AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects modest growth when Invitation Homes reports first-quarter 2026 results on April 30. The consensus among 2 analysts calls for earnings per share of $0.15 and revenue of $687.0M. The revenue estimate range spans from $667.4M to $695.6M, while the EPS forecast shows no variation, with both analysts aligned at $0.15.

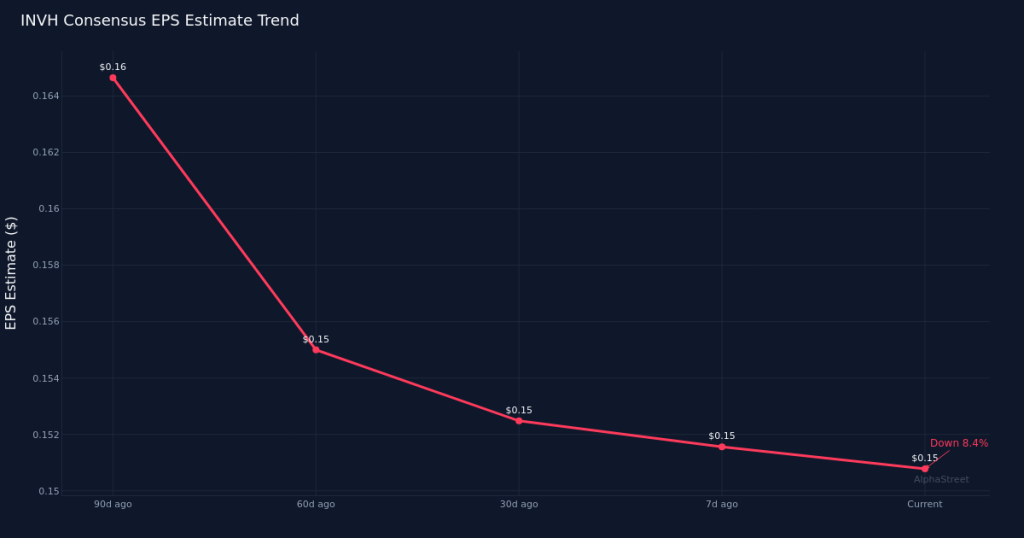

Analyst sentiment has cooled in recent months. While EPS estimates held steady over the past 30 days at $0.15, the 90-day view reveals a down 6.3% drift from $0.16. This gradual reduction in earnings expectations suggests analysts have tempered their near-term outlook for the single-family rental REIT, potentially reflecting concerns about occupancy trends, operating expense pressures, or rent growth dynamics in the company’s markets.

The year-over-year comparison presents a challenging narrative. Consensus revenue of $687.0M represents implied growth of just 1.9% versus the year-ago quarter’s $674.5M, indicating relatively tepid top-line expansion for a residential REIT. More notably, the expected EPS of $0.15 marks an implied 44.4% decline from the $0.27 reported in Q1 2025. This dramatic earnings compression stands in stark contrast to the modest revenue growth, pointing to either significant margin deterioration or changes in the company’s capital structure and financing costs. Last year’s first quarter delivered net income of $105.8M on a net margin of 15.7%, establishing a high bar that current expectations suggest will not be approached.

The profitability disconnect warrants scrutiny. When revenue grows nearly 2% but earnings per share contracts by more than 44%, investors should examine what has changed in the operating model. For a residential REIT like Invitation Homes, potential culprits include rising property operating expenses, higher interest costs on debt, increased property taxes and insurance premiums, or elevated turnover and maintenance expenses. The substantial gap between revenue and earnings trajectories suggests the business is facing meaningful headwinds at the property or financing level that are compressing returns to shareholders.

Invitation Homes operates in the single-family rental space, where key performance indicators extend beyond traditional EPS and revenue metrics. Investors typically focus on same-store rental revenue growth, average occupancy rates, rental rate growth on new and renewal leases, turnover rates, and core funds from operations (FFO) and adjusted FFO metrics that better capture REIT operating performance. The divergence between modest revenue growth and sharp earnings decline suggests these underlying operational metrics may reveal stress in the portfolio, whether from occupancy challenges, slower rent growth, or cost inflation eating into margins.

The estimate range provides limited insight into analyst disagreement. With only 2 analysts covering the stock and complete consensus on the EPS figure at $0.15, there is essentially no divergence of opinion on earnings. The revenue range spans $28.2M from low to high estimate, representing just over 4% variance around the $687.0M consensus. This tight clustering could reflect either genuine confidence in the forecast or simply limited analytical attention given the small analyst count.

Understanding this quarter’s results requires context on portfolio composition and market exposure. Single-family rental REITs are sensitive to local employment trends, housing affordability dynamics, and the competitive landscape between renting and owning. The company’s geographic footprint, average home values, and tenant demographic profile all influence its ability to push rents while maintaining occupancy. Without visibility into these operational details from the prior quarter, investors will need to listen carefully to management’s commentary on April 30 for signals about demand trends and pricing power.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.