Shares of Starbucks Corporation (NASDAQ: SBUX) stayed in green on Thursday. The stock has gained 10% over the past 12 months. The company delivered healthy results for its most recent quarter although its performance was impacted by inflationary pressures as well as pandemic-related headwinds in China. Here are a few points to keep in mind if you have an eye on this stock:

Revenue

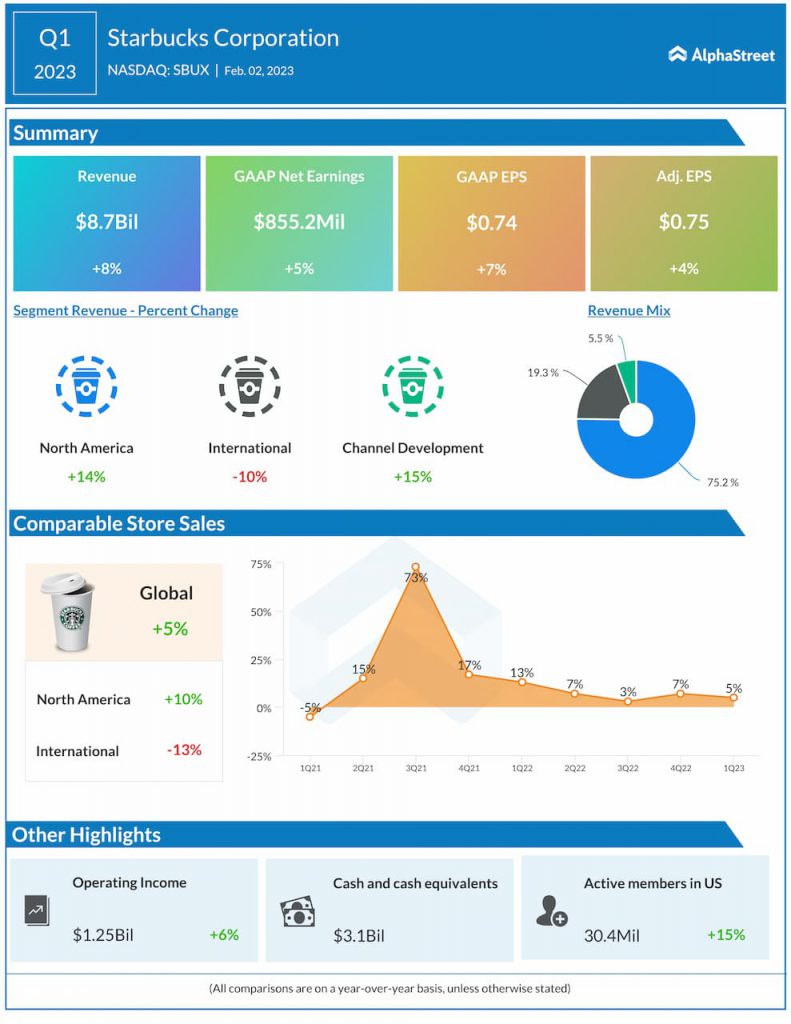

Starbucks generated consolidated revenues of $8.7 billion in the first quarter of 2023, which was up 8% year-over-year. Revenues in the North America segment increased 14% YoY to $6.6 billion. The company’s global comparable store sales grew 5% in Q1, driven mainly by a 7% increase in average ticket. Comparable store sales in North America and US increased 10%, fueled by a 9% growth in average ticket.

However, the company saw revenue in the International segment drop 10% to $1.7 billion, hurt by FX impacts, as well as a 13% decline in comparable store sales caused by pandemic-related disruptions in China. Excluding these impacts, revenue grew 25% and comps rose 11%.

Starbucks also saw its comparable transactions fall by 2% globally, with a 12% decline in international transactions. Even in North America, comparable transactions rose only 1% in the quarter.

Profits and margins

Starbucks’ GAAP EPS increased 7% to $0.74 in Q1 2023 compared to the year-ago quarter. Adjusted EPS grew 4% to $0.75. Meanwhile, operating margin on a GAAP basis dropped to 14.4% in Q1 from 14.6% in the prior-year period, mainly due to investments in wages and benefits, inflationary pressures and sales deleverage in China. Adjusted operating margin also dropped to 14.5% from 15.1% last year.

Store fleet

Starbucks continues to expand its store fleet. The company opened 459 net new stores during the first quarter of 2023. It ended the quarter with 36,170 stores worldwide, of which 51% were company-operated and 49% licensed.

The North America segment had a store count of 17,381 at quarter-end, representing new store growth of 3%. The International segment ended the quarter with 18,789 stores, reflecting new store growth of 8%.

At the end of the first quarter, stores in the US and China made up 61% of Starbucks’ global portfolio. The company had 15,952 stores in the US and 6,090 stores in China. Starbucks aims to have 9,000 stores in China by the end of 2025.

Outlook

Starbucks expects to see negative comps in China through the second quarter of 2023 followed by an improvement during the remainder of the year. Its store growth plan for China remains unchanged as the company continues with its strategy to expand in new cities.

Starbucks expects its operating margin to decline sequentially in Q2, mainly due to the headwinds in China. Margins are anticipated to improve during the latter half of the year with sequential improvements in the third and fourth quarters. Margin expansion is expected to be supported by sales leverage, pricing, productivity gains, and a recovery in China. Starbucks expects a similar trend for EPS as well with a sequential drop in Q2 followed by a meaningful pick-up during the second half.