AlphaStreet Newsdesk powered by AlphaStreet Intelligence

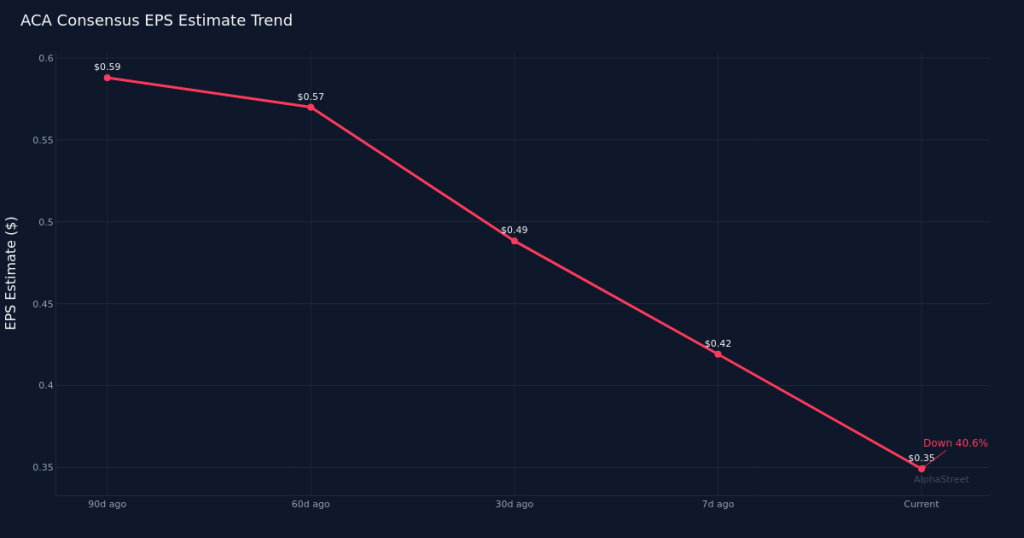

Wall Street expects a difficult quarter. Analysts project Arcosa, Inc. will report earnings of $0.35 per share on revenue of $621.1M when the engineering and construction company releases Q1 2026 results on May 1st. Five analysts cover the stock, with EPS estimates ranging from $0.13 to $0.44 and revenue projections spanning $547.3M to $649.2M. The wide estimate range signals considerable uncertainty around the company’s near-term performance.

Estimates have deteriorated sharply. The current consensus reflects a 28.6% downward revision over the past month, falling from $0.49 just thirty days ago. The trajectory looks even worse on a longer horizon, with the EPS estimate down 40.7% from $0.59 three months ago. This sustained downward pressure suggests analysts have been digesting weaker business conditions or company-specific challenges that emerged during the winter months, forcing a significant reset of expectations heading into the print.

Year-over-year comparisons show contraction. The consensus EPS estimate of $0.35 represents a 28.6% decline from the $0.49 per share Arcosa earned in Q1 2025. Revenue is expected to slip 1.7% from the year-ago period’s $632.0M. The magnitude of the earnings decline far exceeds the modest revenue pullback, pointing to margin compression or operational deleverage. Last year’s first quarter generated $24.0M in net income on a 3.8% net margin, providing a baseline against which investors will measure profitability trends when results are released.

Context matters for an engineering and construction company. Arcosa operates in a sector where project timing, weather conditions, and raw material costs can create significant quarter-to-quarter variability. The first quarter typically faces seasonal headwinds in construction-related businesses, though the year-ago period managed to produce positive earnings despite these challenges. The combination of declining revenue and sharply lower earnings estimates suggests the company may be facing headwinds beyond normal seasonality, whether from reduced infrastructure spending, project delays, or margin pressures in key segments.

The estimate range reveals deep analyst disagreement. The gap between the highest estimate of $0.44 and the lowest at $0.13 is unusually wide, spanning more than triple the low-end projection. This divergence indicates analysts are working with different assumptions about project execution, cost structure, or demand conditions. For investors, this uncertainty means the actual result could swing significantly in either direction, with outperformance or disappointment carrying greater weight than usual in the stock’s reaction.

Profitability trajectory demands attention. With net margin standing at 3.8% in the year-ago quarter and current estimates implying further pressure, investors will scrutinize whether Arcosa can maintain pricing discipline and operational efficiency. Engineering and construction companies face particular sensitivity to input costs, labor availability, and project mix. Any commentary on backlog quality, bidding activity, or margin outlook for the remainder of the year will be critical in assessing whether the current weakness represents a temporary reset or a more fundamental shift in the business environment.

Valuation and sentiment heading into the print. The sharp estimate cuts over the past ninety days suggest investors have likely repriced shares lower in anticipation of weaker results. However, the absence of current stock price data in the verified information prevents quantifying exactly where shares stand relative to their trading range. The post-earnings reaction will hinge not just on whether Arcosa meets the reduced bar, but on management’s commentary about what drove the shortfall and when conditions might stabilize.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.