Digital workflow solutions provider ServiceNow (NYSE: NOW) will release its earnings results for the third quarter of 2019 following the close of market on Wednesday, October 23, 2019. Wall Street expects ServiceNow to post a profit of $0.88 per share on revenue of $884.97 million in the third quarter. This represents a year-over-year growth rate of 29% for EPS and 31.5% for revenue. ServiceNow stock closed down 4.45% at $243 on Friday.

For the second quarter of 2019, ServiceNow surpassed market views. The Santa Clara, California-based firm posted earnings of $0.71 per share on revenue of $833.9 million. Subscription revenue surged 33% over the prior-year quarter, while adjusted subscription billings grew 34% in the second quarter. However, NOW stock declined after it reported second quarter earnings, hurt by the valuation concerns.

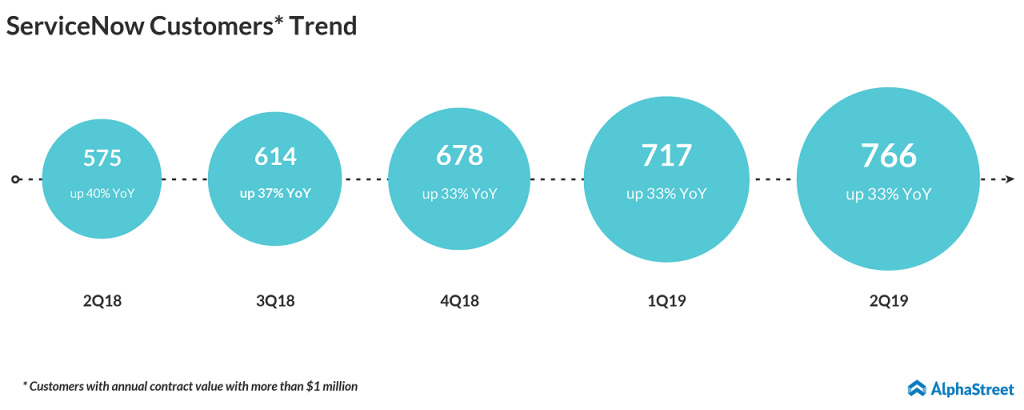

At the end of June 30, 2019, ServiceNow’s customers, with more than $1 million in annual contract value, grew 33% year- over-year to 766.

The company had projected subscription revenue to grow between 32% and 33% for the third quarter and 34% for the full year. Meanwhile, subscription billings are expected to see 26-27% growth in Q3 and 30% growth in 2019.

The continued increase in the number of companies adopting the cloud-based digital workflow solutions and the strategic partnerships like the one with Microsoft (NASDAQ: MSFT) are expected to benefit ServiceNow in the third quarter. However, it’s worth to note that cloud-based software companies’ stocks dropped drastically after Workday (NASDAQ: WDAY)

announced on Wednesday that its human capital management software is expected to end the year with a weaker-than-expected growth.

ServiceNow’s peers Okta Inc (NASDAQ: OKTA), Splunk (NASDAQ: SPLK) and Atlassian (NASDAQ: TEAM), all traded in the negative territory during the past three days. Even though Atlassian’s Q1 financial results topped the market’s views, its stock felt the heat and dropped after its earnings announcement. The iShares Expanded Tech-Software Sector ETF has dropped 5% from last Wednesday.

On October 16, Morgan Stanley downgraded ServiceNow’s rating to Equal Weight from Overweight. NOW stock, which declined 11% since Wednesday, has rallied 36% since the beginning of 2019 and 31% from this time last year.