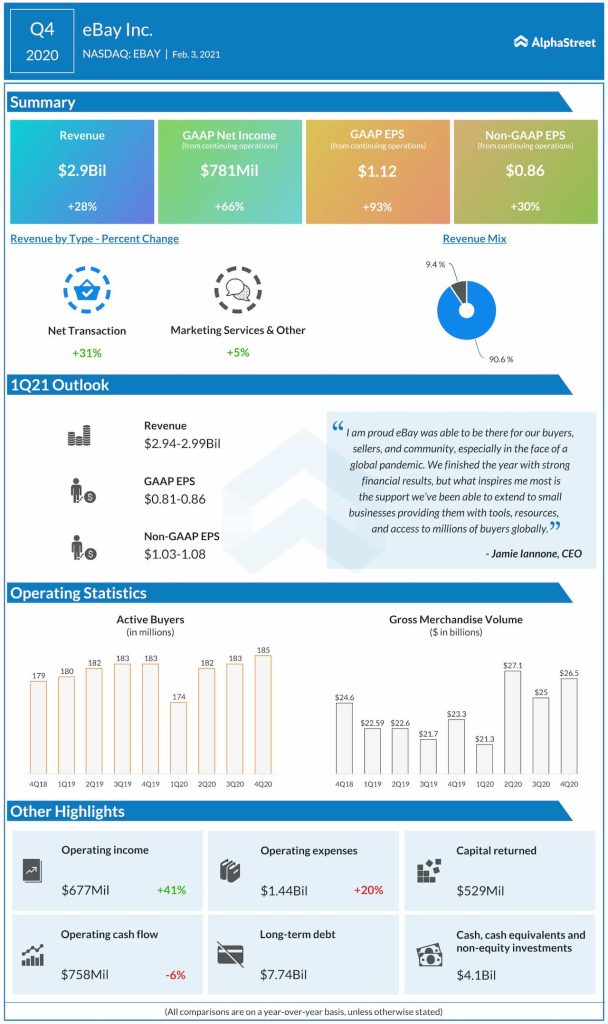

The financial performance of online marketplace eBay Inc. (NASDAQ: EBAY) has not been affected by the ongoing COVID crisis so far, rather the company consistently reported strong earnings that often topped the Street view.

Investing in EBAY

The Silicon Valley-headquartered e-commerce firm’s market value nearly doubled since the onset of the pandemic. While analysts have a positive view of the large-cap stock’s future performance, the sentiment is not strong enough to recommend buying it. While the reasonable valuation indicates there is still room to consider owing it, the stock can offer a better investment opportunity in the future, given its high volatility. It can be assumed that the stock’s future performance would be in line with the way eBay’s business evolves. Meanwhile, it is not the right time to sell.

Being a much sought-after destination for trading certifiable assets, eBay has managed to overcome most of the challenges the e-commerce market is facing. That should give the company a new lease of life, after a long period of stagnation. It is worth noting that the company owes the recent improvement in traffic to CEO Jamie Iannone’s innovative strategies, to some extent. That is significant considering the company’s not-so-impressive performance in recent years, especially when compared to peers like Amazon (NASDAQ: AMZN).

From eBay’s Q4 2020 earnings conference call:

“Our payments transition is on track and will largely be completed this year. Our advertising business will continue to outpace volume through promoted listings and other products. As we defend the core, we plan to expand our new vertical experiences to more markets and innovate in more categories. Today we’ve only just a single-digit percentage of our global GMV but in the coming years that will expand to a majority of the volume.”

Steady User Growth

The main operating segment, called Net Transaction, expanded by a third during the three months ended December 2020, driving up total revenues to about $3 billion. The top-line benefited from a further increase in the number of active buyers, which touched a record high of 185 million. Consequently, fourth-quarter adjusted profit rose 30% year-over-year to 86 cents.

Related: eBay Q4 2020 Earnings Call Transcript

The uptrend is expected to have sustained in the early months of the current fiscal year, thanks to managed payments and strong advertising revenue. For the rest of the year, a moderation in volumes from last year’s COVID-driven highs would make the comparisons bit difficult. The market will be looking for a 55% earnings growth when the company announces its first-quarter results early next month.

Stock Performance

Though the post-earnings rally in early February turned out to be short-lived, the stock recouped the loss quickly and is currently hovering near its peak. In the past twelve months, the shares often outperformed the market. They closed the last session slightly lower.