Online taxi services were among the worst affected by the coronavirus crisis that crippled the entire transportation industry. While the business world is emerging from the pandemic-induced slump, ride-hailing platform Lyft, Inc. (NASDAQ: LYFT) is struggling to get back on track. The company, which became a public entity more than three years ago, is yet to become profitable.

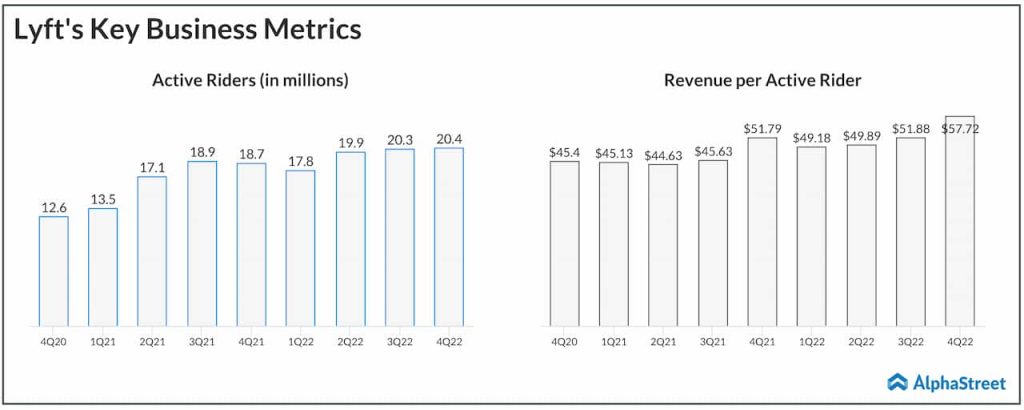

Lyft’s turnaround prospects were dampened by COVID-related movement restrictions and the resultant fall in traffic. Meanwhile, in a sign that the company is on the recovery path, the number of riders rose steadily since the pandemic recovery started. There has been a corresponding increase in revenues.

Read management/analysts’ comments on Lyft’s Q4 2022 financial results

Lyft’s lackluster financial performance has dented investor sentiment, and the stock has been in a free fall for about two years. The weak fourth-quarter results and a dismal outlook for the first quarter of 2023 added to the stock’s downturn, resulting in a 35% fall soon after the announcement last week. From an investment perspective, LYFT has become pretty cheap after the decline, but the underlying weakness makes it a risky bet.

Headwinds

The main hassles for a sustainable recovery are rising competition, especially from arch-rival Uber Technologies Inc (NYSE: UBER), pricing pressures, and seasonal factors that affect vehicle rentals. So, Lyft is currently a laggard among its peers. The recent slowdown in rider additions and shortage of drivers weigh on operations, while the introduction of surge prices made the platform more expensive.

“Relative to three months ago, the competitive dynamics changed. And the better marketplace balance we see it today, creates significant opportunities for long-term growth. To take advantage of this opportunity and grow the market, we must prioritize competitive service levels. This will impact our 2024 adjusted EBITDA and free cash flow targets. We are assessing the impacts of these changes and are actively reviewing adjustments to the business, including cost-cutting measures,” said Lyft’s CEO Logan Green during his recent interaction with analysts.

Surprise Loss

In the fourth quarter of 2022, the company reported a net loss of $588.1 million, marking a deterioration from the prior-year period when the loss was $283.2 million. Excluding one-off items, it posted an adjusted loss of $270.8 million, defying expectations for positive earnings. The bigger loss mainly reflects a revision of calculations for Earnings before Interest, Taxes, Depreciation, and Amortization to comply with the SEC regulations.

TSLA Earnings: All you need to know about Tesla’s Q4 2022 earnings results

Meanwhile, total revenues increased 21% annually to a record high of $1.2 billion, aided by an increase in the number of active riders and higher revenue per user. Taking a cue from the slow recovery, the management issued first-quarter 2023 revenue guidance below analysts’ estimates.

Peer Performance

Earlier, Uber reported a whopping 49% growth in fourth-quarter revenues, which is higher than the consensus estimate. Though net profit declined, due to a sharp increase in operating expenses, the bottom line came in above expectations.

After languishing in historic lows most of last year, Lyft’s stock entered 2023 on an optimistic note but the recovery was short-lived. The stock suffered a major setback after last week’s earnings, and traded lower during Tuesday’s session.