Shares of Macy’s Inc. (NYSE: M) were down on Thursday. The stock has gained 36% over the past three months and 18% over the past one month. The company’s sales and profits for its most recent quarter declined year-over-year but exceeded forecasts, which generated a positive sentiment around the stock. Here’s a look at the retailer’s expectations for the near term:

Sales

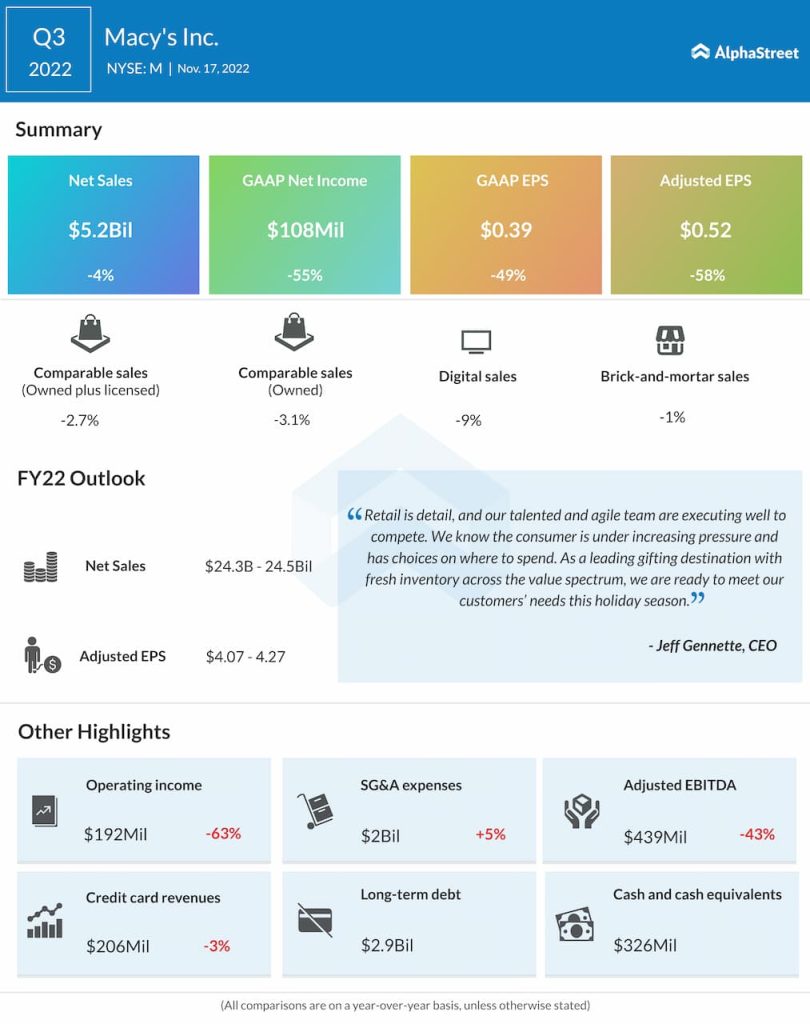

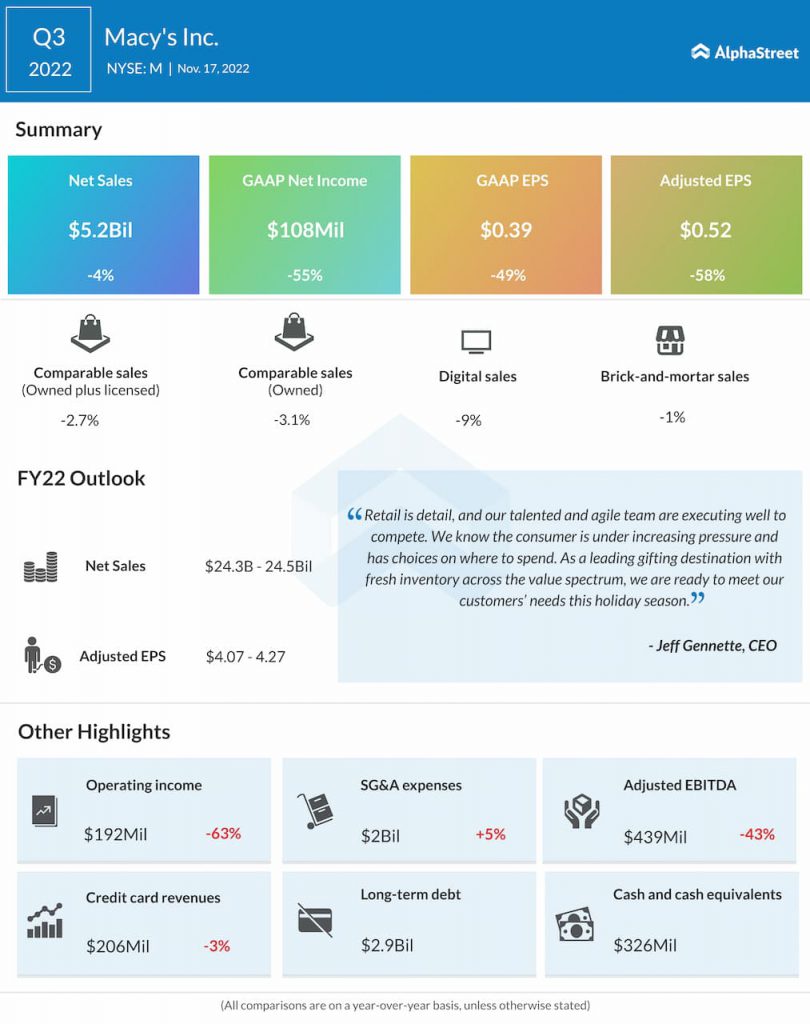

Macy’s generated net sales of $5.2 billion in the third quarter of 2022, which was down 3.9% from the same period a year ago. Comparable sales were down 3.1% on an owned basis and down 2.7% on an owned-plus-licensed basis.

Comparable sales for the Macy’s nameplate were down 4.4% on an owned basis and 4% on an owned-plus-licensed basis. Bloomingdale’s comp sales were up 5.3% on an owned basis and 4.1% on an owned-plus-licensed basis. Bluemercury comp sales were up 14% on an owned and owned-plus-licensed basis. Digital sales decreased 9% and brick-and-mortar sales declined 1% year-over-year.

For the fourth quarter of 2022, Macy’s expects net sales of $8.1-8.4 billion. For the full year of 2022, the company expects net sales of $24.3-24.5 billion. Comparable owned-plus-licensed sales are estimated to be flat to up 1% while digital sales are expected to comprise approx. 33% of net sales for the year.

Profitability

Macy’s delivered adjusted EPS of $0.52 in Q3 2022 compared to $1.23 in the year-ago period. Gross margin for the quarter dropped 230 basis points to 38.7% compared to last year, driven by a decline in merchandise margin that was caused by more discounts to sell slow-moving categories such as casual apparel and warmer weather seasonal goods.

For the fourth quarter of 2022, Macy’s expects adjusted EPS of $1.47-1.67. Gross margin is expected to be down no more than 270 basis points from last year, reflecting the impacts of markdowns and the competitive promotional environment. For the full year of 2022, the company expects adjusted EPS to range between $4.07-4.27 while gross margin is expected to be down approx. 150 basis points from last year.

Others

As stated on its quarterly conference call, Macy’s expects holiday shopping patterns to be similar to 2019. Inflationary pressures on the consumer are expected to continue and the promotional competitive landscape is expected to intensify throughout the holiday and into January.

For the full year, Macy’s expects credit card revenues to make up approx. 3.4% of net sales. SG&A expense rate is estimated to decline approx. 120 basis points from last year. Adjusted EBITDA margin is expected to be approx. 10.5% and capital expenditures are projected to be approx. $1.2 billion.