With the threat of coronavirus not subsiding, the consumer goods sector is staring at an uncertain future and the footwear industry is no exception. The movement restrictions that came into effect in the early days of the pandemic have brought a major change to people’s shopping habits, and cutting discretionary expenses has become the new norm.

Consumer Discretionary

California-based Skechers (NYSE: SKX) has been at the receiving end of the COVID crisis. It started the fiscal year on a dismal note and there are multiple challenges that can delay the recovery, such as households’ waning spending power, dismal employment scenario, and falling consumer sentiment.

[irp posts=”58117″]

Meanwhile, the market is witnessing a mass shift to e-commerce from physical stores – a trend retailers are trying to leverage in these difficult times. In the case of Skechers, the direct-to-customer strategy that integrates the online, offline, and concept stores can play a key role in enhancing customers’ shopping experience.

Digital Sales Spike

According to initial estimates, Skechers recorded triple-digit growth in e-commerce sales in the early weeks of the current fiscal quarter. Also, the company has started reopening stores in areas where the curbs have been relaxed, including China where most of its products are manufactured. On the flip side, the deteriorating Sino-US ties and macro issues, which added to the present crisis, remain a concern for US-based producers like Skechers.

As of now, experts are quite bullish about the company’s shares and recommend buying them, thanks to the recent uptrend and the brand’s growing clout in emerging markets. The other factors that make it attractive are the company’s strong balance sheet and impressive cash position. But investors would likely wait to see how the lifestyle firm comes out of the market crisis, given the cautious short-term outlook and the stock’s high valuation.

“We have proven over the years to be very flexible and nimble when it comes to challenges in the market. We believe that given the strength of our brand, our ability to navigate in challenging environments, and our investments in our future, we will continue to drive demand for our footwear, create more lasting impressions through marketing, and set more sales records.”

Robert Greenberg, CEO of Skechers

So, is the company prepared to tackle the issue? Well, efforts are on to right-size the business through staff reduction and hiring freeze. When it comes to liquidity, capital spending has been restricted to business-critical and strategic projects. When the company releases the first-quarter earnings, which is expected on July 23, the market will be looking for updates on the ongoing distribution center project in China that is slated for completion this year.

Tailwinds

On the positive side, Skechers has relatively low debt. The additional focus on cost management and favorable inventory position should add to the recovery momentum. Also, distribution constraints have eased, removing the logistics-related hassles.

It is imperative for the company to invest in the e-commerce business to make it a full-fledged platform. With the sneaker maker offering products for every customer cohort, ranging from formals to work-wear and sportswear to kids-wear, the brand enjoys a decent market share. At the same time, the American footwear industry is highly competitive and some of the Skechers products directly compete with those of Nike (NKE) and Adidas.

What Next?

In short, the company can’t afford to be complacent at any stage and should keep innovating, especially because seasonal factors and exchange rates often influence the business. That explains the many new partnerships it has formed both in the domestic market and overseas in the recent past. Interestingly, multiple class-action suits filed by rivals, including Nike, against Skechers are at various stages of hearing in the US courts.

While addressing analysts at the first-quarter earnings call, COO David Weinberg said, “While we have limited visibility as to when most markets will reopen and what business atmosphere will be like when they do, we see some positive indicators, including our extremely strong e-commerce business, the positive sales trajectory of our China business and reopening of several markets, most notably, Germany, Scandinavia, and Austria.”

Weak Q1

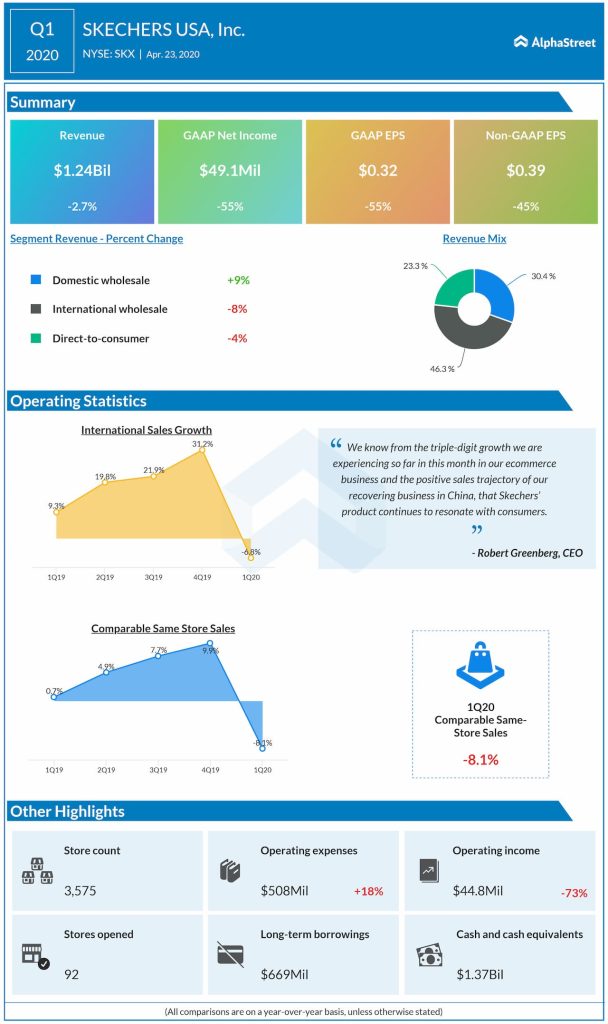

In the March quarter, revenues dropped 2.7% annually to $1.24 billion, apparently due to the COVID-induced disruptions in key markets. Consequently, adjusted earnings declined 45% to $0.39 per share. While overseas sales and comparable sales faltered, domestic wholesale sales advanced, underscoring the strength of the brand. Over the past five years, all the key operating metrics – sales, earnings, and operating income – registered steady growth.

[irp posts=”60997″]

The gradual pullback of Skechers’ shares from last year’s multi-year high was catalyzed by the selloff triggered by the pandemic a couple of months ago. Surprisingly, the stock stabilized pretty quickly since then and pared a part of those losses in recent weeks. The current price broadly matches the value registered a year earlier. The stock closed the last trading session slightly above $30.