AlphaStreet Newsdesk powered by AlphaStreet Intelligence

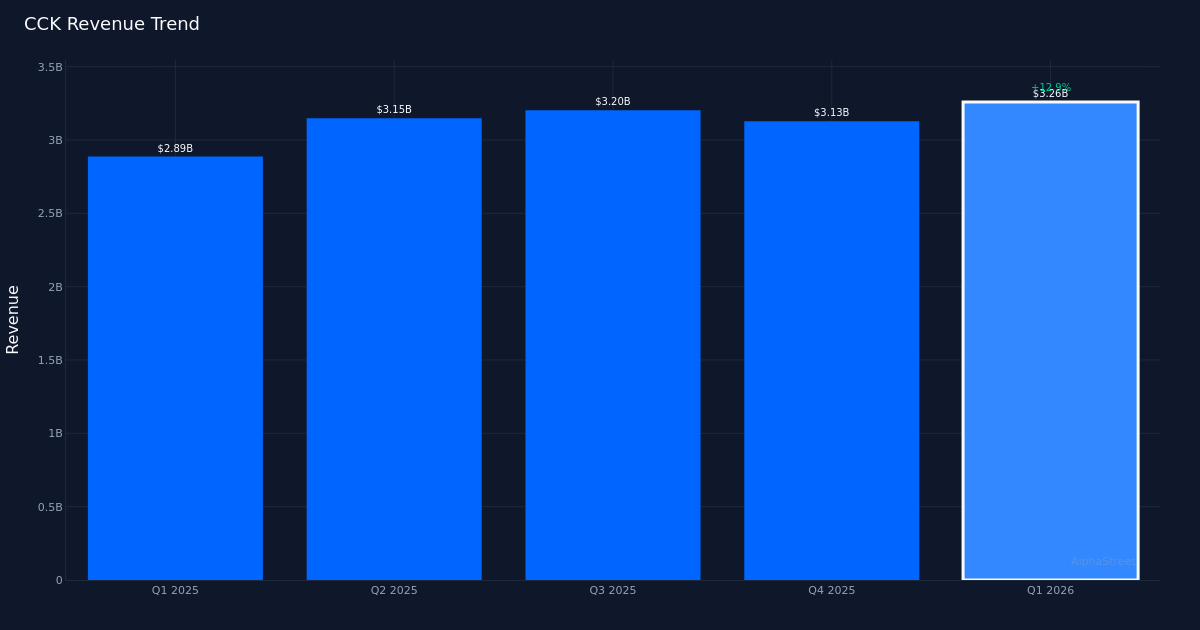

Solid beat. Crown Holdings, Inc. (CCK) delivered Q1 2026 adjusted earnings of $1.86 per share, beating the $1.75 consensus estimate by 6.3% and signaling strong execution in a rebounding packaging market. Revenue totaled $3.26B for the quarter, representing a 12.9% increase from the $2.89B recorded in Q1 2025. The company posted $209.0M in adjusted net income as demand across its beverage packaging portfolio accelerated. Shares traded largely unchanged following the report, suggesting investors may have anticipated the strong performance, or are awaiting further clarity on full-year margin trajectory.

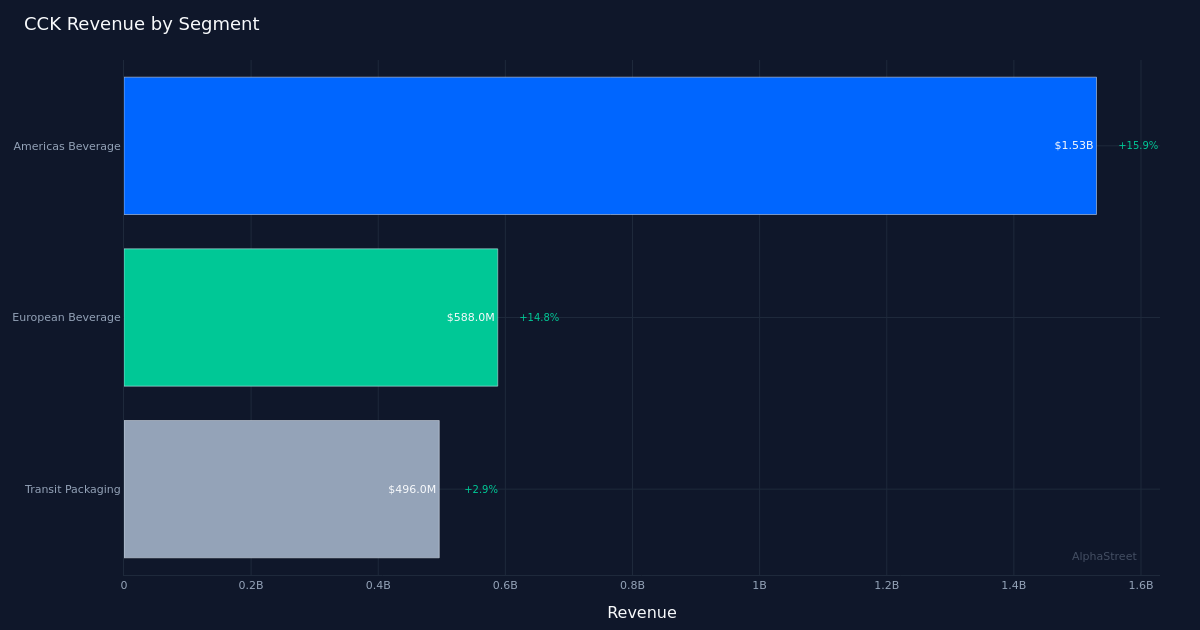

Revenue-driven performance. The quality of this beat appears genuine, anchored by meaningful top-line growth rather than aggressive cost management alone. Global beverage shipments rose 5.0% for the quarter, demonstrating healthy underlying demand across Crown’s core markets. Americas Beverage led the charge with $1.53B in revenue, up 15.9% year-over-year, as the segment capitalized on elevated consumer demand for canned beverages and continued share gains in sustainable aluminum packaging. This double-digit segment growth underscores Crown’s positioning in a market where beverage manufacturers increasingly favor aluminum over alternative materials.

Guidance provides roadmap. Management guided full-year 2026 adjusted EPS to a range of $7.90 to $8.30, establishing clear expectations as the company navigates the balance of the year. The midpoint of this range suggests management anticipates sustained momentum from Q1’s performance, though the width of the guidance window leaves room for variability depending on raw material costs and global demand patterns. Investors will scrutinize whether Crown can maintain the margin discipline demonstrated this quarter while continuing to invest in capacity expansion to meet beverage can demand.

Market sentiment mixed. Wall Street consensus stands at 8 buy, 6 hold, and 0 sell ratings, reflecting a moderately bullish stance on the stock. The absence of sell ratings indicates analysts see limited downside risk, while the split between buy and hold recommendations suggests some debate over valuation at current levels. The muted stock reaction following a clear earnings beat may reflect concerns about whether the Americas Beverage growth rate can sustain through tougher comparisons later in the year, or whether raw material headwinds could pressure margins in subsequent quarters.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.