AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects Lincoln Electric Holdings to deliver EPS of $2.43 on revenue of $1.07B when the welding equipment and consumables manufacturer reports Q1 2026 results on April 30. Nine analysts have published estimates, with EPS projections ranging from $2.23 to $2.57 and revenue forecasts spanning $1.03B to $1.09B. The consensus figures represent measured growth expectations as the company navigates the industrial manufacturing cycle.

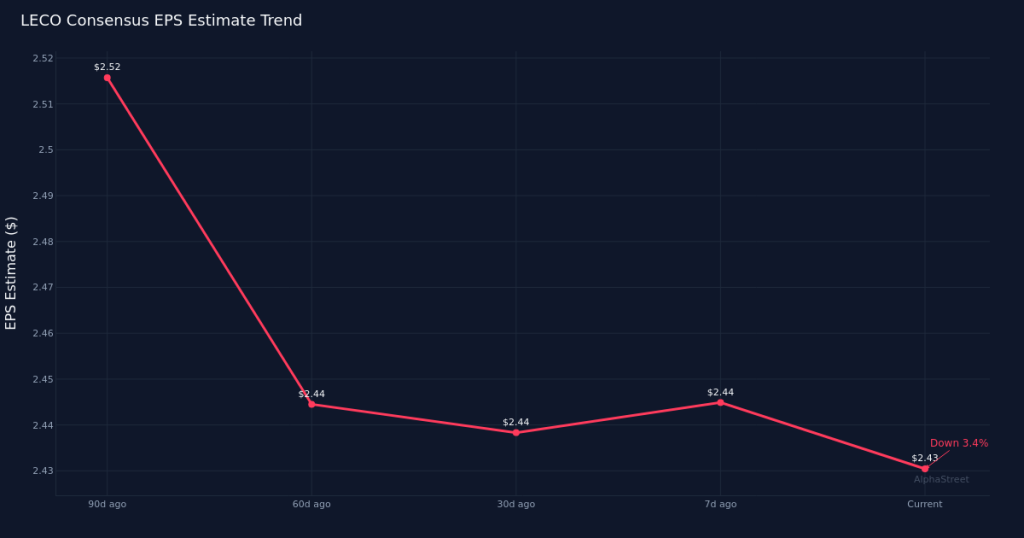

Analyst conviction has weakened modestly heading into the print. The EPS consensus has drifted down 0.4% over the past 30 days from $2.44, and the erosion extends further when looking back 90 days, with estimates declining 3.6% from $2.52. This downward revision pattern suggests analysts have been tempering expectations, potentially reflecting concerns about end-market demand or input cost pressures in the welding and cutting products segment. When estimates move in one direction consistently, it often signals shifting fundamentals rather than noise.

The year-over-year comparison shows Lincoln Electric positioned for double-digit earnings growth. Consensus EPS of $2.43 would mark a 12.5% increase from the year-ago result of $2.16, while the revenue target of $1.07B implies 7.0% growth over the prior-year period’s $1.00B. This dynamic—where earnings are expected to grow nearly twice as fast as revenue—points to anticipated margin expansion or operational leverage. The year-ago quarter generated net income of $121.9M on a net margin of 12.2%, providing a profitability baseline against which to measure the company’s ability to convert incremental revenue into bottom-line performance. For an industrial manufacturer, maintaining or expanding margins while navigating material costs and labor inflation would signal pricing power and operational discipline.

Lincoln Electric operates in the tools and accessories sector, serving industrial end markets that include general fabrication, heavy industries, automotive, and construction. The company’s performance typically reflects broader trends in capital investment, manufacturing activity, and infrastructure spending. Welding consumables tend to correlate with industrial production levels, while equipment sales are more discretionary and sensitive to customer capital budgets. The interplay between these two revenue streams—consumables providing recurring revenue stability and equipment driving lumpier growth—shapes quarterly performance. Investors will be watching for commentary on geographic mix, as North American, European, and Asia-Pacific markets often move at different speeds through the industrial cycle.

The estimate revision trajectory over three months reveals a pattern worth noting. The 3.6% decline in the EPS consensus from $2.52 to $2.43 over 90 days suggests analysts have been recalibrating their models as new data emerged. Whether this reflects softer order trends, foreign exchange headwinds, or competitive dynamics in key markets will likely surface in management’s prepared remarks and guidance commentary. The revision pattern is significant enough to indicate changing expectations rather than minor tweaks.

Lincoln Electric’s track record on estimate accuracy will influence how the market interprets results. Companies with consistent beat-or-miss patterns often see muted reactions to in-line results, while those with less predictable performance can experience sharper moves. The width of the estimate range—$2.23 to $2.57 on EPS—suggests meaningful dispersion in how analysts are modeling the business, with the high-end estimate 15% above the low-end projection. This dispersion indicates uncertainty about key assumptions, whether related to volume, pricing, mix, or cost absorption.

Beyond the headline numbers, operational metrics will provide texture on business momentum. Management typically discusses order rates, backlog trends, and pricing realization across product categories. For a manufacturer with both consumables and capital equipment exposure, the book-to-bill ratio and backlog conversion rates offer insight into near-term revenue visibility. Commentary on automation and welding technology adoption could signal longer-term growth drivers, while any discussion of capacity utilization or inventory management speaks to operational efficiency and working capital discipline.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.