Shares of Philip Morris International Inc. (NYSE: PM) were up over 3% on Thursday after the company beat expectations on both revenue and earnings for the second quarter of 2022. The quarterly results were driven by strong momentum in IQOS as well as favorable cigarette category trends. Based on these trends, the company has raised its outlook for the full year.

Quarterly performance

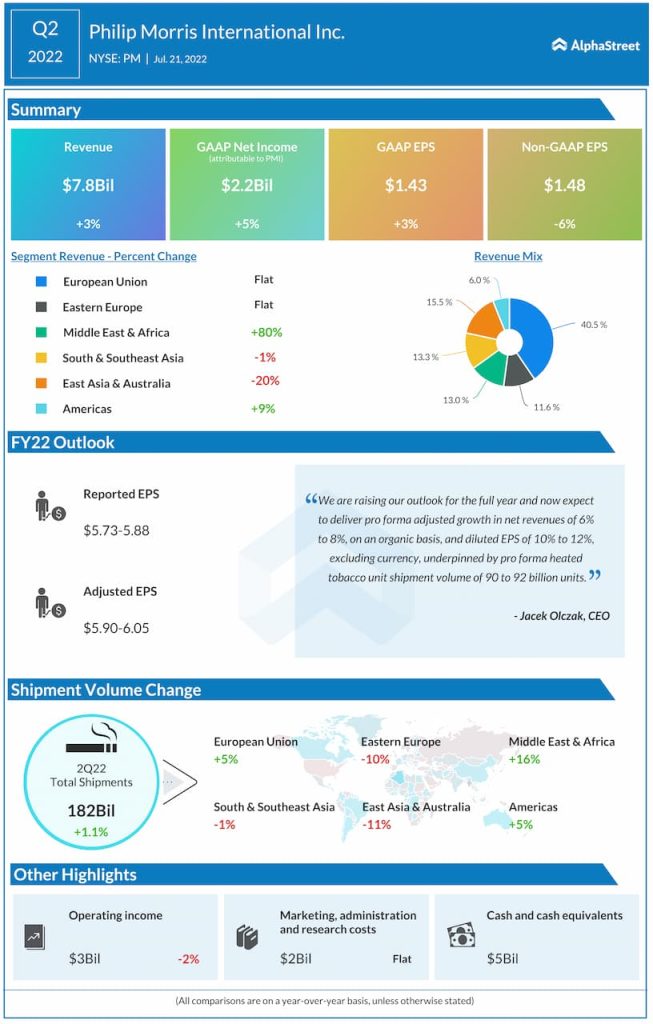

Net revenues increased 3% year-over-year to $7.83 billion, surpassing projections. On an organic basis, revenues increased 8.7%, reflecting favorable volume/mix driven mainly by higher heated tobacco unit volume, device volume and cigarette volume. GAAP EPS rose nearly 3% to $1.43. Adjusted EPS fell 6% YoY to $1.48 but beat estimates.

IQOS

Pro forma total IQOS users at the end of Q2 were estimated at approx. 19 million, reflecting a YoY growth of over 20%. On a sequential basis, the company saw user growth of more than 1.1 million due to the easing of device limitations and pandemic restrictions. PMI is seeing strong momentum in the EU region, Japan and developing markets.

IQOS devices accounted for approx. 5% of the $4.2 billion of pro forma RRP net revenues for the first half of the year. For the full year of 2022, PMI expects to deliver pro forma HTU shipment volumes of 90-92 billion units.

The IQOS ILUMA continues to do well across its initial launch markets. ILUMA is seeing robust growth in Japan and it is performing well in markets such as Spain and Switzerland where it is seeing good demand. PMI launched ILUMA in Greece in late June and it plans to roll it out in more markets during the fourth quarter.

Swedish Match acquisition

Philip Morris expects to close the Swedish Match acquisition during the fourth quarter. This deal will allow PMI to tap into the large and growing US smoke-free market, and by adding products like the nicotine pouch brand ZYN to its portfolio, it will allow the company to take advantage of the opportunity in other smoke-free categories in the coming years.

Outlook

Based on the strong growth seen in IQOS and robust trends in combustibles, the company raised its full-year 2022 guidance. Total pro forma shipment volumes are expected to grow by 1.5-2.5% for the year. Pro forma net revenues are estimated to grow 6-8% on an organic basis while pro forma currency-neutral adjusted EPS is projected to grow 10-12%. For the third quarter of 2022, pro forma adjusted EPS is expected to range between $1.23-1.28.

Click here to access the full transcripts of the latest earnings conference calls