After ending a choppy session on Friday, US futures are pointing to a lower open in the stock market today. A partial shutdown of the US government is likely to continue until after Christmas as the Congress missed a midnight Friday deadline for getting a spending bill passed.

President Donald Trump and Democratic lawmakers remain discrete on the issue of funding for the president’s controversial border wall. The partial shutdown took effect at midnight on Friday as Trump has demanded $5 billion for construction of the wall on the border with Mexico. No votes are scheduled to end the stalemate until after Christmas.

The S&P futures declined 3.74% to 2,393.25, Dow futures fell 3.45% to 22,204 and Nasdaq plunged 5.09% to 6,003.50. Elsewhere, shares at Asian markets closed mixed on Monday, and European stocks are inching lower.

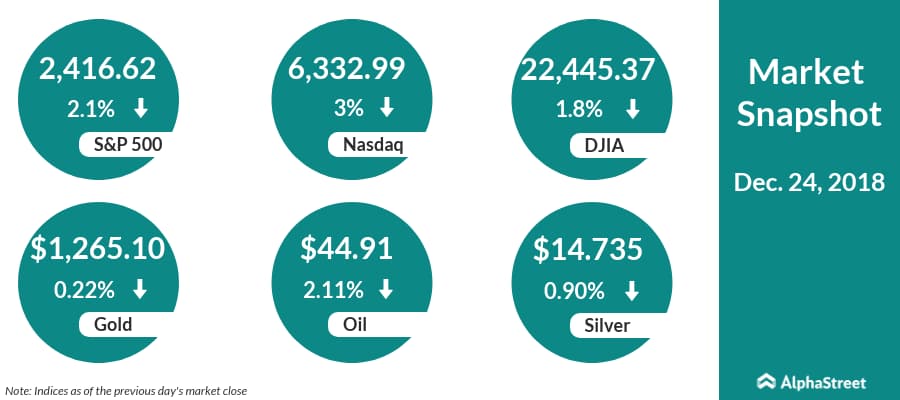

On December 21, US ended lower, with Dow down 1.8% to 22,445.37, the Nasdaq dropped 3% to 6,332.99 and the S&P 500 inched down 2.1% to 2,416.62. Traders remained concerned about the higher risk of a partial government shutdown. The markets were also impacted by the renewed concerns of the US-China trade talks.

Meanwhile, White House trade advisor Peter Navarro said the trade war between the US and China would not come to an end in near-term. On the economic front, the Chicago Fed National Activity Index for November is set for release today.

The markets will finish early to mark Christmas Eve and will be closed for the holiday on Tuesday. The normal trading hours are expected for the rest of the week. But volumes are likely to be thinner and the move could be exaggerated as most of the traders are out for the holidays.

Last week, the Federal Reserve lifted its benchmark interest rate for the fourth time this year by 25 basis points to 2.5%. Chairman Jerome Powell said the Fed will continue to unwind its balance sheet at the current pace. Traders were concerned that the stock market declines were hurt by the two monetary tightening actions.

Crude oil futures are down 2.11% to $44.91. Gold is trading down 0.22% to $1,265.10 and silver is down 0.90% to $14.735. On the currency front, the US dollar is trading down 0.23% at 110.957 yen. Against the euro, the dollar is up 0.33% to $1.1405. Against the pound, the dollar is up 0.21% to $1.2656.

Follow our Google News edition to get the latest stock market, earnings and financial news at your fingertips.

Most Popular

CVX Earnings: Chevron reports lower revenue and profit for Q1 2024

Energy exploration company Chevron Corporation (NYSE: CVX) announced first-quarter 2024 financial results, reporting a decline in net profit and revenues. Net income attributable to Chevron Corporation was $5.50 billion or

ABBV Earnings: AbbVie reports lower adj. profit for Q1 2024; revenue edges up

Specialty biopharmaceutical company AbbVie, Inc. (NYSE: ABBV) Friday announced first-quarter 2024 financial results, reporting a decline in adjusted earnings and a modest rise in revenues. The company reported worldwide net

CL Earnings: Key quarterly highlights from Colgate-Palmolive’s Q1 2024 financial results

Colgate-Palmolive Company (NYSE: CL) reported first quarter 2024 earnings results today. Net sales increased 6.2% year-over-year to $5.06 billion. Organic sales increased 9.8%. Net income attributable to Colgate-Palmolive Company was