Campbell Soup Company (NYSE: CPB) benefited significantly during the COVID-19 pandemic period as people staying indoors stocked up on its soups and snacks products and turned to preparing more meals at home. While the company believes the customers it gained during the health crisis are likely to stay on with it after the pandemic subsides, there are concerns that food companies in general are going to see their momentum wane once vaccines are distributed and things go back to normal.

Quarterly performance

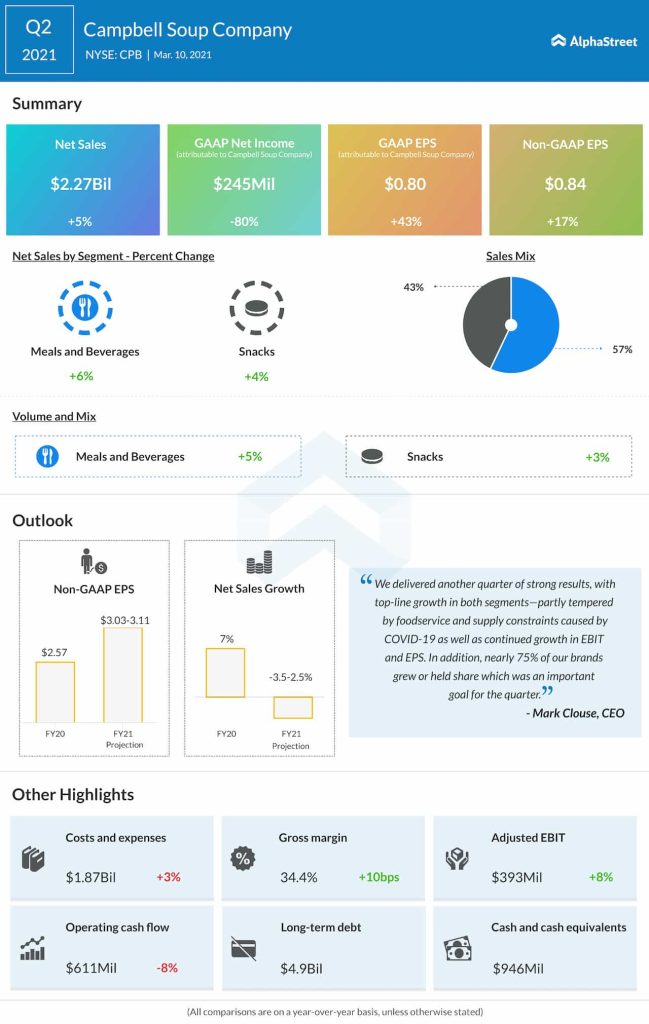

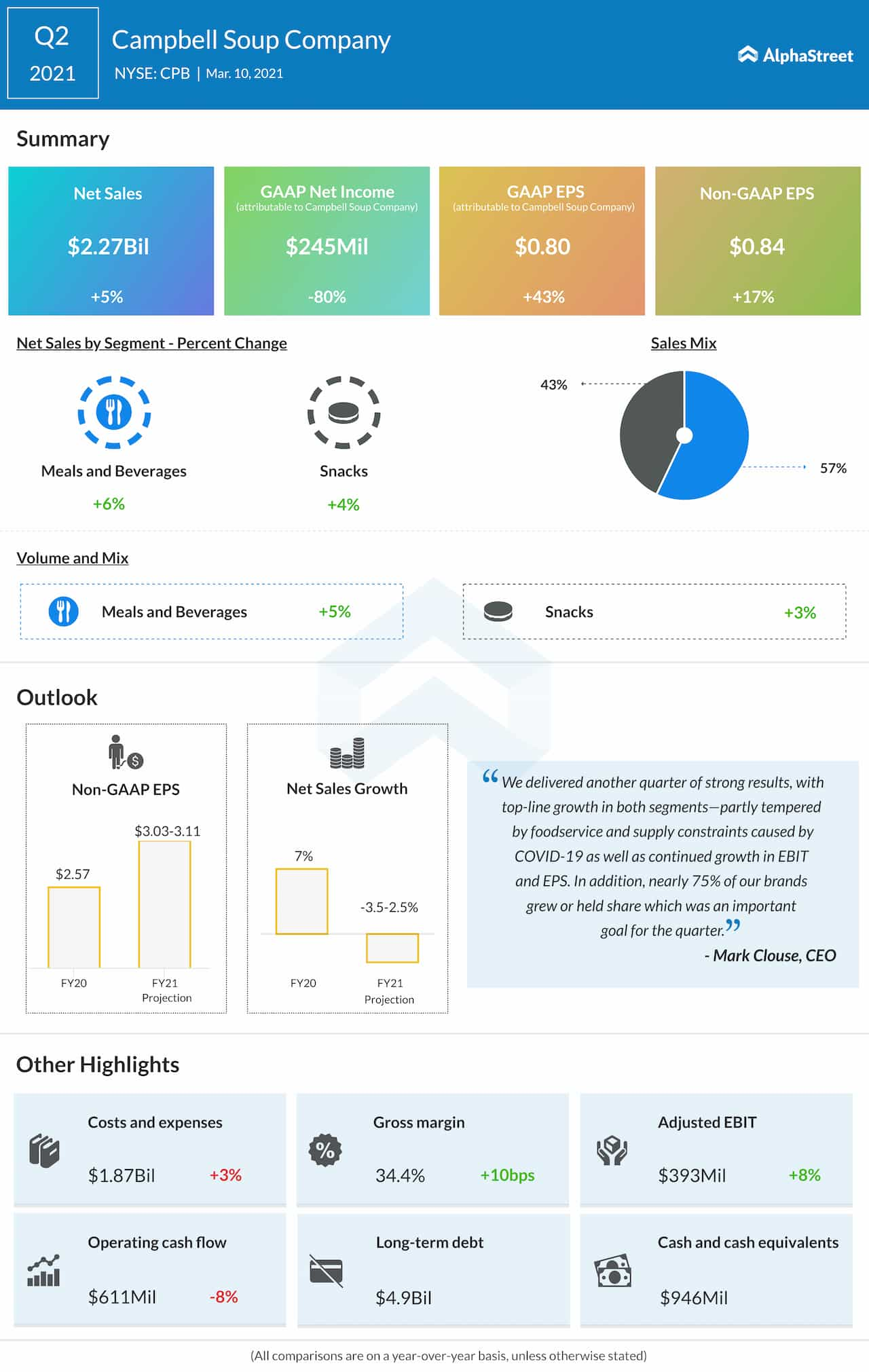

In the second quarter of 2021, net sales rose 5% year-over-year, both on a reported and organic basis, to $2.27 billion. Adjusted EPS increased 17% to $0.84. While earnings surpassed projections, revenue fell short of expectations. The top line benefited from an increase in volume and mix driven by strong demand due to higher at-home food consumption. However, the foodservice business remained challenged due to impacts from the pandemic.

Demand trends

In Q2, Campbell’s Meals & Beverages segment delivered a growth of 6% driven by strength in soups, beverages, pasta, and pasta sauces. The Snacks segment grew 4% helped by high demand for salty snacks like potato chips and popcorn. The company witnessed strong momentum in its V8, Prego, Kettle Brand, Late July, Cape Cod, Pop Secret and Pepperidge Farm brands which grew market share and increased household penetration during the quarter.

Campbell managed to hold or increase market share across nearly 75% of its portfolio during the quarter. The company’s online channel was instrumental in driving growth helped by the addition of the click-and-collect fulfillment model. In-market dollar consumption rose 89% year-over-year in Q2.

