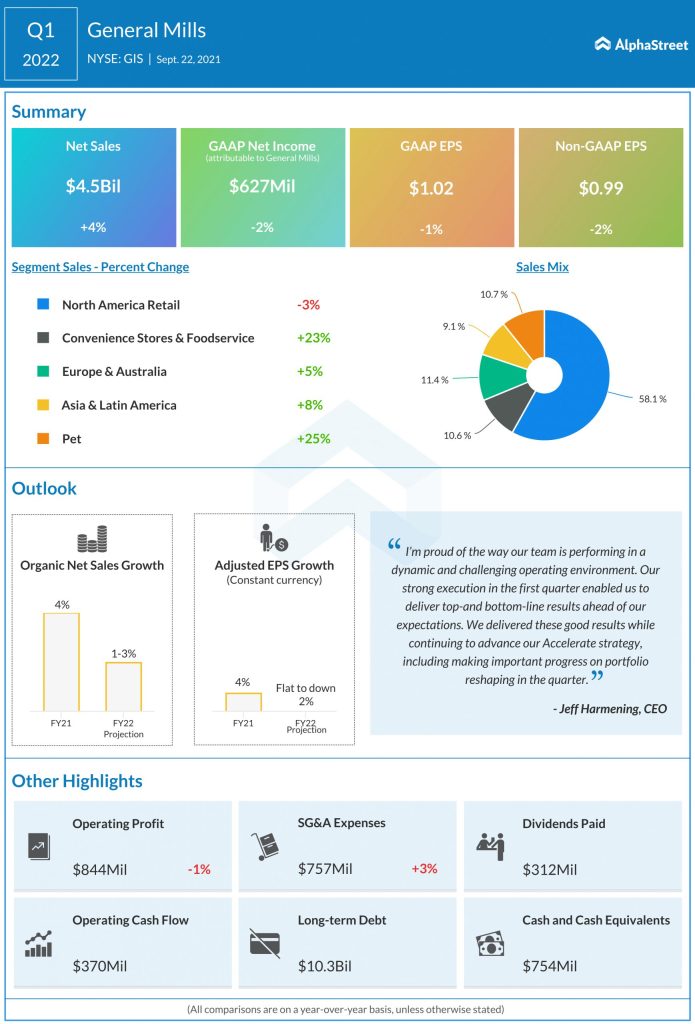

Shares of General Mills Inc. (NYSE: GIS) were up 3.2% on Wednesday after the company delivered better-than-expected results for the first quarter of 2022. Net sales rose 4% year-over-year to $4.5 billion, exceeding market estimates. Adjusted EPS amounted to $0.99, also surpassing expectations.

For the full year of 2022, General Mills expects organic sales to come in toward the higher end of its initial guidance range of a decline of 1-3%. Constant currency adjusted EPS is expected to be toward the higher end of the company’s initial guidance range of flat to down 2%.

Looking at the earnings report, here are three factors that can be expected to help drive growth for the company going forward:

Strong demand for pet food

General Mills believes the increase in the pet population and strong demand for pet food provides opportunities to drive further growth. In Q1, net sales for the Pet segment increased 25% YoY to $488 million. The Blue Buffalo brand continued to drive strong retail sales growth and market share gains during the quarter.

The pet treat brands which the company acquired from Tyson Foods (NYSE: TSN) posted a 20% growth in retail sales during the quarter. Dog Treats is the second largest segment in Pet Food with retail sales of $7 billion and it continues to grow at a high single-digit rate.

The recent acquisitions helped General Mills expand its portfolio, making it a leading player in the Dog Treats segment, and gave it a strong footing within the pet foods space. The company’s Pet segment now generates $2 billion in net sales with attractive margins and significant growth ahead.

Higher demand for food at home

General Mills expects demand for food at home to stay high relative to pre-pandemic levels. These pandemic-driven shifts in consumer behavior are expected to stay on as people continue to work from home and prefer to do their own cooking and baking.

Within North America Retail, despite declines in US Meals & Baking and US Cereal during the first quarter, sales rose 3% for US Snacks and 3% in constant currency in Canada. Net sales for US Yogurt were on par with year-ago levels.

In the Europe & Australia segment, net sales grew 5%, helped by sales increases for snack bars and yogurt. Within the Asia & Latin America segment, net sales increased 8%, driven by Yoki meals and snacks in Brazil and Haagen-Dazs ice cream in China.

Portfolio reshaping

In July, General Mills acquired Tyson Foods’ pet treats business which included the Nudges, True Chews and Top Chews brands. The acquisition will help the company solidify its position in the $37 billion US pet food category.

The company has also signed an agreement with Sodiaal to divest its European Yoplait operations. The transaction is expected to close by the end of calendar year 2021. These actions are expected to help drive more profitable growth going forward.

Click here to read the full transcript of General Mills’ Q1 2022 earnings conference call