AlphaStreet Newsdesk powered by AlphaStreet Intelligence

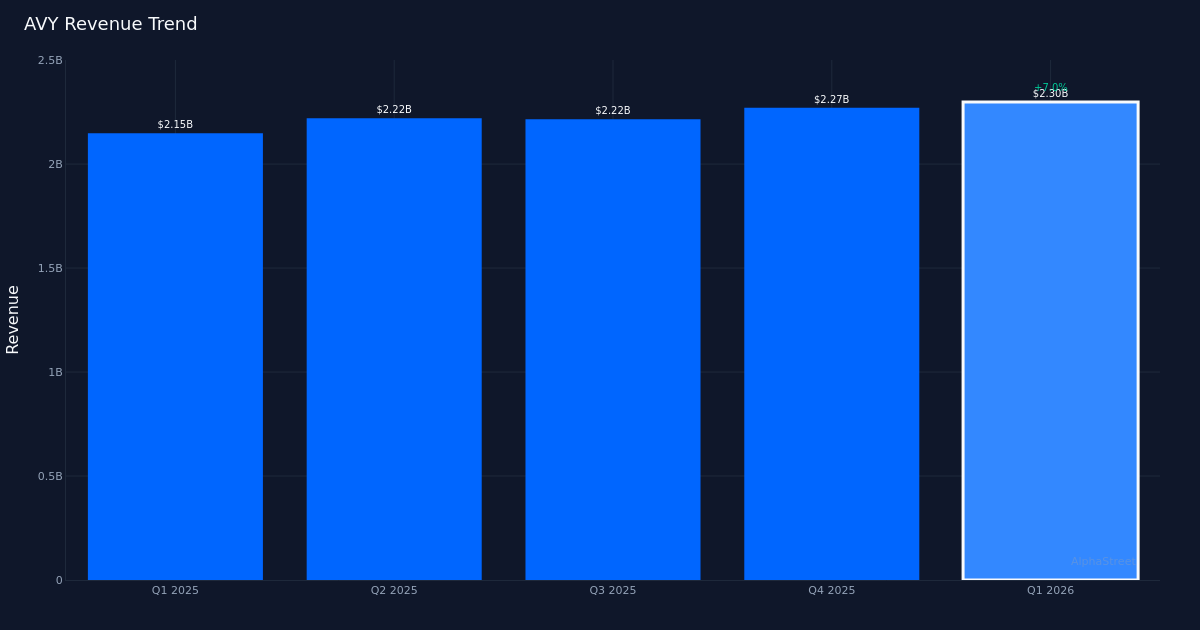

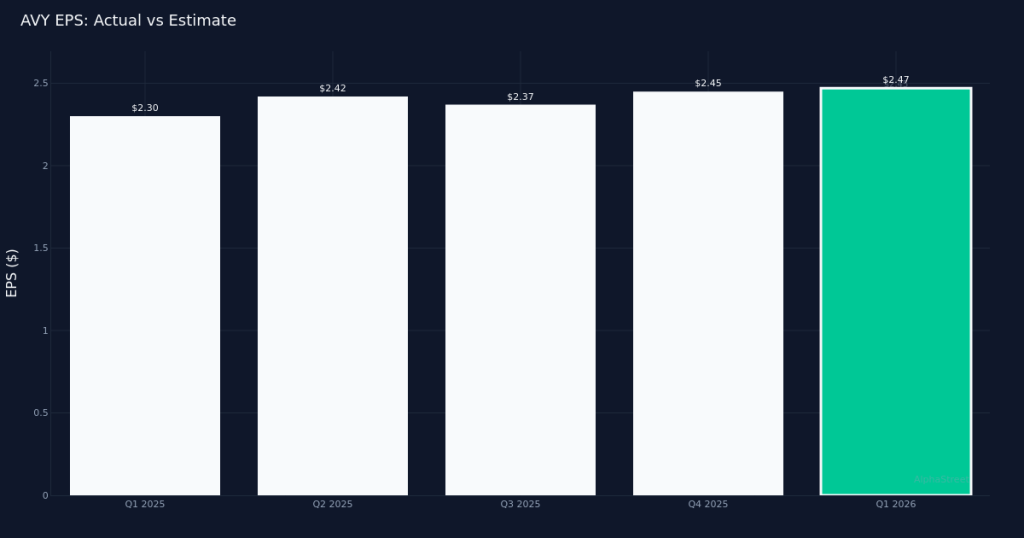

Modest beat delivered. Avery Dennison Corporation (NYSE:AVY) reported Q1 2026 adjusted earnings of $2.47 per share, edging past the Street’s $2.45 estimate by 0.8%. The packaging and containers specialist generated $2.30B in revenue for the quarter, up 7.0% from $2.15B in the year-ago period, with adjusted bottom-line profit reaching $190.5M. The results reflect a company finding growth traction through a combination of volume gains and strategic portfolio positioning, though organic momentum remains measured at just 1.1% for the quarter.

