The reopening of the market after the virus-driven shutdown is eliciting a mixed response from the corporate world, but companies like Starbucks Corp. (NASDAQ: SBUX) believe the worst of the pandemic is behind them. While being part of an industry hit hard by the crisis, the coffee chain looks to get back on track by early next year as reopening gains pace in key markets like U.S and China.

Related: Starbucks Q4 2020 Earnings Call Transcript

Online Push

Interestingly, the company expects to restore operations at a faster pace than widely estimated, even though the recovery of store-traffic outside the U.S. has been sluggish. During the pandemic days, the company generated revenues mainly from the sales of popular items like Frappuccinos and Pumpkin Cream Cold Brew. Meanwhile, taking a cue from the shift in customer behavior, the management is giving priority to ramping up the digital ecosystem and aligning the product portfolio.

From Starbucks’ Q4 2020 Earnings Conference Call:

“As customers continue to adapt to work from home and study from home realities, they create safe, familiar, and convenient experiences, and have shifted their buying behavior accordingly. And we’ve adapted rapidly to meet those evolving needs. Broadly speaking, we’ve seen US transactions migrate from dense metro centers to the suburbs, from cafes to drive-throughs, from early mornings to mid-mornings with outpaced recovery on the weekends.”

The market was optimistic enough to look beyond Starbucks’ weak fourth-quarter statistics and focus on the positive outlook. As a result, the stock made notable gains since last week’s earnings release, after losing steam initially. Currently, it is hovering close to the most recent peak and the valuation looks high relative to earnings. So, market watchers have assigned the stock moderate buy rating.

Bullish View

Exuding confidence in its efforts to tweak the business model in response to the changing customer behavior, the management has predicted that comparable sales would bounce back from the current lows and grow in double-digits next year. In the U.S, comparable sales are picking pace aided by the initiatives to support partners and maintain stable engagement, thereby ensuring quality customer experiences. The fact that drive-through and mobile orders accounted for about 75% of US sales in the final three months of 2020 shows the new sales trend is gaining ground.

