One of the reasons behind the dominance of GoPro Inc. (NASDAQ: GPRO) in the action camera market has been the absence of direct competitors, but the entry of new players is changing the market dynamics. Interestingly, the monetary benefits of being a market leader are yet to fully reflect on the tech firm’s financial performance.

Also Read: Can Alphabet replicate the success of Search

Though GoPro’s positive third-quarter results lifted market sentiment slightly, the shares continue to languish at historical lows without showing any sign of bouncing back. Worse, the long-term prospects of the stock don’t look encouraging, with the average target price indicating continued weakness. In short, it is not the right time to invest in the single-digit midget, while those holding the stock can wait for further cues before selling.

A Big Bet

The company is counting on its HERO9 Black camera — which has been driving subscriber growth after the successful launch earlier this year — to take the business to the growth path. However, revenue contribution from the subscription business is low and that is unlikely to improve in the near future. When it comes to boosting the top-line, the company might need to attract mainstream customers, considering the rising competition from cheaper competitors.

Direct-to-Customer Push

Meanwhile, the ongoing innovation in the digital platform should help the company serve customers in an effective manner, thereby expanding the subscriber base further and raising gross margin, which has remained under pressure due to discounts and freebies. Despite the unfavorable factors, the company expects to remain profitable in fiscal 2020.

Commenting on direct-to-consumer efforts, GoPro’s CEO Nicholas Woodman said, “We’re able to fill more subscriptions and more value to the consumer. We’re seeing that in records in terms of revenue, and we’ll see that, again, I think in Q4. It’s expanding our margins, it’s expanding our cash flow, and diversifying, not so much yet on the revenue basis, but definitely on a margin and operating profit basis. The direct-to-consumer model is definitely helping along with the subscription benefit. So we see that continuing into 2021 and beyond.”

Bullish View

The executives do not see headwinds from the inventory imbalance either, going forward. The optimism comes from speculation that sales would remain unaffected by the COVID-related curbs on international travel, as customers might instead travel to local destinations and record their experiences using GoPro gadgets. It is also estimated that people would want to use the products even while they are confined to homes during the lockdown.

We expect to exit 2020 with low channel inventory positioning us well for 2021. Our direct-to-consumer subscription-centric approach is generating improved cash flow, margin, and LTV, while delivering a high-margin subscription revenue stream, we expect will have a positive impact on profitability in 2021.

Nicholas Woodman, chief executive officer of GoPro

Earnings Rebound

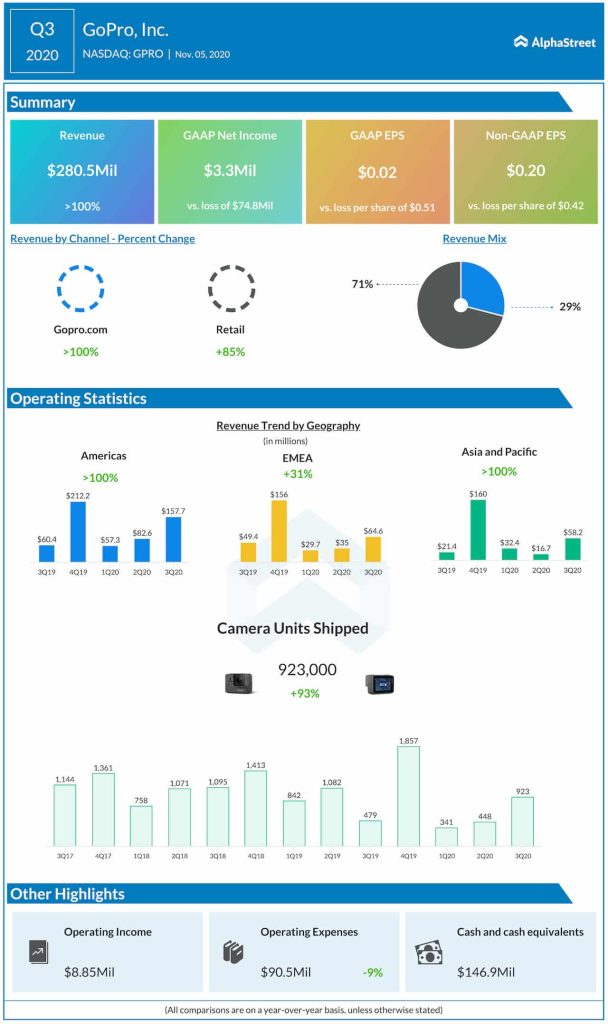

After incurring losses for two consecutive quarters, GoPro reported earnings of $0.20 per share for the most recent quarter from a loss of $0.42 per share a year earlier. Both the business segments registered strong growth and total revenues more than doubled to $281 million. It was the biggest growth since the fourth quarter of 2019 when revenues surged across all markets and operating segments.

Read management/analysts’ comments on quarterly reports

The stock has been trading below the $10-mark for more than three years, all along staying below its long-term average and underperforming the market. On the bright side, the value nearly doubled since the beginning of the year, with most of the gains coming after this week’s earnings report.