These days, the Internet has such a huge influence on people’s lives that it has become a one-stop destination for all solutions. It is natural that even to get inspired, people turn to cyberspace — a service Pinterest, Inc. (NYSE: PINS) has been providing successfully. Like its peers, the image-sharing platform is witnessing an increase in traffic ever since the shelter-in-place orders came into effect.

After last week’s post-earnings rally, Pinterest’s stock has probably reached its peak. Analysts are a bit cautious in their recommendations and have assigned the stock moderate buy rating, with a target price that represents an 8% downside.

Keeping Pace

The San Francisco, California-based company has been constantly innovating since going public last year so as to compete effectively with rivals like Snap, Inc. (SNAP). The entry of new players into the photo-sharing space – the latest being Google’s (GOOG) Keen app — has resulted in an increase in competition.

[irp posts=”67148″]

Pinterest is rapidly evolving into a platform that offers ideas on a wide range of topics — from do-it-yourself tips to interesting cooking recipes. There has been a marked improvement in its liquidity position that helped the platform remain debt-free – something that will help it continue investing in content, ads diversification, and use-case expansion.

Growing Ad Demand

Advertiser demand has increased since the early days of the pandemic, and the momentum is expected to gather steam as the macro conditions improve. Advertisers are benefitting from measures adopted by Pinterest’s management to optimize conversion. The online shopping feature has been a big hit among both advertisers and Pinners.

Going by the current trend, it seems that online shopping would be a key revenue driver going forward. The company expects to benefit from advertisers boycotting mainstream social media platforms like Facebook (FB), though it would likely be a short-term movement. The executives are also seeing opportunities in the untapped Latin American market.

We’ve shipped shopping-only surfaces and engagement with those surfaces up to 50% in the first half of 2020. And we’re also seeing more product-only searches, which have grown by 8 times in 2020. As you know, from previous calls our strategy in shopping is to make these surfaces, but to also make sure that they’re filled with highly relevant products.

Ben Silbermann, chief executive officer of Pinterest

Lingering Concerns

With the COVID situation not showing any signs of improvement, there are concerns that advertising demand might weaken if the authorities impose more lockdowns. The back-to-school season, which typically falls in the third quarter, is an important period for Pinterest’s business. But, the advertising prospects look bleak this season due to the shift to distance learning. In short, year-over-year comparisons will be difficult in the remainder of the year, due to the unusual market scenario.

“I don’t know what the fall will hold in terms of future lockdowns, but what we’re seeing is a rise in cases and the prospect of potentially slower store reopenings, less economic activity, and possibly just that uncertainty, in general, is something we need to factor in. What we’re hearing from retail and advertisers, they have a shorter leash on their budget commitments right now, there are store closures in place and possibly more coming,” said chief financial officer Todd Morgenfeld while replying to analysts’ questions at the second-quarter conference call.

Having initiated its cost-reduction program much earlier than originally planned, the company is continuing with the capital investment plan while also increasing the headcount, at a time when most businesses are in the rightsizing mode.