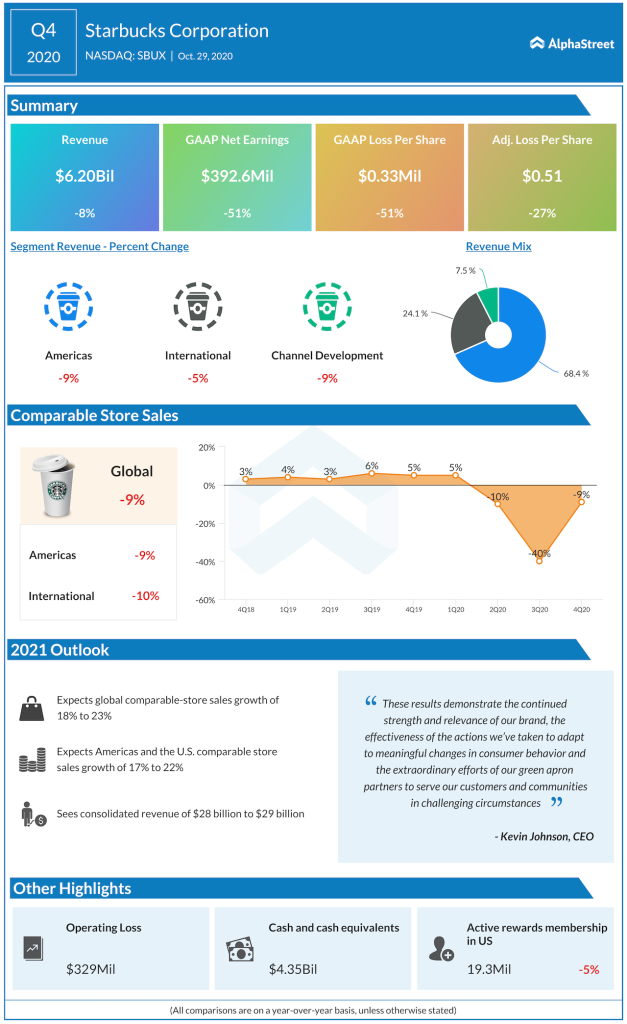

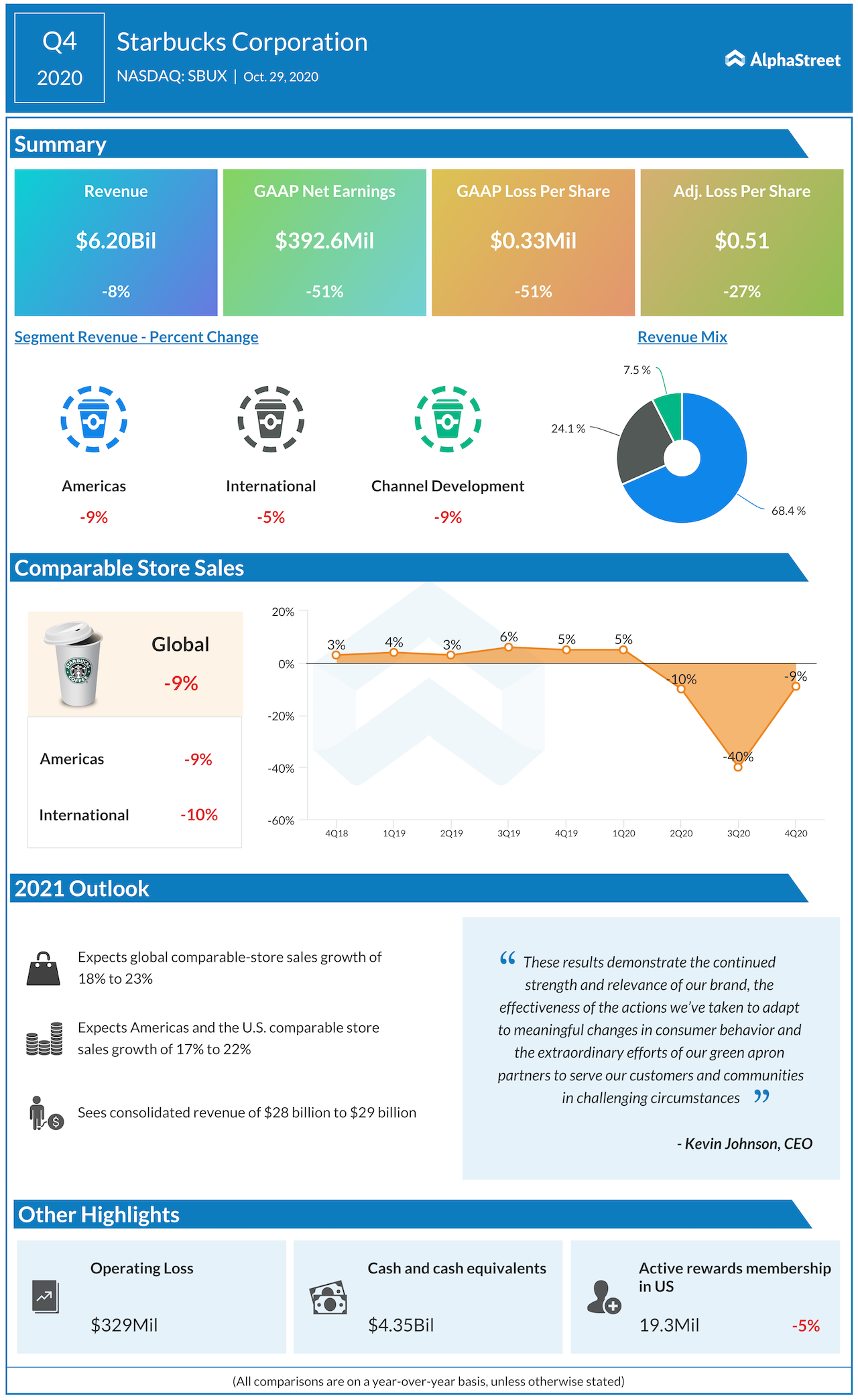

Comps on Recovery Path

Starbucks reported a decline in adjusted earnings to $0.51 per share in the fourth quarter when revenues dropped 8% from last year to $6.2 billion, with all the three business segments registering lower sales. The bright spot was a sequential improvement in comparable-store performance, which decreased at a slower pace.

“Our business recovery is progressing well, and through rapid innovation, we’ve built a new level of resilience for the future. We believe that the investments we made to protect our partners’ well-being and provide them with economic certainty combined with our principled approach to decision-making and transparency of our communications have built trust with all stakeholders and will pay dividends long into the future,” said Kevin Johnson, chief executive officer of Starbucks.

Read managements/analysts’ comments on quarterly reports

Continuing its recovery from the lows seen mid-March, Starbucks’ stock is trading slightly above the $90-mark, which is close to the levels seen at the beginning of the year. It has gained 26% in the past twelve months but underperformed the broad market during that period.