Cisco Systems Inc. (NASDAQ: CSCO), which dominates the enterprise network infrastructure market, is working to expand beyond its core business through acquisitions and by investing in tech innovations like AI. Recently, the company embarked on an organizational restructuring, with focus on cost-cutting.

Cisco’s stock tumbled on Wednesday after it reported flat second-quarter results and announced a major workforce reduction. Investor sentiment was also hurt by the management’s weak guidance. In the following session, CSCO traded slightly below its 52-week average. The shares have lost about 3% so far in 2024. The company has hiked quarterly dividends regularly and offers an impressive yield of about 3%, which is well above the market average.

SaaS Growth

Of late, there has been an uptick in Cisco’s recurring revenues, reflecting the shift in its business model with focus on raising subscription renewals. As part of its efforts to diversify the business, the company made a series of acquisitions last year and is preparing to add more businesses to its fold. The software-as-a-service business should benefit from the acquisition of cybersecurity firm Splunk, which is expected to be completed in the third quarter of 2024.

The company has lowered its guidance for fiscal 2024, to reflect cautious customer spending amid elevated inventory levels and concerns over the high interest rates. Though demand spiked post-pandemic when markets reopened and supply chain issues eased, the momentum waned later as customers postponed their installations due to macro headwinds.

From Cisco’s Q2 2024 earnings call:

“Over the next six months, you can expect more meaningful announcements across the portfolio through our accelerated organic innovation and inorganic investments. In addition, we have now extended our AI-powered ThousandEyes into Cisco Secure Access joining past integrations with AppDynamics, WebEx Catalyst, and Meraki platforms. ThousandEyes allows our customers to understand the digital experience of users, applications, and things through billions of daily measurements of the Internet and public SaaS, as well as thousands of enterprise customers creating best-in-class digital experiences for users.”

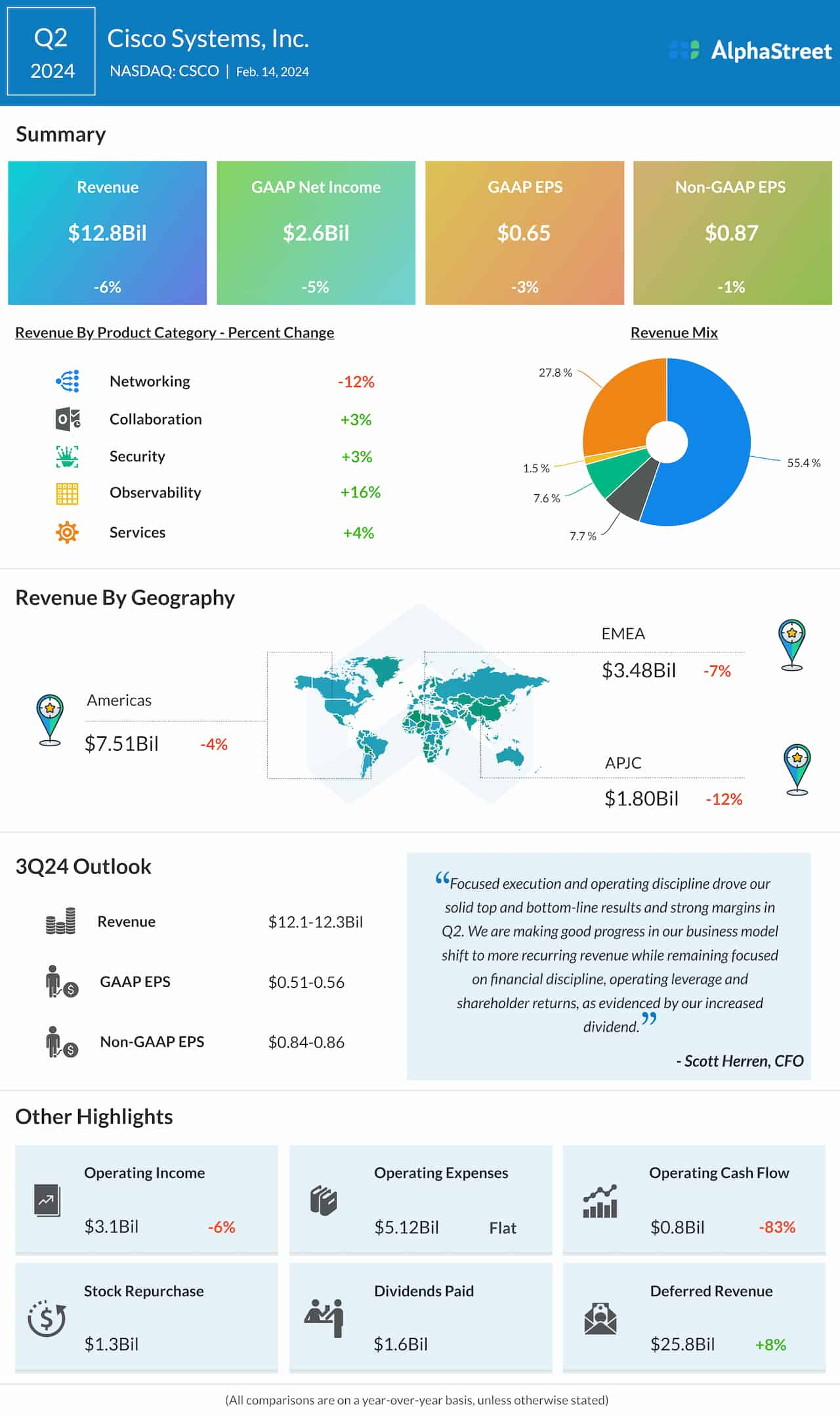

Weak Q2

In the second quarter, Cisco’s revenues and earnings declined. However, the numbers topped expectations, a trend that has continued over the past several years. Q2 revenues decreased 6% year-over-year to $12.8 billion, mainly reflecting a double-digit fall in Networking revenues that more than offset growth in the other segments. Operating expenses remained broadly unchanged from last year as the company works to achieve better cost efficiency.

For the third quarter, the management expects revenues to be in the range of $12.1 billion to $12.3 billion and adjusted earnings to be between $0.84 per share and $0.86 per share. Full-year adjusted profit is expected to be between $3.68 per share and $3.74 per share, on revenues of $51.5-$52.5 billion. The revised outlook is below analysts’ forecast.

Cost-Cutting

During the earnings call, Cisco’s leadership revealed plans to reduce the company’s workforce by 5% as part of a restructuring program, triggering a stock selloff. CSCO suffered one of the worst single-day losses in recent times and slipped below the $ 50 mark. The weakness continued on Thursday and the stock traded down 2% in the afternoon.