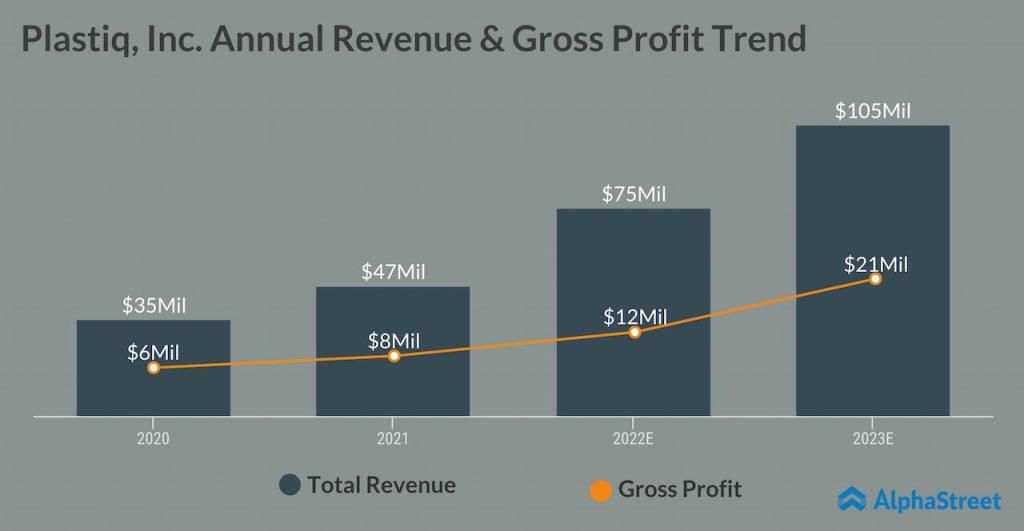

The payments market witnessed significant growth in recent years, especially during the pandemic that triggered the widespread adoption of digital payment services. Plastiq, Inc., a leading payment automation platform, has played a key role in enabling small and medium businesses to participate in the digital transformation by helping them access automated payment systems and giving multiple options for B2B payments. It is estimated that more than 195,000 payers are using Plastiq, which is currently preparing to go public.

In an exclusive interview with AlphaStreet, Plastiq’s chief executive officer and co-founder Eliot Buchanan spoke about the company’s upcoming stock market listing and future plans. Read the full interview:

Can you give a brief overview of the company and its operations?

Plastiq started as a consumer-facing payment platform originally, helping consumers use a credit card to pay for anything they’d like – including tuition, rent, or even their taxes. We’ve since evolved into a solution for small-to-midsize businesses – helping them run all their accounts payable. We help businesses access working capital right in their payment workflows through credit cards and short-term financing. This helps improve cash flow so they can better operate their business. One of the ways we discovered this need was that we would analyze the credit cards that small businesses were using on our platform that had many of them had had no rewards. That meant that the people using these credit cards didn’t care about what rewards the cards offered – they simply wanted to take advantage of the ability to use a credit card to make a payment. And as our relationships got deeper with our clients, we learned more about their needs – evolving our product and focus to help them with additional challenges like finding new sources of credit and more.

What is your strategy to compete effectively with others like Stripe?

Stripe’s model is no different than the methods for credit card acceptance that go back five decades. Plastiq’s approach is totally unique. A buyer-funded model, differentiated from Stripe in that the merchant can elect to pass the card processing fees to their customer in exchange for the benefit of leveraging their card as a financing instrument for large B2B expenses like inventory, ads, raw materials, and freight.

The payments industry, as it relates to credit card acceptance, has for decades now been fundamentally focused on the idea that merchants should be paying a 4-5% fee to accept credit cards. Plastiq’s approach is the exact opposite.

We believe the segment of the $9-trillion market size of B2B payments does not run through credit cards because merchants have no interest or ability to eat this type of fee. And so, we reverse the model. Our belief is that most of the ecosystem can support what we refer to as a “buyer-funded” model. When businesses use Plastiq to accept credit cards, it’s free. Not only does the model offer convenience for businesses that want to get paid faster by customers, it’s a way to provide more buying power and instant working capital for their customers. It all adds up to healthier supplier/custom relationships.

Galaxy Next Generation’s main focus in FY23 is accelerating revenue growth: CEO Gary LeCroy

By decoupling the funding mechanism from the disbursement mechanism, Plastiq bridges the gap in B2B payments where there is often a mismatch between how buyers and suppliers want to pay or get paid. Plastiq enables a business to pay suppliers digitally (from a credit card or bank account) and even if their vendor still prefers a paper check, Plastiq makes that possible. Plastiq Connect enables any platform to offer a payment solution to customers.

How will B2B payments look ten years from now? We believe there’s no world where all businesses aren’t embedding payments and being active parts of the payments ecosystem. In the future, we envision Plastiq existing as an infrastructure for platforms that may not even exist today, as the plumbing behind the accounts payable and cash flow needs any provider can capitalize on to support and monetize their customer base.

How do you look at Plastiq’s prospects as a public company, in terms of scaling the business?

We’re excited about becoming a publicly traded company for many different reasons, but there were two primary drivers for us. First, it’s an opportunity to sufficiently capitalize on the company, which would give us a competitive advantage in the market. Second, becoming a publicly traded company helps showcase our credibility in the market. It will help us attract new partners, talent, and clients – which will be incrementally valuable as we continue to grow.

Once public, we plan to invest significantly in product and feature development – helping our customers with new capabilities and solutions that make their businesses run more effectively. We’re also going to explore some M&A opportunities, looking for companies that would complement and extend our current product portfolio. We’ll also look to invest in additional go-to-market activity to increase awareness for Plastiq across the board.

Can you talk about emerging trends in the payments industry?

For five or six decades now, the credit card industry has been focused on one primary value proposition which is convincing merchants that in order to accept credit cards, they should be paying a fee of 3 – 4%. We believe that part of the reason why the $9-trillion market of B2B payments does not run on credit cards is that the merchant has neither interest nor the ability to pay that type of fee – which is why we reversed it. Our belief is that most of the ecosystem can support what we call a buyer-funded model versus a supplier-funded model – which is the foundation for our business.

Trxade explores alternative ways to find partners for B2C assets: CEO Suren Ajjarapu

There are five key trends that support that foundation and align with our mission:

- SMBs lack access to sufficient, on-demand cash flow which is a critical component to growing their business.

- Legacy providers focus on consumer and enterprise markets with few purpose-built SMB solutions, forcing SMBs into a consumer-style bill pay

- Inadequate access to technology and data with limited visibility into cash positions, AP, and AR workflows.

- Payments are managed by complex, paper-based processes that are expensive, manual, and prone to error.

- Mounting interest in Buy-Now-Pay Later (BNPL), giving SMBs more flexibility with short-term financing, allowing a business using this product to select an installment or payment plan for that transaction.

Where do you see Plastiq five years from now?

It’s hard to predict what’s going to happen tomorrow, let alone 5 years from now. I do expect that Plastiq will continue to expand its product portfolio addressing new challenges that our customers face every day – particularly as technology and the market evolves. When I think further down the road, I see Plastiq as more of an infrastructure solution for the accounts payable needs of any provider that wants to monetize their small-to-midsize business base, whether it be banks, payroll companies, insure-tech companies, etc.