Home Depot, Inc. (NYSE: HD) has effectively tapped into the sharp increase in demand for home improvement during the pandemic while beating headwinds related to store closure and supply chain disruption. In the early weeks of the crisis, the retailer witnessed a sharp increase in customer traffic as people flocked to its stores for buying home remodeling and maintenance products.

Stock Peaks

After maintaining slow and steady growth over the past several months, shares of the Atlanta-headquartered home improvement company climbed to an all-time high recently. It seems to have peaked and is likely to stay flat in the coming weeks, offering a fresh buying opportunity. Analysts, in general, recommend buying HD. Meanwhile, the impressive dividend growth makes the stock a preferred choice for income investors. The company has returned around 15% of its market cap to shareholders in the past five years, in the form of share buybacks and dividends. Its return on equity has been well about the average so far this year and the trend is expected to continue, thanks to the booming housing market and elevated home prices.

Read management/analysts’ comments on Home Depot’s Q2 report

Meanwhile, the slowdown in do-it-yourself activities — a key growth driver that helped Home Depot emerge as a pandemic winner — due to market reopening and relaxation of movement restrictions points to a potential slowdown in its financial performance in the second half.

Road Ahead

When the company reports third-quarter results on November 16 after the closing bell, Wall Street will be looking for earnings of $3.34 per share — representing a 5% year-over-year increase — on revenues of $34.58 billion. Initial estimates show that top-line growth slowed in the second half, compared to the prior-year period when sales grew at a record pace. The resurgence of COVID-19 cases and the emergence of new variants will weigh on consumer spending, thereby dragging down sales. The other challenges include stiff competition, rising inflation, and continuing supply chain issues.

In the near term, we remain focused on being flexible and agile as we navigate this dynamic environment, but we also continue to leverage the momentum of our strategic investments to further enhance interconnected shopping experience in support of our goals to drive growth faster than the market in any environment, further strengthen our position as a low-cost provider in home improvement with a relentless focus on productivity and efficiency and deliver exceptional shareholder value.

Craig Menear, chief executive officer of Home Depot

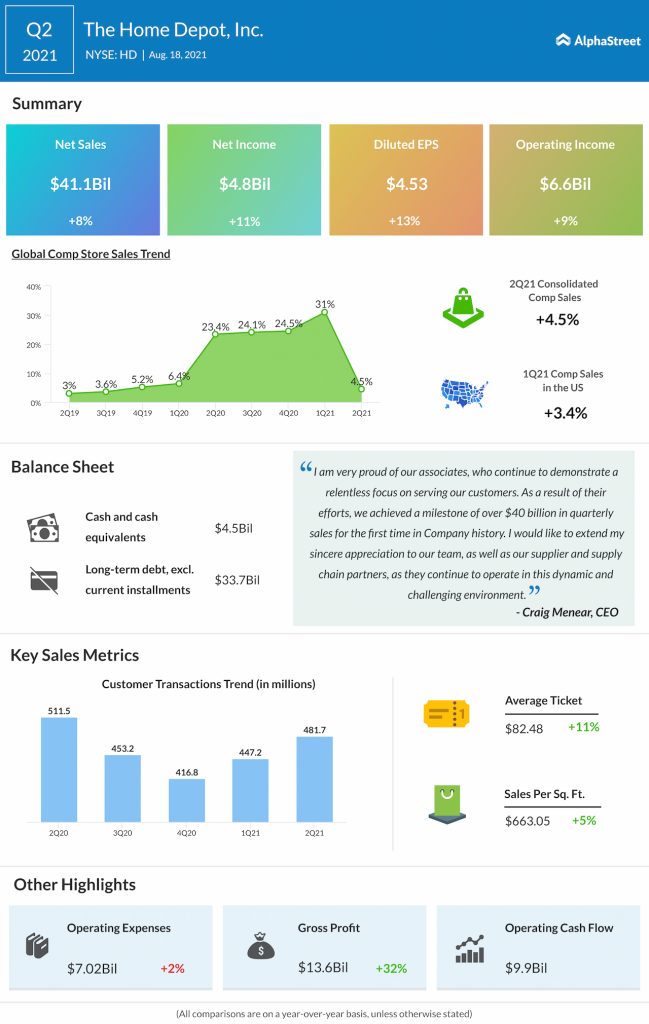

The company’s second-quarter performance was one of the best in terms of sales and profitability, but weakness in certain areas raised concerns that the boom time is probably over. Net sales rose 8% annually to a record high of $41.1 billion, resulting in a 13% growth in earnings to $4.8 billion. The numbers also came in above the market’s prediction. Meanwhile, customer transactions decreased about 6% during the quarter when comparable-store sales growth decelerated sequentially and fell short of expectations.

Competition

Home Depot enjoys an edge over its nearest rival Lowe’s Companies, Inc. (NYSE: LOW) on many fronts, including a stronger base of professional customers, a better economy of scale, and strong margins. After posting double-digit earnings growth for the July quarter, Lowe’s will be releasing third-quarter results on November 17.

COST Stock: These factors make Costco a good bet for the long term

Home Depot’s stock, which has gained about 9% in the past twelve months, mostly stayed above the 52-week average. It traded slightly higher early Monday, after closing the previous session at $372.18.