American Express Company (NYSE: AXP) is scheduled to report second quarter 2019 earnings results on Friday, July 19, before market open. The consensus estimate is for earnings of $2.03 per share on revenue of $10.82 billion. In the trailing four quarters, the company has topped earnings estimates three times.

The results in the second quarter are expected to be driven by higher cardmember spending, loan volumes and billings growth. Revenues are expected to benefit from higher member spending and fee income. New memberships and related income are also likely to help the topline numbers.

The credit card provider’s partnerships with other companies

like Delta Air Lines (NYSE: DAL) are also likely to benefit revenues during the

quarter. The growth in revenues will prove beneficial to the bottom line numbers.

However higher expenses related to customer services are likely to put pressure

on margins during the period.

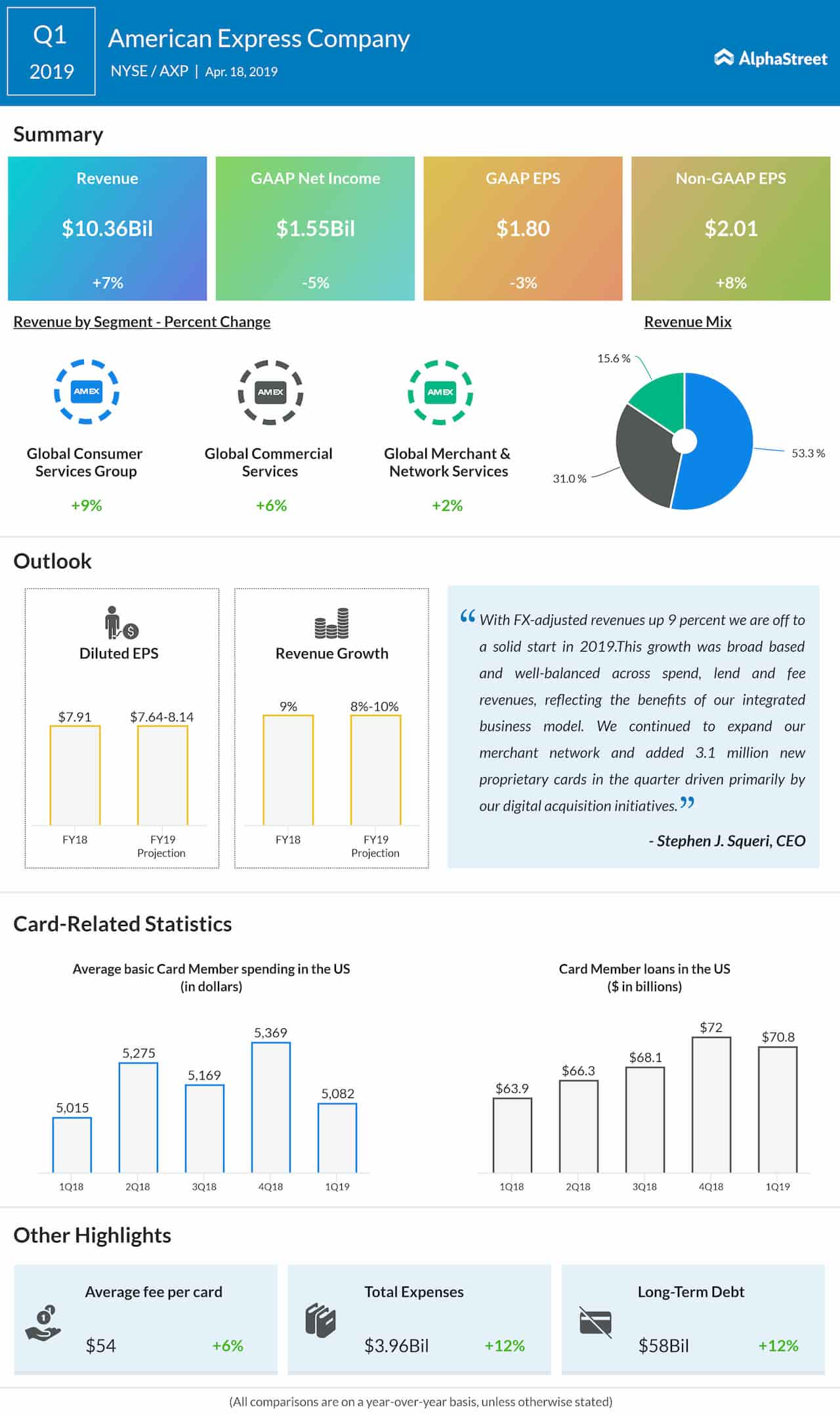

In the first quarter of 2019, Amex beat earnings estimates but missed the mark on revenue. Revenue grew 7% year-over-year to $10.36 billion while adjusted EPS grew 8% to $2.01. The company saw revenue increases across all its segments.

For fiscal year 2019, Amex has guided for GAAP EPS to come

in the range of $7.64-8.14 and adjusted EPS in the range of $7.85-8.35. The

company expects revenue to grow 8-10% during the year.

American Express’ shares have gained 27% in the trailing 52 weeks and over 35% so far this year. The majority of analysts have rated the stock as Hold while others have rated it as Buy.