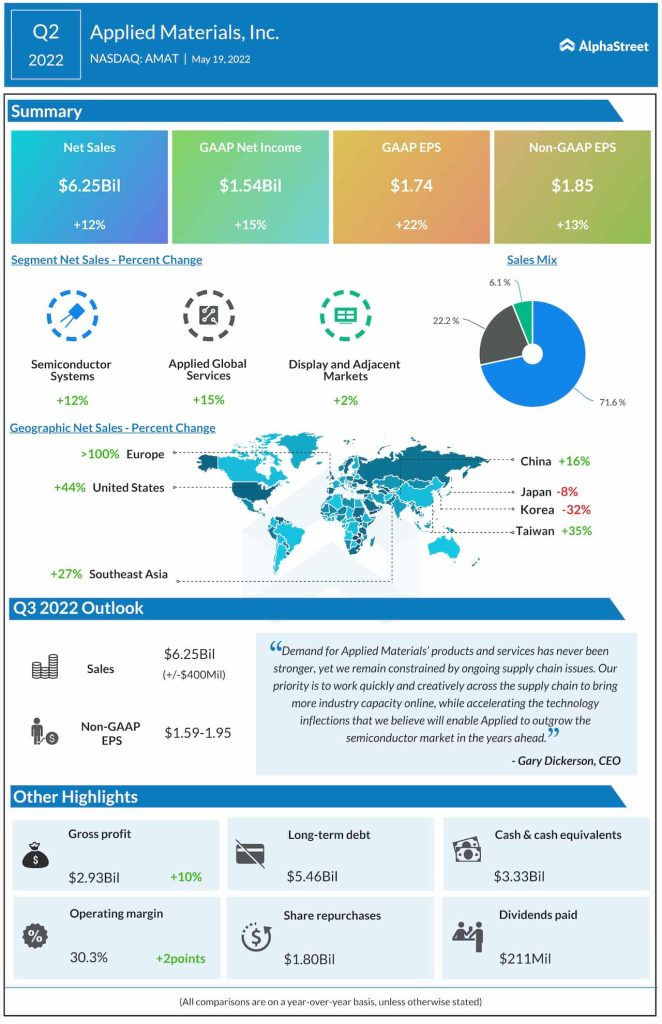

Q2 Results

Applied Materials has been surprisingly resilient to the COVID crisis and all along maintained stable revenue and bottom-line performance, which mostly beat the estimates. However, overall performance fell short of expectations in the second quarter, though all three business segments registered growth, driving up net sales by 12% to $6.25 billion. Consequently, adjusted earnings moved up 13% to $1.85 per share.

INTC Earnings: Highlights of Intel’s Q1 2022 financial results

Applied Materials’ shares are down 36% from the levels seen at the beginning of 2022. After suffering a big loss following the earnings release, the stock closed the last trading session lower.