The Home Depot (NYSE: HD), a leading home improvement retailer, this week reported mixed results for the second quarter of 2024. The company’s stock dropped soon after the announcement — the better-than-expected numbers failed to impress the market as investor sentiment was hurt by the management’s cautious guidance. Of late, sales have been under pressure due to cautious consumer spending amid inflation concerns and macroeconomic uncertainties.

The current price of HD is broadly unchanged from its value four months ago, but it is down 10% from the March peak of $395.20. The stock gained momentum on Wednesday, recovering from the post-earnings dip. Over the past several years, the company has regularly raised its dividend, currently offering an above-average yield of 2.8%, which continues to attract income investors.

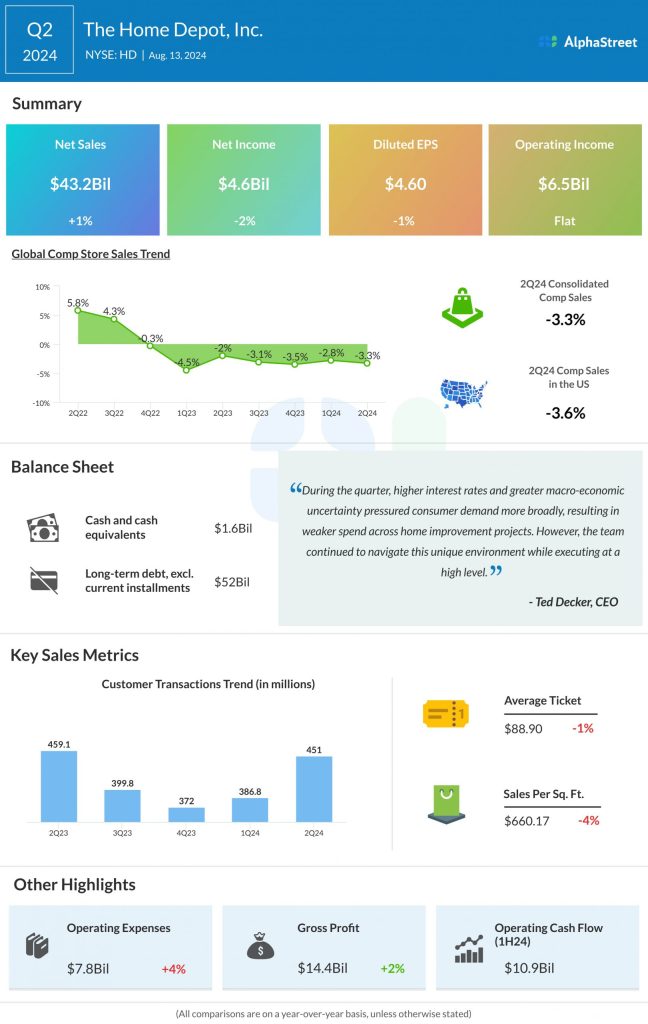

In the July quarter, Home Depot’s revenue beat estimates, after missing in the previous quarter. Net sales edged up 1% from last year to $43.2 billion in Q2, while earnings dropped modestly to $4.6 per share. The bottom line beat estimates for the fifth straight quarter. With a 3.3% year-over-year decline, global comparable store sales dropped for the seventh time in a row. The top line was negatively impacted by weakness in consumer spending and continued softness in Spring projects due to extreme weather changes.

Guidance

For fiscal 2024, the management now expects comparable sales to decline in the 3-4% range from last year, which is revised from the earlier estimate for a 1% decline. The weaker guidance reflects softening demand as customers postpone their purchases due to inflation and elevated interest rates. It is worth noting that do-it-yourself customers, individuals who own houses, account for a major chunk of the company’s business. Since the Federal Reserve is expected to cut interest rates later this year, people would want to wait until the next monetary policy meeting before taking up major home improvement projects.

In the whole of fiscal 2024, unadjusted and adjusted earnings are seen declining 2-4% and 1-3%, respectively. Meanwhile, Home Depot is expected to benefit from contributions from recently acquired SRS Distribution, a supplier to landscaping and roofing businesses, in the second half. So, the company currently expects total sales to increase between 2.5% and 3.5% in FY24.

From Home Depot’s Q2 2024 earnings call:

“The fundamentals of the home improvement market remain strong, and we have significant growth opportunities in front of us. We are gaining share-of-wallet with our customers, whether they are shopping in our stores, on our digital assets, or through our Pro Ecosystem. Our merchants, store and MET teams, supplier partners, and supply chain teams are always ready to serve in any environment. They did an outstanding job delivering value and service to our customers throughout the quarter…”

Expansion

During the quarter, Home Depot completed the acquisition of SRS Distribution for about $18 billion. The company expects the buyout to be complementary and additive to growth in the near term, with the potential to raise the total addressable market to around $1 trillion.

In the past 30 days, shares of Home Depot have stayed above their twelve-month average. They traded up 2.5% on Wednesday afternoon.