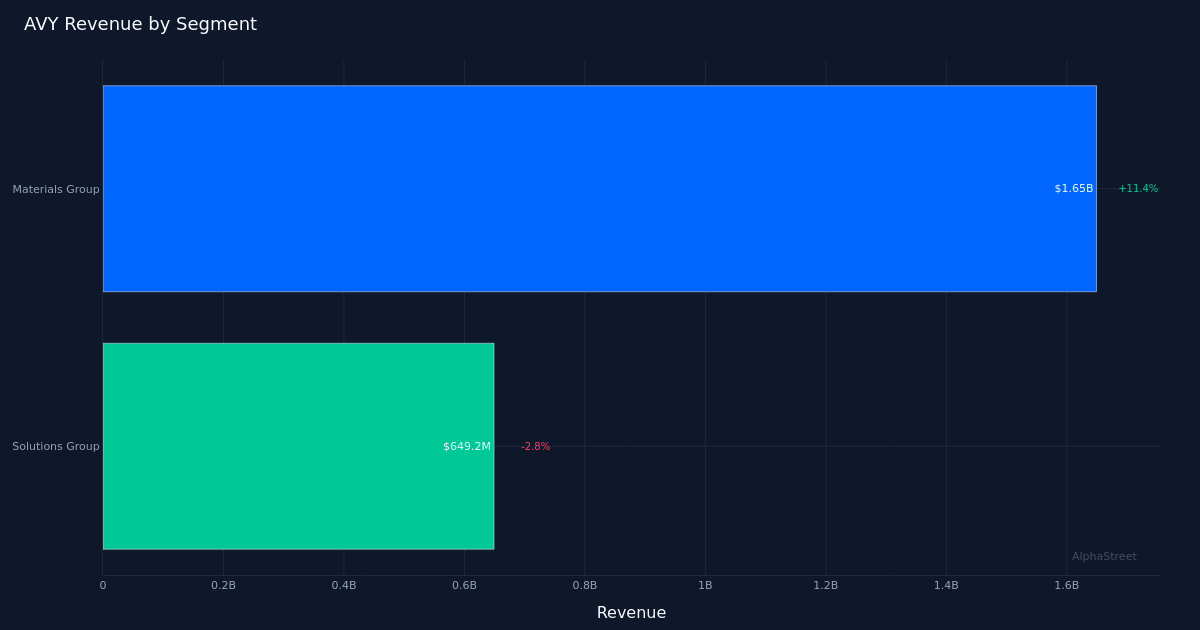

Quality of performance. The earnings beat appears driven primarily by top-line expansion rather than aggressive cost management, a healthier foundation for sustained performance. The 7.0% revenue increase significantly outpaced the 1.1% organic sales change, suggesting acquisitions and favorable currency impacts provided meaningful tailwinds. Materials Group emerged as the clear standout, delivering $1.65B in revenue with an impressive 11.4% year-over-year gain. This segment’s double-digit growth demonstrates strong positioning in pressure-sensitive materials and specialty tapes, markets benefiting from secular trends in e-commerce packaging and industrial applications.

