International Business Machines Corporation (NYSE: IBM) has been busy streamlining its business over the past decade, divesting underperforming assets and giving importance to high-value products and services. From a legacy technology company, it has grown into a leading provider of cloud computing, mainframe and security services to top enterprises.

Stock Up

For IBM’s stock, it has been a roller-coaster ride for quite some time. It bounced back from a one-year low a few months ago and entered an upward spiral after the last earnings release. IBM is trading comfortably above its 52-week average, outperforming the market. With the factors behind the recent uptrend still in place, the stock is unlikely to withdraw in the near future. For those who missed the opportunity last year, it’s time to add the stock to their portfolios. However, short-term traders might be disappointed.

Also Read: International Business Machines Corporation’s Q3 2022 Earnings Call Transcript

When it comes to the use of cash, returning capital to shareholders has been a key priority for the company. Over the past ten years, it has reduced the number of outstanding shares by a fifth through share buyback program. Also, IBM has raised the dividend consistently, and currently offers a yield of around 5%. Last month, the shares once again crossed the $150 mark, before entering 2023 on a low note.

From IBM’s Q3 2022 earnings conference call:

“We generated $4.1 billion in the first three quarters, that’s up over $900 million year-to-year. We’re wrapping on payments related to the Kyndryl separation and the 2020 structural actions in driving working capital efficiencies. In terms of uses of cash in the first three quarters, we invested over $1 billion in the acquisition, which was more than offset by proceeds from divested businesses. And we returned nearly $4.5 billion to shareholders in the form of dividends.”

New Strategy

Reflecting the growing competition and new trends in the tech landscape, the century-old company recently lost the top spot in the US patent league table to Samsung, after staying there for about three decades. It seems to be shifting focus to expanding the portfolio, rather than maintaining the patent leadership. The company is all set to acquire technology company Octo, which provides digital transformation services exclusively to the federal government.

The strategy complements the management’s restructuring initiative, under which the company spun off its legacy IT infrastructure business a few years ago to focus more on high-growth areas like artificial intelligence and cloud computing. More recently, the company separated its managed infrastructure services business.

Stock Analysis: Why this blue-chip stock is a must-buy for 2023

Over the past six years, IBM’s quarterly earnings either exceeded or matched estimates regularly, making it one of the best-performing tech firms in relation to analysts’ estimates. It is estimated that the company would report a 7% growth in adjusted earnings when it announces fourth-quarter results on January 25 after the market closes. However, net revenue is expected to dip 2% annually to $16.37 billion. Going by the long-term trend, it is very likely that the results would beat forecasts.

Key Numbers

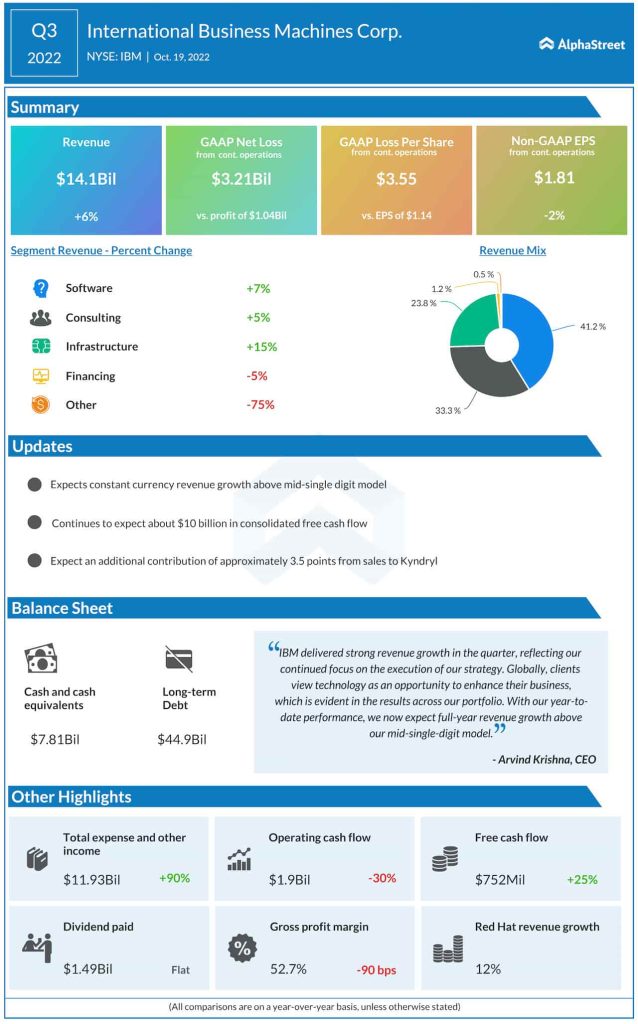

In the three months that ended September 30, all three operating segments registered growth, lifting total revenues by 6% to $14 billion. However, the bottom line was negatively impacted by a sharp increase in expenses, and earnings per share from continuing operations declined by 2% to $1.81.

Shares of IBM closed the last session up by around 2.5 dollars and traded higher in the early hours of Monday’s session. They gained about 2% in the first week of the year.