While the increase in the demand for residential properties during the pandemic came as a relief to the housing market, related businesses like construction-equipment manufacturing also benefited from the surprise-growth. Excavator maker Caterpillar Inc. (NYSE: CAT) has stayed resilient to the slowdown so far and sees the positive momentum to continue supported by the recovery in the international markets, especially in the Asia Pacific.

Read management/analysts’ comments on Caterpillar’s Q4 results

Caterpillar’s stock surged to a record high this week, after gaining steadily for about one year. The current target price indicates it might pull back in the coming months and settle around the $200-mark. That calls for caution as far as investing in CAT is concerned, though prospective investors willing to take a risk can still go for it.

COVID Impact

Sales of the Illinois-based company — the largest construction equipment manufacturer in the world — were affected by lower end-user demand and decline in dealer inventories, but its performance last year was better than expected. However, there are concerns that the company might find it difficult to achieve its operating margin target and long-term growth goals — with focus on continued investment in new products and services.

On the positive side, the mining sector is getting back on track after the initial slump, which is good news for Caterpillar given its substantial market share in that market.

Earnings Beat

Interestingly, the company’s earnings beat estimates more frequently during the crisis than in the pre-COVID era, mainly reflecting the resilience of the construction industry to the pandemic. The bottom-line continues to benefit from the management’s efforts to reduce cost. Meanwhile, cash flow came under pressure from the move to maintain higher inventory to ease supply chain disruptions.

From Caterpillar’s Q4 2020 earnings conference call:

“We expect to achieve our investor day operating margin targets in 2021 despite the impact of reinstating short-term incentive compensation. We also expect to meet our investor day free cash flow targets this year. Given our intention to return substantially all of our ME&T free cash flow to shareholders, as well as our desire to be in the market on a regular basis, we expect to revisit our current pause in share repurchases later this year.”

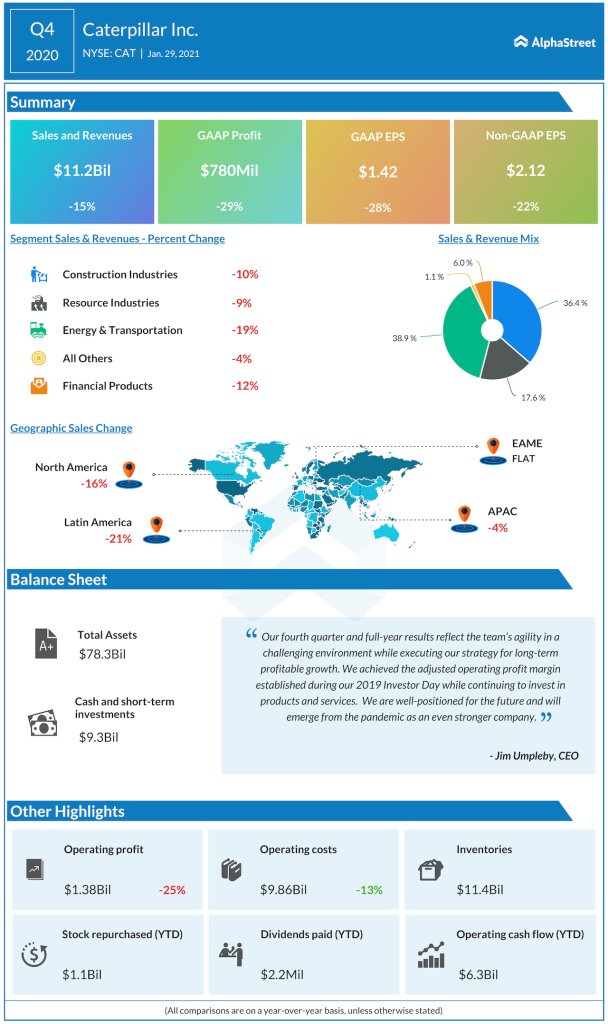

In the fourth quarter, a broad-based contraction across all business segments resulted in a 15% drop in revenues to $11.2 billion. As a result of the weak top-line performance, adjusted earnings declined to $2.12 per share from $2.71 per share in the year-ago period. Still, it was better than the outcome analysts had predicted, thanks to the management’s cost-cutting initiatives that helped in reducing operating expenses significantly. The market responded positively to the results and the stock rallied after the announcement.

At the Bourses

The company’s market value nearly doubled since last year, with the stock making strong gains during the pandemic period after recovering from the initial slump. It advanced 22% since the beginning of the year, far outperforming the broad market.