Home goods retailer Bed Bath & Beyond Inc. (NASDAQ: BBBY) has been going through a rough patch for quite some time. Though the company is making progress in its transformation efforts, by enhancing omnichannel capabilities and optimizing the store fleet, it might not be sufficient for a turnaround.

After slipping into the single-digit territory last month, the stock has maintained a downtrend. The company suffered heavy losses in recent quarters, missing estimates every time. The underlying weakness of the business and falling sales make BBBY one of the riskiest stocks. In general, analysts following the stock are cautious in their outlook, citing its bleak future prospects.

Outlook

For the New Jersey-headquartered company, which operates nearly 1,000 retail stores and an eCommerce platform, the upcoming holiday season is crucial as it would determine the future of the business. It is estimated that sales would be affected by the unfavorable merchandise mix, due to disruption in the supply of several leading brands.

Bed Bath & Beyond Inc Q1 2022 Earnings Call Transcript

The absence of their favorite items on the shelves of Bed Bath & Beyond will discourage customers from returning to the stores, and the shrinking store traffic might push the company into bankruptcy. It is bad news at a time when it is making aggressive efforts to retain customers and increase store footfall.

Turnaround

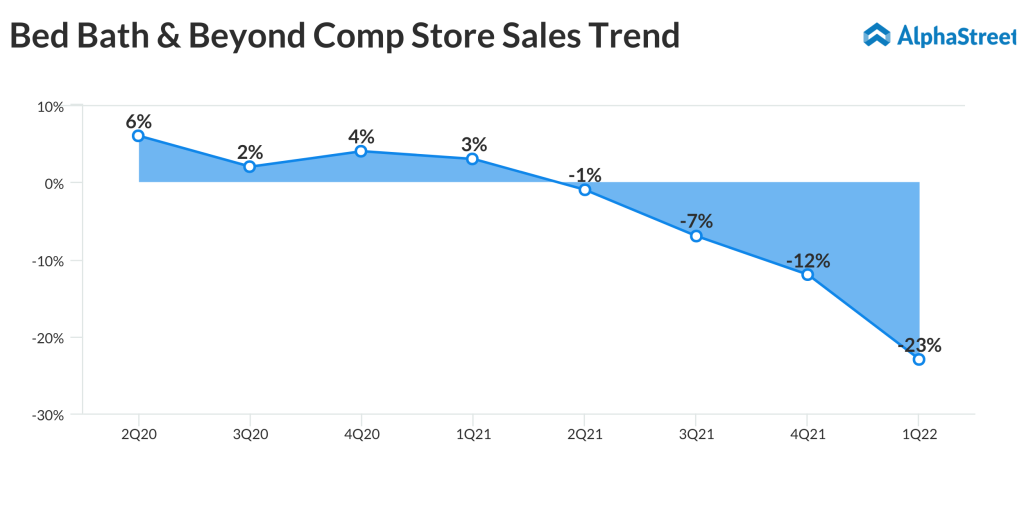

Recent performance shows the problems are more deep-rooted than they appear to be. It looks like the company needs a broader strategy to revive the brand, expand eCommerce sales and retain customers.

One of the major concerns is the deteriorating balance sheet, marked by elevated debt – total liabilities stand at $5.2 billion — with the tough economic backdrop adding to the challenges. In the first quarter of 2022, the company incurred an adjusted loss of $2.83 per share, compared to a profit of $0.05 per share in the prior-year period. The bottom line was negatively impacted by a sharp decline in net sales to $1.46 billion, reflecting a 25% fall in comparable store sales.

Leadership Crisis

The dismal first-quarter performance forced then CEO Mark Tritton to step down after he failed to lead the turnaround, the purpose for which he was brought in a few years ago. The leadership crisis deepened after the departure of the company’s merchandising chief, and more recently the death of chief financial officer Gustavo Arnal.

From Bed Bath & Beyond’s Q1 2022 earnings conference call:

“In the near term, we have very clear priorities for where we must see improving results. First, we have to make sure we are focusing resources on driving traffic to stores and digital platforms. We also must prioritize how we are serving customers to recapture market share. I believe a lot of this work is best done in a back-to-basics mantra that prioritizes knowing our customers and delivering the experience they deserve wherever they interact with us.”

Walmart Stock: How does WMT perform in the changing retail landscape

Bed Bath & Beyond will be publishing second-quarter results on Thursday before the opening bell. Analysts are looking for an adjusted loss of $1.85 per share on revenues of $1.47 billion.