AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street targets double-digit growth. Analysts are looking for Hubbell Incorporated (NYSE:HUBB) to deliver earnings of $3.86 per share on revenue of $1.50B when the electrical equipment manufacturer reports first-quarter 2026 results on April 30. The consensus represents the midpoint of 13 analyst estimates, with EPS projections ranging from $3.63 to $4.04 and revenue forecasts spanning $1.50B to $1.52B. The Street’s expectations call for continued momentum in both top- and bottom-line performance as the company navigates infrastructure investment cycles and utility grid modernization trends.

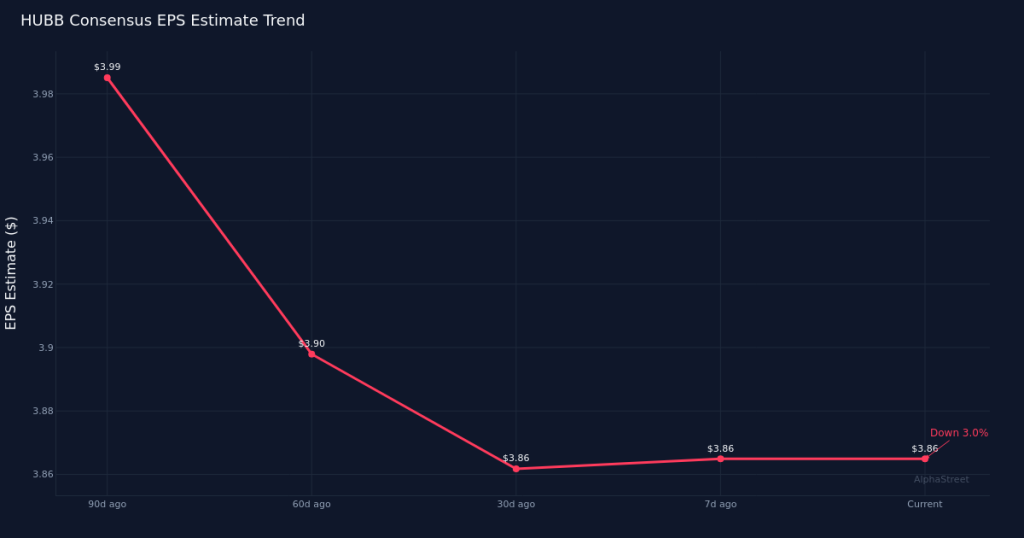

Estimates have edged lower over recent months. While the EPS consensus has held steady over the past 30 days at $3.86, the 90-day view reveals a downward drift of 3.3% from $3.99. This gradual reduction in analyst expectations suggests some tempering of optimism entering the quarter, though the magnitude remains modest. The revision pattern may reflect concerns about input costs, project timing, or macroeconomic headwinds affecting electrical equipment demand, though analysts have largely maintained their overall constructive stance on the company’s near-term trajectory.

Year-over-year comparisons point to solid growth. The consensus EPS estimate of $3.86 would represent growth of 10.3% compared to the year-ago result of $3.50, while the revenue target of $1.50B implies expansion of 9.5% from $1.37B in the first quarter of 2025. Last year’s quarter delivered net income of $181.9M on a net margin of 13.3%, establishing a profitability baseline against which investors will measure operational efficiency this time around. The implied growth rates suggest Hubbell is expected to sustain momentum in both volume and pricing power across its electrical solutions portfolio, though the margin trajectory will be critical given the erosion in analyst estimates over the past three months.

Electrical infrastructure tailwinds support the setup. Hubbell operates in the electrical equipment and parts sector, positioning it to benefit from secular trends including utility grid hardening, renewable energy integration, data center expansion, and industrial electrification. The company’s portfolio spans utility solutions and electrical systems, serving both the power generation and distribution markets as well as commercial and industrial end customers. Demand drivers in these segments have been robust as utilities invest in aging infrastructure and enterprises upgrade electrical systems to handle increased power loads, though lead times and project phasing can create quarterly volatility.

Profitability progression merits attention. The year-ago net margin of 13.3% provides context for evaluating whether Hubbell can maintain or expand profitability amid the anticipated revenue growth. With the EPS growth rate of 10.3% running slightly ahead of the implied revenue expansion of 9.5%, the forecast embeds modest operating leverage. Investors will scrutinize whether this reflects pricing discipline, favorable product mix, productivity initiatives, or simply a lighter cost backdrop, particularly given the estimate cuts observed over the 90-day window.

Track record and sentiment frame expectations. Understanding how frequently Hubbell beats or misses consensus will be important for gauging whether the current estimates incorporate an appropriate margin of safety, though historical beat rates provide only one lens for evaluating the setup. The stability in 30-day estimates contrasts with the 90-day decline, suggesting analyst conviction has recently firmed even as longer-term views were recalibrated downward. This dynamic leaves the quarter with a mixed sentiment profile heading into the print.

Execution and guidance will drive the stock reaction. Beyond the headline numbers, investors will focus on segment performance across utility and electrical solutions, order book trends, pricing realization, and management’s commentary on project pipelines and bidding activity. Any updates on supply chain dynamics, input cost pressures, or margin sustainability will be critical given the year-over-year profitability comparison. Forward guidance for the remainder of 2026 will likely carry more weight than the Q1 result itself, particularly if management addresses the factors behind recent estimate revisions.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.