AlphaStreet Newsdesk powered by AlphaStreet Intelligence

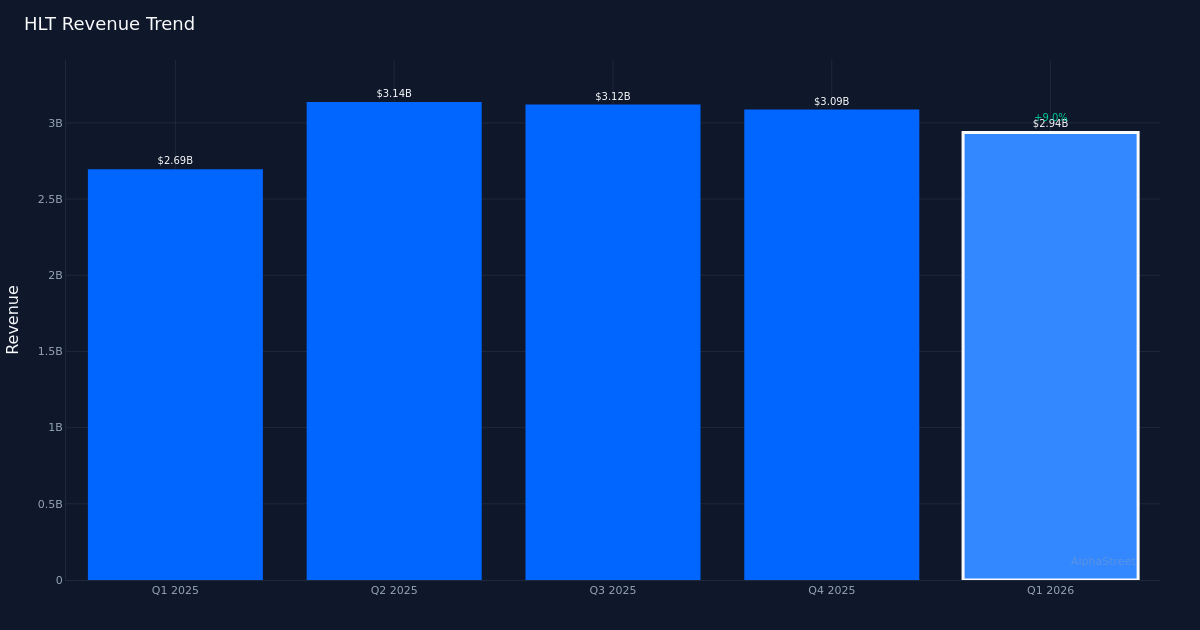

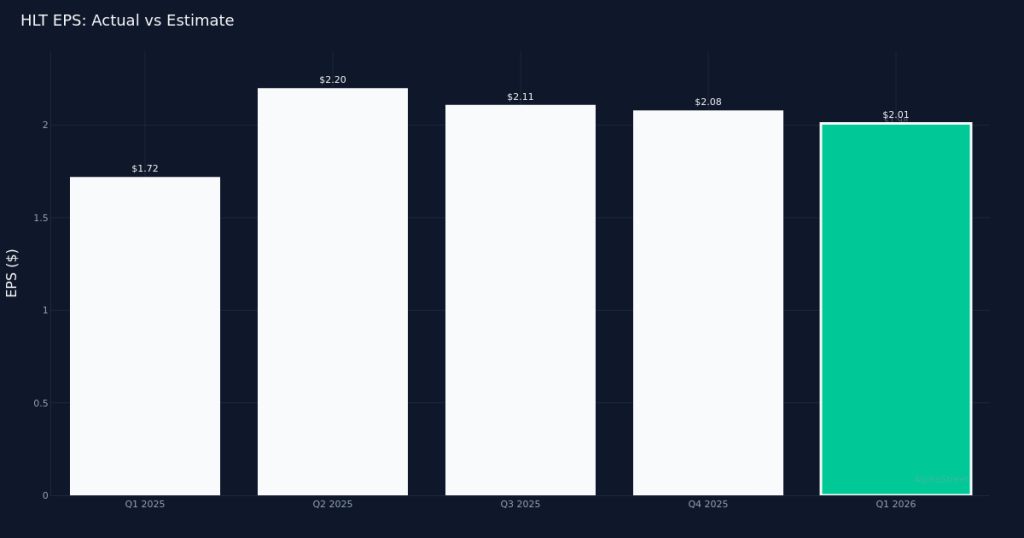

Modest earnings beat. Hilton Worldwide Holdings Inc. (NYSE:HLT) posted Q1 2026 adjusted EPS of $2.01, topping Wall Street’s $1.98 estimate by 1.5% in a quarter that demonstrated the lodging giant’s continued ability to extract revenue growth from its asset-light franchise model. The company generated $2.94B in revenue for the quarter, up 9.0% from $2.69B in Q1 2025, while adjusted net income reached $466.0M.