Elusive Profit

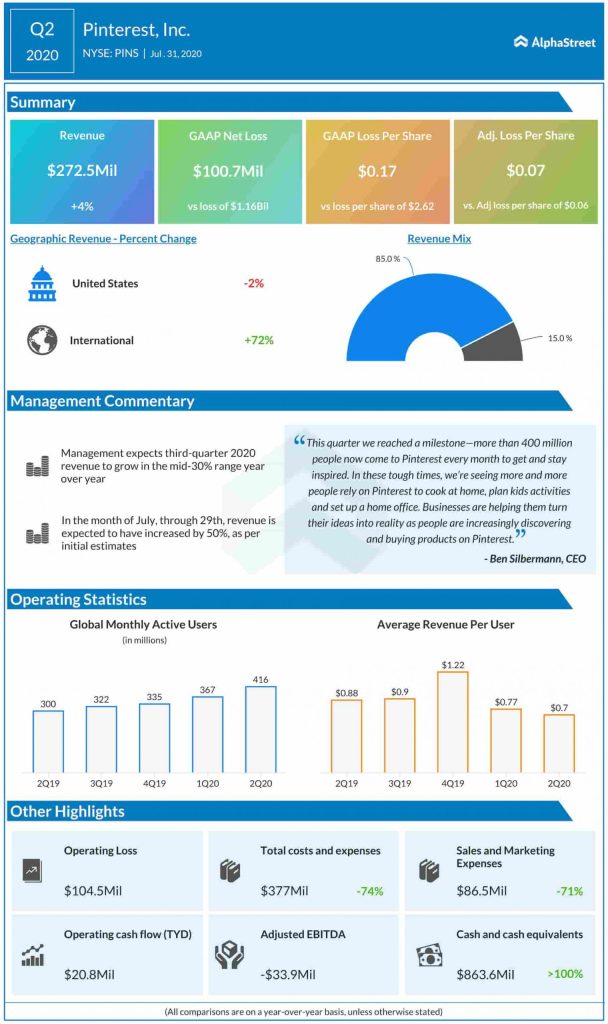

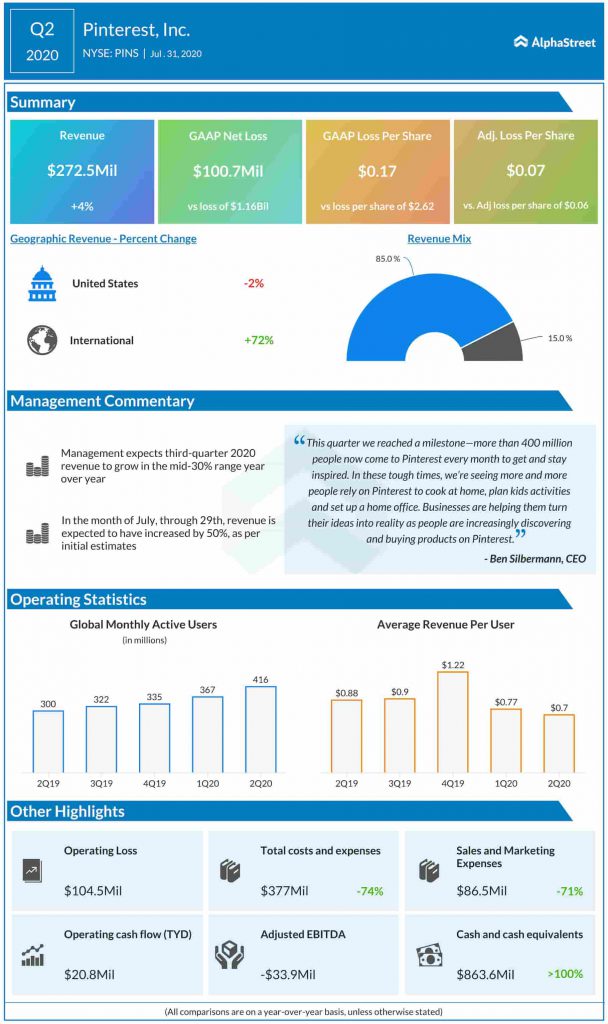

Pinterest remained in a loss in the second quarter though revenues moved up by 4% to $273 million as a modest weakness in the United States was more than offset by a sharp increase in traffic in the overseas market. It was much better than the outcome experts had predicted.

Initial estimates show that revenues grew in double digits so far in the current quarter, with the number of monthly active users crossing 400 million for the first time. The management expects revenues to grow in the mid-30s percent range year-over-year in the third quarter.

The impressive quarterly numbers brought cheer to investors last week and shares of the company climbed the highest level since the early weeks of its IPO. The stock gained about 50% in one week alone, continuing the steady uptrend that started in early March. Pinterest’s market value nearly doubled since the beginning of the year.