The soups category performed well, with particular strength in condensed soups, which grew sales in the double-digits and continued to gain market share in the quarter. During the holiday season, Campbell saw the number of buyers of condensed cooking soups increase double-digits. The category also benefited from the addition of new products such as canned offerings and plant-based products.

On its quarterly conference call, Campbell stated that based on its research, nearly 13 million new households purchased its soup products since the initial peak of the pandemic and with the emergence of quick-scratch cooking, more than 30% of the consumers are cooking more with soup since the start of the pandemic.

The company believes that as work-from-home is likely to continue post-pandemic, at-home food consumption is set to prevail going forward, thereby benefiting the Meals & Beverages segment. The Snacks segment, which makes up around 50% of annual revenues, will also benefit from this trend as nearly 30% of lunches are accompanied by snack foods.

Outlook

Despite the optimism expressed by the company, there are concerns that as vaccines are distributed and people start venturing out, at-home food consumption will gradually begin to decrease. Campbell has guided for full-year 2021 net sales to decline in the range of 2.5-3.5%, reflecting the cycling impact of the pandemic-related spike in demand seen during the back half of 2020.

However, as the trend of dining out gains speed, the company can be expected to see a recovery in its foodservice business. It can be assumed that Campbell might be able to retain some of the pandemic-related momentum in the near term before life goes back to normal and the pace begins to moderate.

Click here to read the full transcript of Campbell Soup Q2 2021 earnings conference call