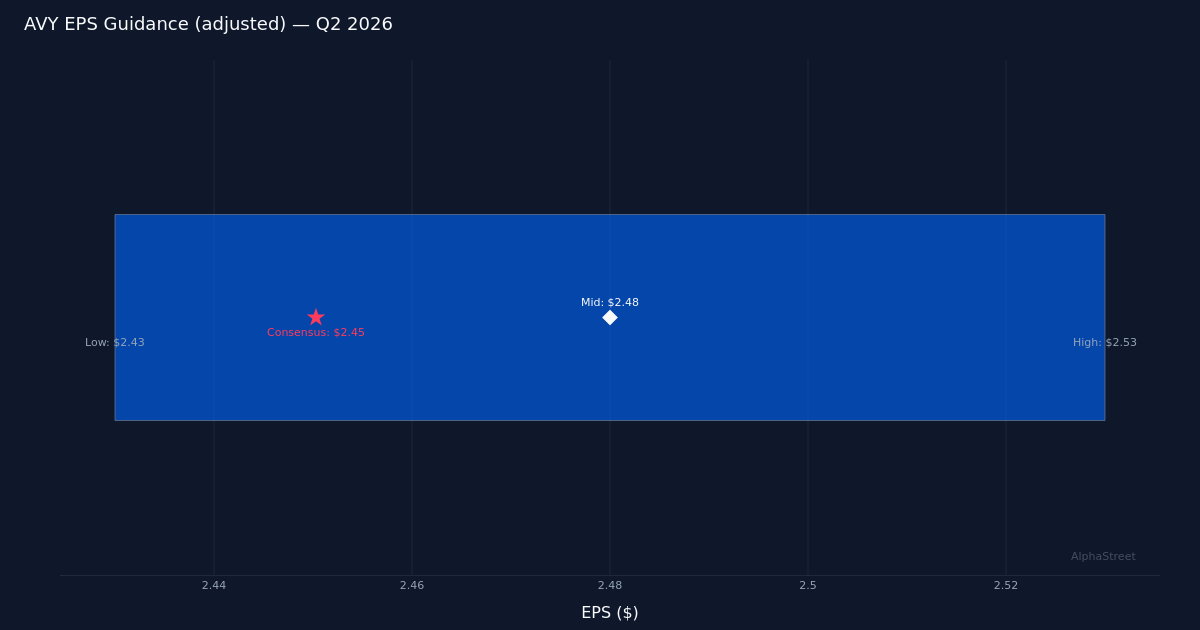

Guidance shows confidence. Management projected Q2 2026 adjusted EPS in the $2.43 to $2.53 range, a guidance band that straddles current quarter performance. The midpoint of $2.48 represents a modest sequential uptick and signals management’s expectation for stable operating conditions through the spring months. This guidance framework suggests the company anticipates continued Materials Group strength offsetting any potential softness in other divisions, while maintaining disciplined cost control across the enterprise.

Market reaction muted. Shares traded largely unchanged following the release, indicating investors viewed the results as broadly in line with expectations despite the technical beat. The lack of stock movement suggests the market had already priced in this level of performance, or alternatively, that concerns about the modest organic growth rate offset enthusiasm for the headline beat. With analyst sentiment skewing constructive at 7 buy ratings versus 5 hold ratings and zero sells, the Street maintains a generally favorable outlook on the company’s positioning.

Operational execution solid. The divergence between reported revenue growth of 7.0% and organic sales expansion of 1.1% merits attention. While inorganic contributions boosted the headline figure, the underlying organic performance reveals a more challenging demand environment where volume and pricing power remain constrained. For a packaging materials company navigating inflationary input costs and evolving customer requirements, maintaining even low-single-digit organic growth represents competent execution, though hardly exceptional.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.