AlphaStreet Newsdesk powered by AlphaStreet Intelligence

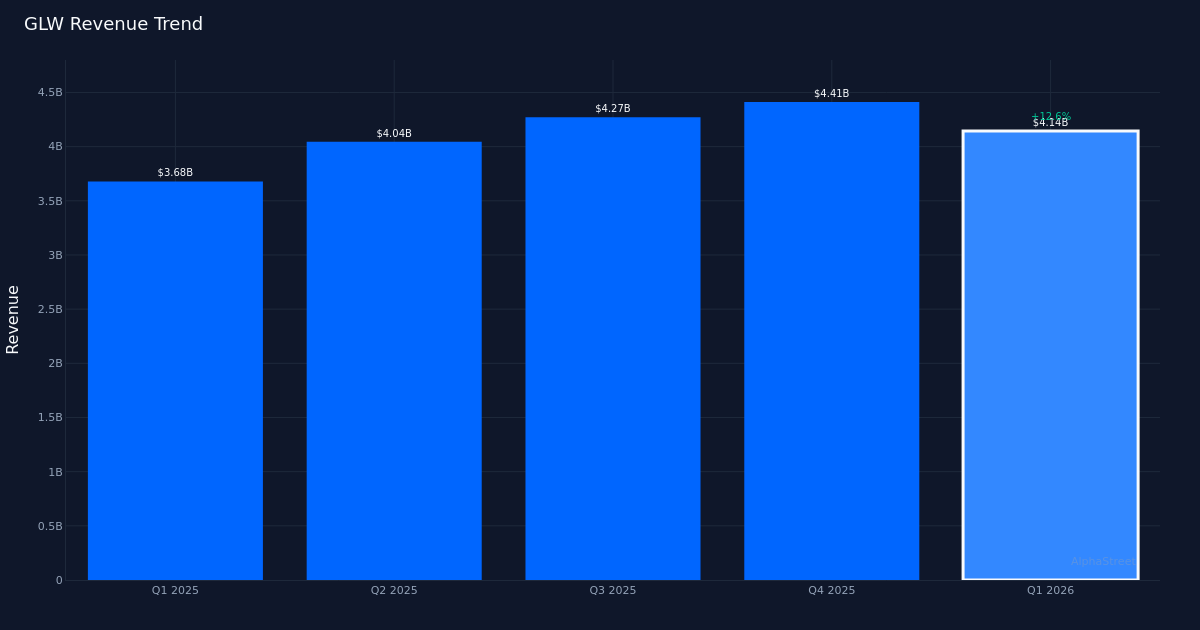

In-Line Earnings. Corning Incorporated (NYSE: GLW) delivered Q1 2026 core earnings of $0.70 per share, matching the $0.70 consensus estimate, while revenue totaled $4.14B for the quarter. The electronic components manufacturer posted adjusted profit of $612.0M as demand strength drove a 20.0% increase in sales from the $3.45B recorded in Q1 2025. The stock retreated 4.5% to $168.01 despite the solid top-line performance, suggesting investors had priced in upside or are concerned about near-term margin dynamics.

Revenue Quality. The 20.0% year-over-year revenue expansion reflects genuine demand strength rather than financial engineering, a critical distinction for institutional investors assessing earnings sustainability. The company’s ability to translate robust sales growth into profit demonstrates operational leverage in its electronic components business, though the market’s negative reaction indicates skepticism about whether this pace can continue. With revenue climbing substantially faster than in recent quarters, Corning appears to be capturing share in key end markets.

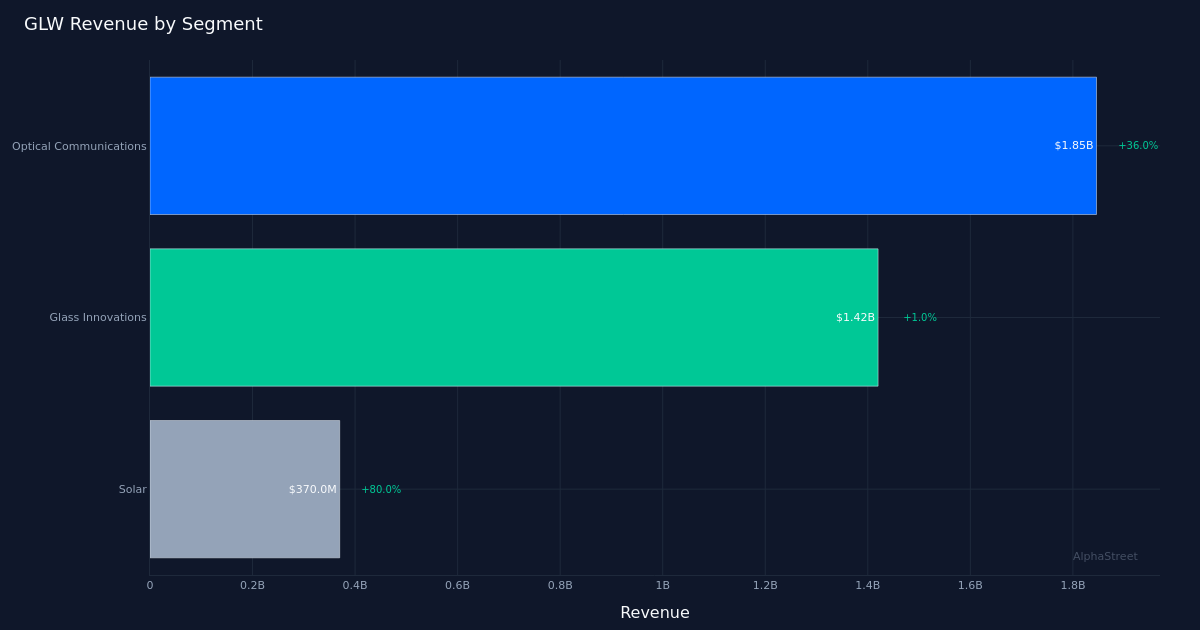

Optical Communications Momentum. The standout performance came from Optical Communications, which generated $1.85B in revenue, up 36.0% year-over-year, establishing itself as the clear growth driver for the quarter. This segment’s acceleration reflects sustained infrastructure buildout and data center expansion, trends that typically have multi-year runways. The magnitude of growth in this division suggests Corning is well-positioned in secular growth markets where capacity constraints and technological advancement create pricing power.

Guidance Framework. Management projected Q2 2026 EPS in the $0.73 to $0.77 range, representing a sequential improvement at the midpoint, while expecting revenue of $4.60B for the next quarter. The revenue guidance implies continued momentum from Q1 levels, though the sequential step-up will require sustained performance across business segments. The EPS guidance range provides flexibility for margin variability, but the midpoint of $0.75 suggests management confidence in maintaining profitability while investing for growth.

Wall Street Positioning. Analyst sentiment remains constructive with a consensus of 10 buy ratings and 5 hold ratings, with no sell recommendations in the coverage universe. This positive bias reflects confidence in Corning’s market position and growth trajectory, though the stock’s decline following results may prompt some analysts to revisit their price targets. The lack of sell ratings suggests the investment community views the current valuation as reasonable despite near-term execution questions.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.