Colgate-Palmolive Company’s (NYSE: CL) stock gained after the consumer products giant reported better-than-expected fourth-quarter results, despite headwinds from softer consumer spending and broader economic volatility. However, management issued conservative sales and margin guidance for fiscal 2026, citing tariff-related uncertainties and weakness in the domestic market.

The Stock

Over the past several months, the New York-headquartered company’s stock market performance has not been very impressive, but it entered 2026 on a positive note. Maintaining the momentum, the stock rose early Friday following the earnings announcement. The shares have gained around 12% so far this year.

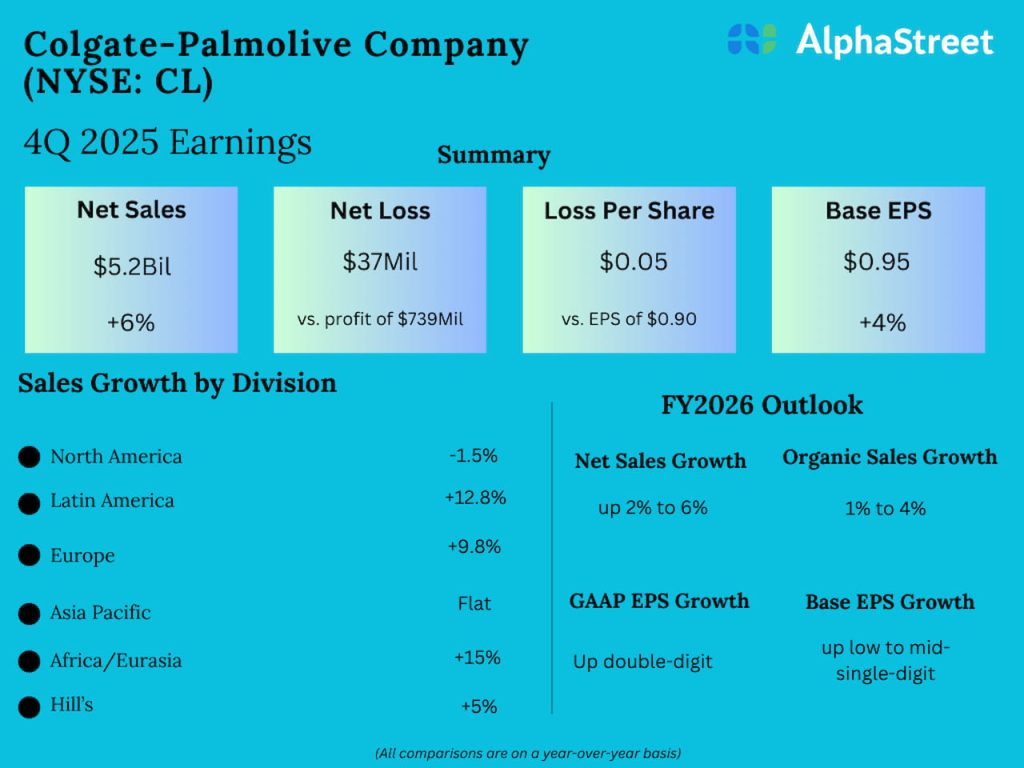

Adjusted earnings rose to $0.95 per share in the fourth quarter from $0.91 per share in the corresponding quarter last year, exceeding expectations. The bottom-line growth reflects an increase in net sales to $5.23 billion from $4.94 billion in the same period of 2024. Sales exceeded estimates. Organic sales moved up 2.2% YoY.

Earnings Beat

On an unadjusted basis, the company reported a net loss of $37 million or $0.05 per share for the fourth quarter, compared to a profit of $739 million or $0.90 per share in the year-ago quarter. Meanwhile, gross profit margin decreased 10 basis points from last year to 60.2% during the three months.

From Colgate-Palmolive’s Q4 2025 Earnings Call:

“We delivered improved momentum on our business in Q4 in terms of organic sales growth and market share, and we have seen stabilization of category growth rates as we exit 2025, but we still face significant uncertainty. While category growth may have stabilized, growth rates remain low. This is difficult in and of itself, but also could lead to higher levels of promotion and other competitive activity. Foreign exchange is favorable right now but has been a negative impact for 8 of the past 10 years.”

Outlook

Colgate-Palmolive announced the launch of its new 2030 strategy, called the Strategic Growth and Productivity Program, transitioning from the plan that concluded in 2025 and emphasizing omnichannel demand, digital investment, and organizational restructuring. The management said it expects ongoing operational challenges and slower category growth to continue in the short term. For fiscal 2026, the company expects net sales to be up 2% to 6%, including a low-single-digit positive impact from foreign exchange.

The guidance for full-year organic sales growth is 1-4%, which includes a 20 basis-point impact from the company’s exit from its private label pet food business. On a reported basis, gross profit margin is expected to expand in FY26, with advertising up and double-digit earnings per share growth. The company has lowered its outlook for the skin health business to reflect lower-than-expected category growth rates and weak performance in certain markets, particularly in China.

The stock was trading up 5% on Friday afternoon, crossing its 52-week average price of $85.60. CL has gained more than 3% in the past six months.