AlphaStreet Newsdesk powered by AlphaStreet Intelligence

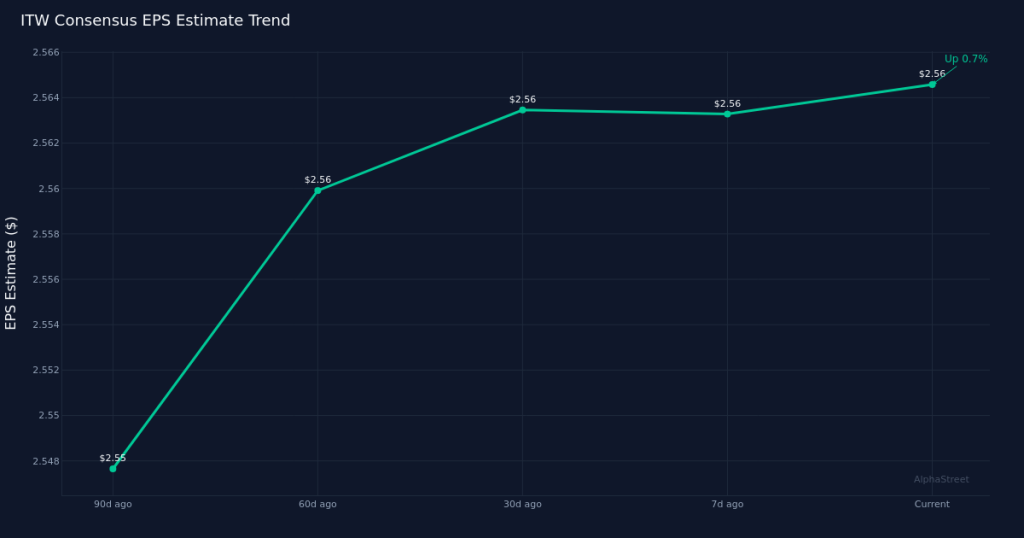

Wall Street expects Illinois Tool Works to deliver sequential growth as the diversified industrial manufacturer reports Q1 2026 results on April 30th. The consensus among 14 analysts calls for earnings of $2.56 per share on revenue of $4.01B. Estimate ranges are tight, with EPS projections spanning $2.53 to $2.60 and revenue forecasts between $3.96B and $4.07B, suggesting relatively uniform expectations across the Street.

Analyst sentiment has shown modest upward drift over the past three months but has flatlined recently. The EPS consensus has climbed up 0.4% over the past 90 days from $2.55, indicating a gradual upgrade cycle as analysts incorporated incremental improvement into their models. However, the 30-day drift shows down 0.0% movement from $2.56, signaling that expectations have stabilized heading into the print with no last-minute adjustments to estimates.

The consensus implies solid year-over-year expansion across both the top and bottom lines. Compared to Q1 2025 results of $2.38 per share on revenue of $3.84B, Wall Street is modeling implied EPS YoY change of +7.6% and implied revenue YoY change of +4.4%. This growth profile would represent meaningful operating leverage if achieved, with earnings expanding at nearly double the rate of revenue growth. A year ago, the company generated net income of $700.0M, translating to a net margin of 18.2%, establishing a high bar for profitability that investors will scrutinize when evaluating margin performance in the upcoming quarter.

The specialty industrial machinery sector backdrop presents a mixed environment for Illinois Tool Works heading into the report. As a diversified manufacturer serving end markets spanning automotive, food equipment, test and measurement, welding, and polymers, the company’s performance serves as a proxy for broader industrial demand. The year-over-year comparison becomes particularly relevant given that Q1 2025 represented a period when many industrial markets were navigating inventory corrections and uncertain capital spending. The implied growth rates suggest Wall Street believes those headwinds have eased, though the relatively modest revenue expansion indicates analysts aren’t expecting a dramatic cyclical inflection.

Margin trajectory will be a critical focus given the divergence between revenue and earnings growth rates. The implied earnings growth of +7.6% on revenue growth of +4.4% suggests analysts are building in margin expansion, whether through the company’s ongoing enterprise initiatives around operational excellence, favorable mix shifts across its seven segments, or pricing discipline holding despite potential volume softness in certain end markets. The year-ago net margin of 18.2% provides the baseline against which investors will evaluate profitability trends, particularly as industrial companies navigate the balance between volume recovery and maintaining pricing gains achieved during previous inflationary periods.

Illinois Tool Works operates a portfolio model with exposure across multiple industrial verticals, making segment-level performance critical to understanding the overall narrative. The automotive OEM business, test and measurement equipment, welding systems, and food equipment divisions each serve distinct demand drivers, from vehicle production schedules to restaurant capital spending to infrastructure investment. Investors will dissect which segments are accelerating, which are stabilizing, and where persistent weakness may be offsetting strength elsewhere in the portfolio.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.