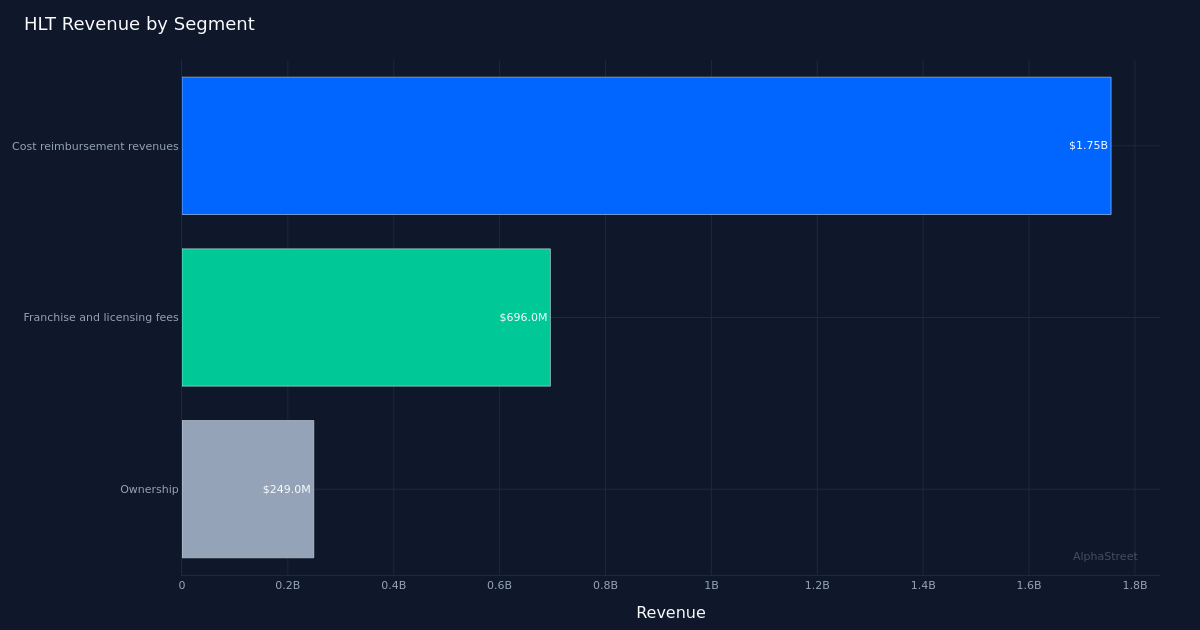

Revenue quality strong. The earnings beat appears fundamentally sound, driven by top-line momentum rather than aggressive cost management. System-wide comparable RevPAR growth of 3.6% on a currency neutral basis reflects healthy underlying demand across Hilton’s global portfolio of 9,260 properties. The franchise and licensing fees segment, which generated $696.0M in revenue for the quarter, continues to serve as the company’s highest-margin revenue stream and underscores the strength of Hilton’s capital-efficient business model. This revenue mix—weighted heavily toward franchise fees rather than owned real estate—typically commands premium multiples from institutional investors given its scalability and cash generation characteristics.

Guidance suggests confidence. Management’s full-year outlook projects FY 2026 GAAP EPS of $8.28 to $8.40, a range that implies continued double-digit earnings growth as the company benefits from both unit expansion and same-property revenue gains. The midpoint of this guidance band suggests management sees the momentum from Q1 as sustainable throughout the year, though the relatively tight range indicates limited visibility into potential upside scenarios. With the quarter’s 3.6% RevPAR growth running ahead of many industry forecasts entering the year, Hilton appears positioned to capture share in an increasingly competitive global lodging market.

Muted stock reaction. Shares traded largely unchanged despite the earnings beat, indicating the results landed squarely in line with buy-side expectations that had likely crept higher ahead of the print. The sell-side community remains constructive but not overwhelmingly bullish, with Wall Street consensus standing at 12 buy ratings, 14 hold ratings, and 1 sell rating. This cautious positioning suggests analysts are weighing Hilton’s consistent execution against valuation concerns and questions about how much further RevPAR can expand in a maturing cycle.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.