Shares of Philip Morris International Inc. (NYSE: PM) were down 1.5% on Tuesday despite the company reporting better-than-expected earnings results for the third quarter of 2021. Both revenue and earnings surpassed market projections and the company narrowed its earnings guidance for the full year. PMI also cautioned that the ongoing chip shortage could impact its IQOS growth in the coming months.

Quarterly performance

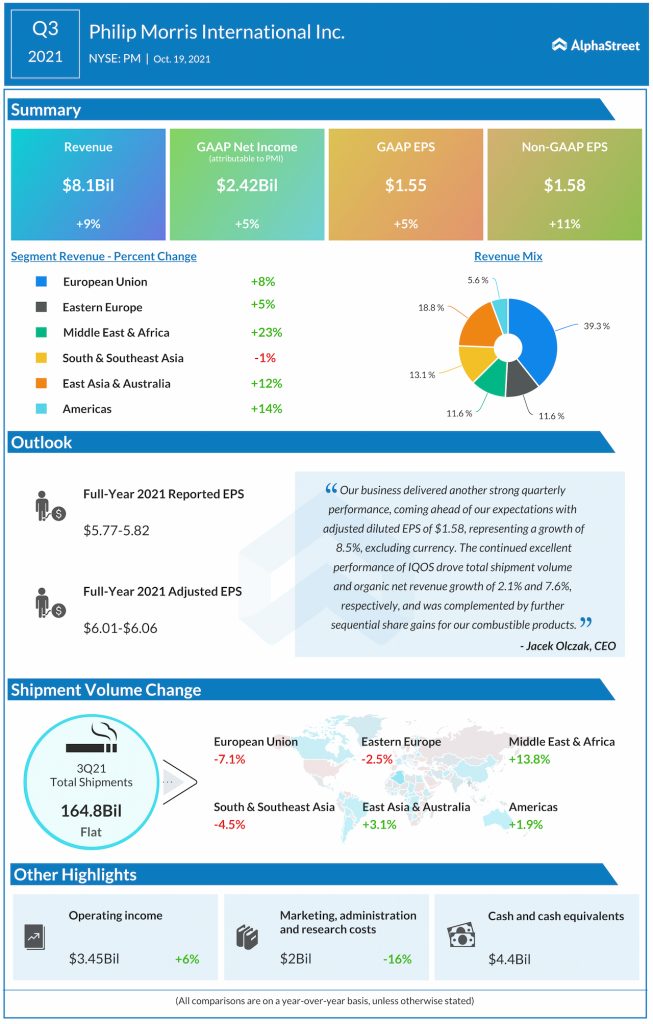

In Q3 2021, PMI’s net revenues increased 9.1% year-over-year to $8.1 billion, beating estimates. On an organic basis, revenues grew 7.6%, reflecting favorable volume/mix and higher device volume. Reported EPS rose 4.7% to $1.55 while adjusted EPS grew 11.3% to $1.58, exceeding expectations.

Assumptions and strategies

During the quarter, PMI’s total shipment volume increased by 2.1% helped by higher heated tobacco shipment volumes in Eastern Europe and East Asia & Australia, as well as higher cigarette shipment volumes in the Americas and the Middle East & Africa.

In Q3, net revenues from smoke-free products made up 28.6% of total revenues. At quarter-end, total IQOS users stood at approx. 20.4 million, of which around 14.9 million have switched to IQOS and stopped smoking.

The ongoing global semiconductor shortage is expected to take a toll on IQOS growth as IQOS device supply takes a hit and the company prioritizes devices for existing users over new user acquisition. In addition, the launch of IQOS ILUMA in certain markets which was set to take place this year has been pushed to the second half of 2022.

Along with strong growth in existing markets, PMI is driving the geographic expansion of its smoke-free products as it aims to reach 100 markets by 2025. In Q3, the company launched IQOS in Egypt. It also has a presence in the snus and nicotine pouch category in Norway and Iceland thanks to its recent acquisition of AG Snus. The number of markets where PMI’s smoke-free products are available for sale now stands at 70.

PMI is looking to move into new business areas beyond nicotine and tobacco. The company sees significant opportunity in areas like botanicals and inhaled therapeutics, which are expected to have an addressable market of around $65 billion by 2025. The acquisitions of Fertin Pharma, Otitopic and Vectura are expected to help expand its development capabilities.

Outlook

Philip Morris narrowed its reported EPS guidance for the full year of 2021 to a range of $5.77-5.82 from its previous range of $5.76-5.86. Adjusted EPS is expected to be $6.01-6.06. On an organic basis, revenues are expected to grow plus 6.5% to plus 7%.