DocuSign Inc. (NASDAQ: DOCU) has benefited significantly from the work-from-home trend that gained prominence during the COVID-19 pandemic. The company reported strong results for the first quarter of 2021 and expects the solid momentum to continue in the coming months.

Q1 Performance

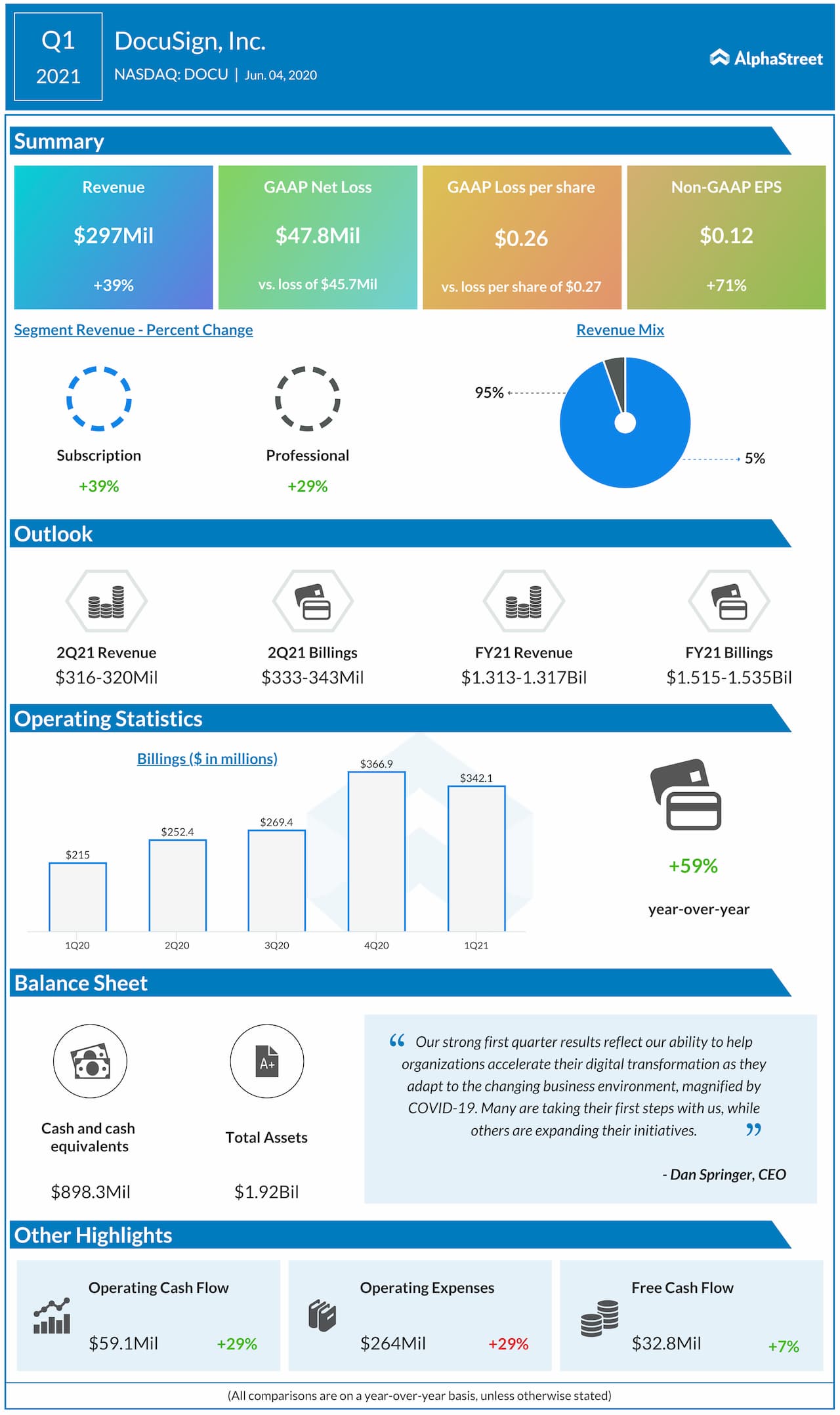

DocuSign witnessed a 39% increase in revenue along with a 59% growth in billings, driven by both the adoption by new customers as well as an expansion in use cases across a broad portion of its installed base.

The company’s paying customers totaled around 661,000

globally, driven by the addition of over 10,000 net new direct customers and

around 58,000 self-service customers. The results benefited from the strong

sales of its eSignature solutions. Expansions and upsells to existing customers

in eSignature drove a dollar net retention of 119% in the quarter.

Digital

transformation

The shift to remote work caused by the pandemic led to faster

digital transformations across companies thereby leading to higher demand for

DocuSign’s products. As companies needed to sign and manage their agreements, irrespective

of location, DocuSign’s eSignature solution saw a rise in demand.

“For organizations that hadn’t already embraced DocuSign for eSignature, that were only using us for a few select use cases, the pandemic has been a catalyst for the greater digital transformation of their end-to-end agreement processes. We always believed this transformation will happen and that a unifying platform for agreements will be needed.” – Dan Springer, CEO

ADVERTISEMENT

The company does not expect the move towards remote work and

digital transformation to reverse in a post-COVID business environment and

believes the trend will only accelerate going forward. Organizations will

continue to shift their processes to digital platforms and the demand for

solutions that help simplify this procedure will increase.

DocuSign expects the adoption of eSignature by new customers

and the expansion of use cases by existing customers to continue. This demand

for eSignature is expected to lead to the adoption of other Agreement Cloud

products as well thereby providing additional benefits. DocuSign believes that

as companies realize the simplicity, cost efficiency and speed of digital

processes, they are seldom likely to go back to their old procedures.

Outlook

DocuSign believes that as the pandemic subsides and the restrictions slowly go away, there might be a slight pull-back in the remote work and travel trends but there will not be a complete return to the old levels. The company expects its churn levels to remain consistent with the prior year.

The company expects subscription revenues to be $298-302 million in the second quarter of 2021 and $1.243-1.247 billion for fiscal year 2021.

Click here to read the full transcript of DocuSign Q1 2021 earnings call