AlphaStreet Newsdesk powered by AlphaStreet Intelligence

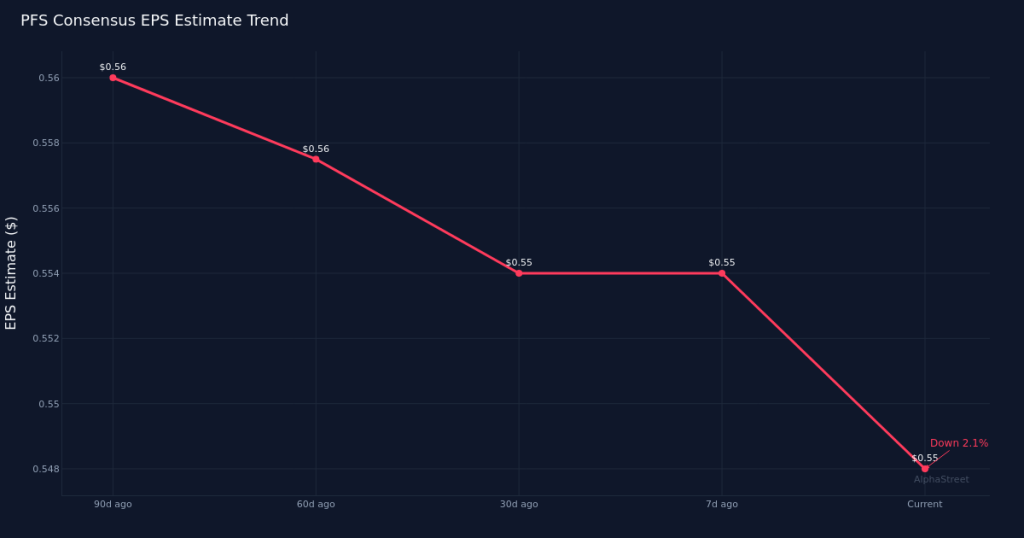

Wall Street is looking for Provident Financial Services to deliver earnings of $0.55 per share when the regional bank reports first quarter 2026 results. The consensus view comes from five analysts covering the institution, with EPS estimates ranging narrowly and revenue projections spanning. The tight dispersion in estimates suggests analysts hold relatively uniform views on the bank’s near-term performance trajectory.

Analyst conviction has remained steady in recent weeks but shows signs of modest erosion over a longer horizon. The $0.55 consensus has held firm, unchanged from prior expectations. Looking back, however, estimates have drifted down, indicating a subtle recalibration as analysts incorporated evolving deposit costs, loan demand patterns, or net interest margin dynamics into their models. This modest downward revision, while small in magnitude, reflects the challenging operating environment regional banks continue to navigate.

The consensus figures imply solid year-over-year expansion across both top and bottom lines. Compared to the first quarter of 2025, when Provident reported earnings of $0.49 per share on revenue of $208.7M, the Street’s current expectations translate to 12.2% growth in EPS. A year ago, the bank generated net income, reflecting the earnings power typical of well-managed regional banks. The implied earnings acceleration ahead of revenue growth suggests analysts expect some combination of operating leverage, improved efficiency, or favorable credit dynamics to drive margin expansion, though the specific drivers will become clear only when management reports results and provides commentary.

Prior quarter momentum data is not available in the verified dataset, limiting visibility into the sequential trajectory heading into this report. Investors will need to rely on year-over-year comparisons and broader industry trends to assess Provident’s recent performance. Regional banks broadly have been managing through an environment characterized by elevated funding costs, cautious loan growth, and persistent questions about commercial real estate exposure. How Provident has navigated these crosscurrents relative to peers will be a key focus when results emerge.

Historical beat-and-miss data is not included in the available information, so investors lack a clear view of Provident’s track record for surprising relative to estimates. Some regional banks consistently exceed expectations through conservative guidance and disciplined execution, while others experience more volatile results tied to credit events or interest rate sensitivity. Understanding where Provident falls on this spectrum would provide useful context for interpreting the upcoming report, but that pattern will need to be assessed through other research.

Stock positioning data heading into the report is not available in the verified dataset. Where shares trade relative to their 52-week range typically influences how the market interprets results, with stocks near highs facing tougher hurdles to rally on modest beats and those near lows potentially benefiting from lower expectations. Investors will need to monitor the technical setup independently as the report date approaches.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.