The pandemic came as a setback for Lyft, Inc. (NASDAQ: LYFT) as the ridesharing platform was going through a crucial phase when the travel restrictions were imposed. But the company managed to get back on track by attracting customers through promotional offers and by enhancing drivers’ compensation. Now, the question is whether it would be able to retain the momentum in this troubled market.

Recently, shares of the company slipped to an all-time low, but experts are of the view that the trend would change for the better. While the bullish target price validates the rebound in ridesharing, there is continuing uncertainty over the stock’s long-term prospects. However, LYFT traded higher most of Wednesday’s regular session, extending the recent uptick. The fact that the company has raised its dividend on a regular basis should also bring cheer to shareholders.

Profitability

Being part of a highly competitive but still emerging industry, Lyft is yet to generate profit. There are also concerns about the unimpressive bottom-line performance in recent quarters, compared with analysts’ estimates, though the company maintained stable revenue performance during that period.

Read management/analysts’ comments on quarterly reports

The online taxi industry, which is still at a nascent stage, is yet to prove its sustainability, with leading players like Lyft and Uber Technologies (NYSE: UBER) experiencing high volatility even after becoming public entities a few years ago. The nature of the business is such that the companies struggle to establish as successful brands that elicit meaningful customer loyalty. To put it simply, customers tend to switch between service providers as per their convenience since there are no binding agreements like contracts.

Financial Data

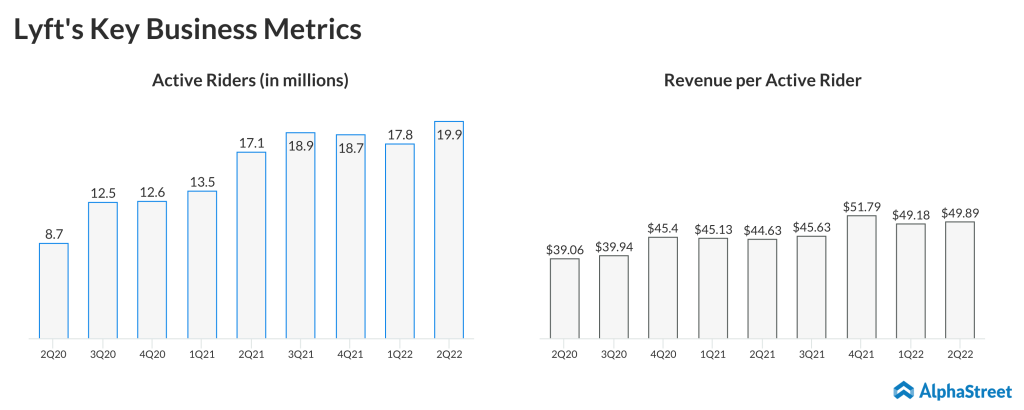

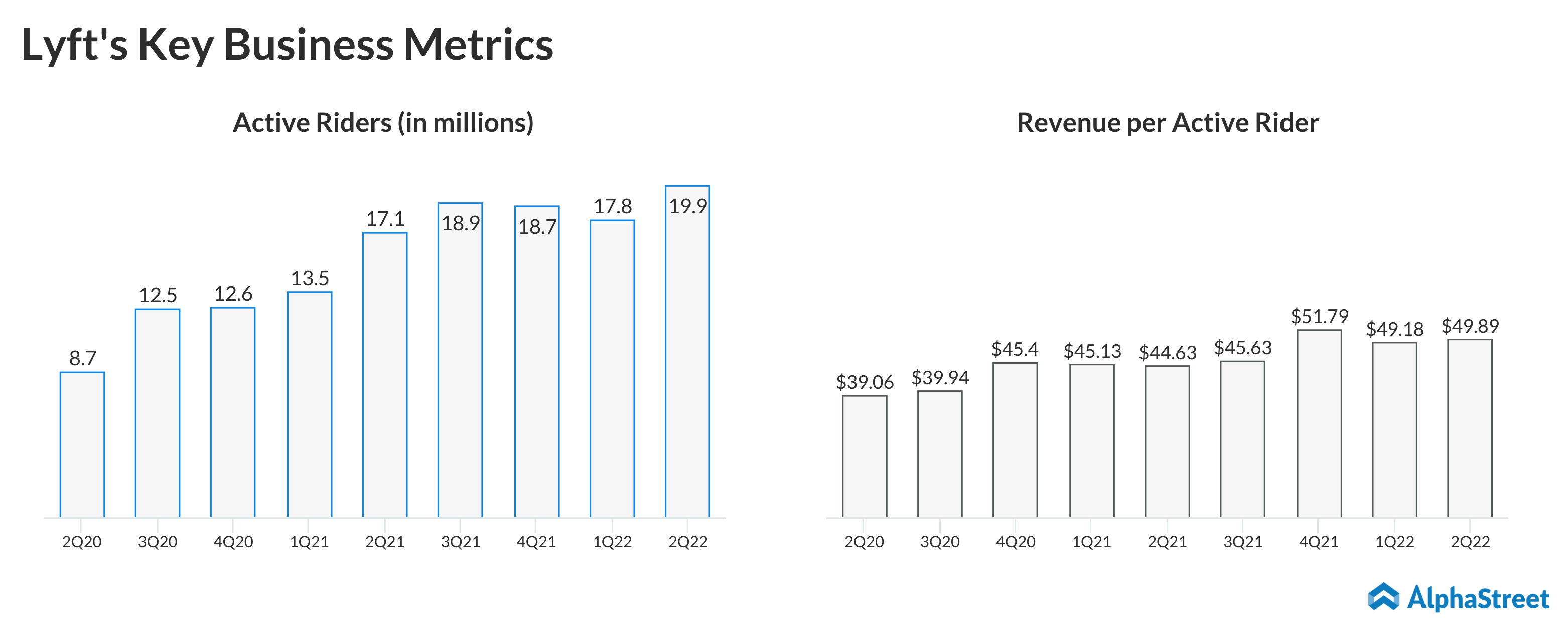

Lyft reported an adjusted profit of $64 million for the second quarter of 2022, which marked an improvement from the prior-year period when the company incurred a loss of $18 million. On an unadjusted basis, however, it reported a net loss of $377.2 million or $1.08 per share, compared to a loss of $251.9 million or $0.76 per share last year. At $990.7 million, revenues were up 87%.

On the positive side, there is a continued uptick in EBITDA, which excludes special items. It is estimated that the management’s cost-cutting initiatives would come in handy in the turnaround efforts, against the backdrop of elevated operating expenses dragging down earnings.

“Over the past several months, one of the most common requests in investor conversations has been for more visibility into our longer-term profitability. While the macroeconomic environment continues to create near-term uncertainty, we are confident in the fundamentals of our business. As we look out to 2024, we are targeting adjusted EBITDA of $1 billion with over $700 million of free cash flow, which is defined as operating cash flow less CAPEX,” said Lyft’s CEO Logan Green during a recent interaction with analysts.

Uber slips to loss in Q2 despite strong revenue growth; bookings at a record high

Lyft’s stock has lost about 58% since the beginning of the year. All along it stayed sharply below the long-term average and the all-time high recorded a few years ago. Trading slightly below $20 on Wednesday afternoon, it continued to underperform the broad market.