Shares of The Campbell’s Company (NASDAQ: CPB) were up 1% on Thursday. The stock has dropped 7% over the past three months. The soup and snacks company delivered mixed results for the second quarter of 2025 and lowered its guidance for the full year as it continues to face challenges in its snacks business.

Sales and profits

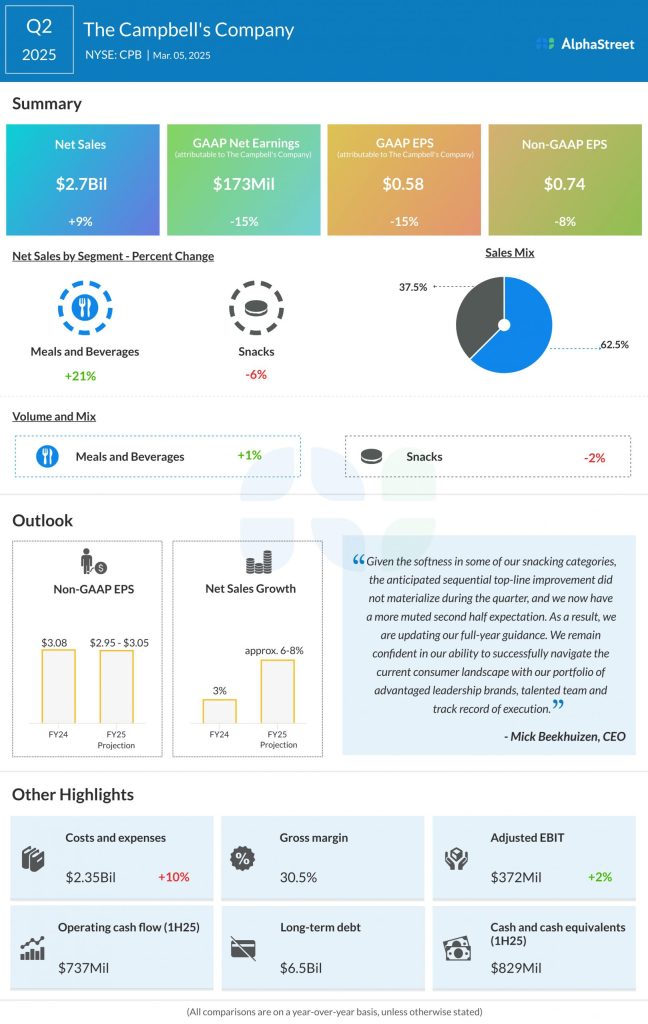

Campbell’s net sales grew 9% year-over-year to $2.7 billion in Q2 2025, benefiting from the Sovos Brands acquisition. Organic sales were down 2%, hurt by weakness in some of the snacking categories. GAAP earnings per share decreased 15% to $0.58 while adjusted EPS fell 8% to $0.74.

Snacks weakness – a continued headwind

In Q2, Campbell’s did not see the recovery it expected in some of its snacking categories and this not only hurt its quarterly performance but also led it to lower its guidance for the year. The Snacks segment saw net sales decrease by 6% in the second quarter. Organic sales were down 3%, driven by declines in third-party partner and contract brands, Goldfish crackers, and Snyder’s of Hanover pretzels.

Weak category performance and tough competition negatively impacted the Goldfish brand while the salty snacks category has been facing headwinds from new entrants and increased promotions. Meanwhile the Pepperidge Farm brand delivered strong performance in cookies and stuffing.

Margins in the Snacks business were impacted by increased promotional and marketing investments during the holiday season, higher supply chain costs, and unfavorable mix. CPB anticipates Snacks margins to improve sequentially throughout the third and fourth quarters of 2025 compared to the second quarter.

Resilience in Meals & Beverages

The Meals & Beverages division continued to see momentum in Q2, with net sales increasing 21%, helped by the Sovos acquisition. Organic sales dropped 1% due to declines in SpaghettiOs and US soup. The soup portfolio benefited from an increase in at-home cooking, which drove growth in condensed cooking and broth. However, declines in condensed soups and ready-to-serve soups led to a drop in US soup sales.

Within the ready-to-serve portfolio, the Chunky, Pacific, and Rao’s brands performed well during the quarter. In the Italian sauce portfolio, Prego and Rao’s delivered strong performances. Campbell’s remains optimistic on Rao’s becoming its next $1 billion brand.

Lowered outlook

Due to the ongoing challenges in its snacks business, Campbell’s lowered its guidance for the full year of 2025. It now expects net sales to grow 6-8% while organic sales are expected to be down 2% to flat. Adjusted EPS is now expected to be $2.95-3.05, or down 4% to down 1% year-over-year.