International Business Machines Corporation (NYSE: IBM), which has long been a market leader in the technology industry, embarked on a transformation drive a few years ago and shifted focus to cloud computing to better align the business with technological advancements and widespread adoption of cloud technology.

The Armonk-headquartered tech giant’s stock hit a new record this month, after gaining an impressive 23% in the past six months. The new peak is significant because it comes after a series of stock splits. IBM is a dividend aristocrat liked by income investors, offering a solid yield of 4.5% which is above the S&P 500 average. The upbeat sentiment over the company’s resilient performance and strong growth prospects indicate that the stock has more room to grow.

On Track

IBM’s legacy mainframes are among the widely used data servers. Continued product innovation and launch of new models, which lead to regular customer upgrades, catalyze revenue growth. The uptrend will likely continue in 2024, aided by the integration of AI and continued growth in partnerships. After an extensive reorganization, marked by M&A activities like the separation of infrastructure service business Kyndryl and the acquisition of Red Hat, IBM is more of a cloud and AI company now, than a traditional technology firm.

At the same time, IBM faces stiff competition in the areas of enterprise cloud and AI from the likes of Microsoft, and Amazon, which are also the company’s partners. It ended the third quarter with an impressive free cash flow of $1.7 billion, but the relatively high debt is a concern for stakeholders.

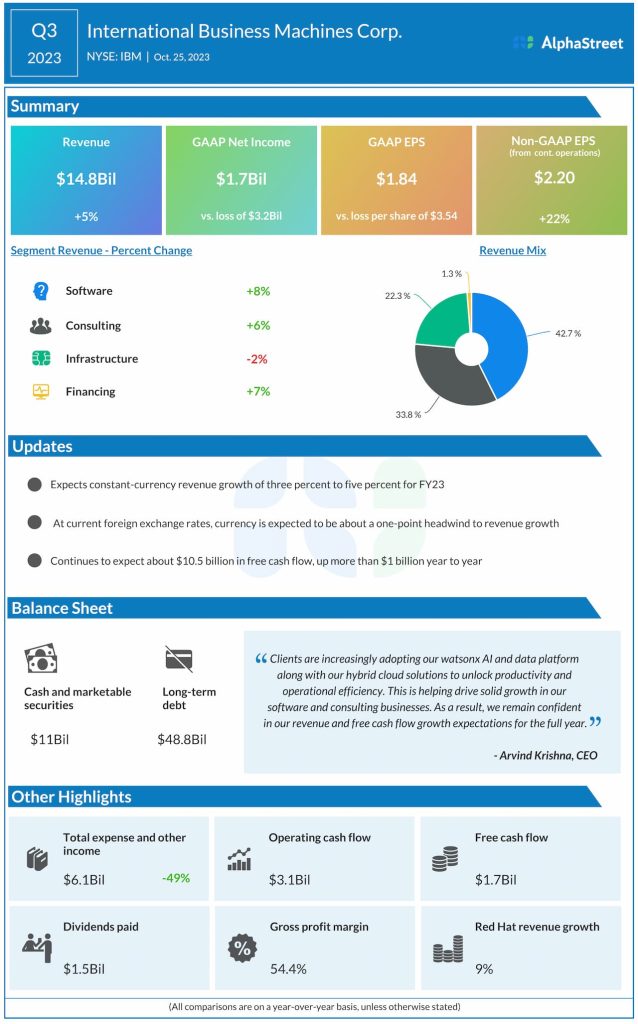

Good Show

In the third quarter, the tech firm’s revenues increased 4.6% year-over-year to $14.8 billion and rose 3.5% at constant currency. The outcome was broadly in line with analysts’ estimates. Adjusted earnings climbed 22% from last year to $2.20 per share during the three months. On a reported basis, net income was $1.7 billion or $1.84 per share in Q3, vs. a net loss of $3.2 billion or $3.54 per share last year. Earnings beat estimates, as they did every quarter in the past three years.

From IBM’s Q3 2023 earnings call:

“Our overall growth reflects our ability to help clients leverage data and AI for competitive advantage, automate IT environments, and seamlessly integrate hybrid cloud solutions. We also continue to position our business for the future, launching new products and offerings, forging, and expanding key partnerships, investing in talent and skills, and focusing our portfolio. We have been taking concrete actions to deliver productivity in our own business. All of this results in an IBM that is aligned to our clients’ most pressing needs and has a stronger financial profile.”

Outlook

The management estimates that revenue will grow 3-5% in fiscal 2024, at constant currency. It is looking for full-year free cash flows of about $10.50 billion, which is up $1 billion year-over-year. The company will be reporting fourth-quarter results on January 24, after the closing bell. Analysts expect adjusted earnings to rise to $3.75 per share in Q4 from $3.60 per share last year, on revenues of $17.22 billion.

With only a few days left in 2023, shares of IBM have gained 13% since the beginning of the year and are trading well above the long-term average. After opening Friday’s session higher, the stock maintained the momentum during the day.