While the technology sector is riding the wave of the COVID-driven digitalization spree, some players like Slack Technologies (NYSE: WORK) are facing the market’s ire for their mediocre performance. Shares of the corporate communications app nosedived this week though it reported better-than-expected results for the most recent quarter.

The tech firm lagged behind some of its competitors this year, despite a year-over-year growth that is attributable to the widespread adoption of online tools for corporate communication during the COVID days. Meanwhile, the relevance of Slack’s platform in the changed scenario is evident from the faster customer addition, marked by double-digit growth in the number of paid users.

Related: A visual dashboard of Facebook’s Q2 earnings

“The pandemic has obviously had both positive and negative effects on our business. We believe the positive changes will have a greater impact and will persist as part of a permanent structural shift in the way that we work. On the other hand, the negative effects will dissipate as we emerge from the pandemic and related economic uncertainty,” said CEO Stewart Butterfield during his interaction with analysts this week.

Connect Channel

The company is counting on the positive response to its cross-organization communication channel Connect, which is considered a better alternative to email. Analysts look optimistic about the shift in the business model and the company’s ability to create shareholder value. The bullish target price shows that those who invest in the stock now would not be disappointed. Taking a cue from the stock’s lackluster performance in the past, some experts caution about the underlying risk.

Not surprisingly, Slack is in the process of tweaking its strategy to better align the business with the new work atmosphere in the corporate world, after enhancing customers’ self-serve experience by incorporating innovative features into the platform. A few weeks ago, the company ventured into the corporate directory business through the acquisition of start-up Rimeto. Such moves assume importance considering the stiff competition the platform is facing from Microsoft’s (MSFT) Teams app.

Customer Base

The ongoing efforts to convert normal customers into paid customers have been effective so far — mainly through a 90-day trial for teams joining the existing paid customers — and the trend is expected to continue. That, along with the aggressive go-to-market initiatives, should drive the recovery once enterprises resume investing in digital assets.

Nevertheless, the growth initiatives, including investments in innovations like Connect, might not translate into profit and shareholder value in the near term. The management said it sees macro-related challenges in the installed base. Another area of concern is the relatively high churn rate, probably due to the spending cuts practiced by enterprises in the wake of the virus-related uncertainty.

Impressive Show

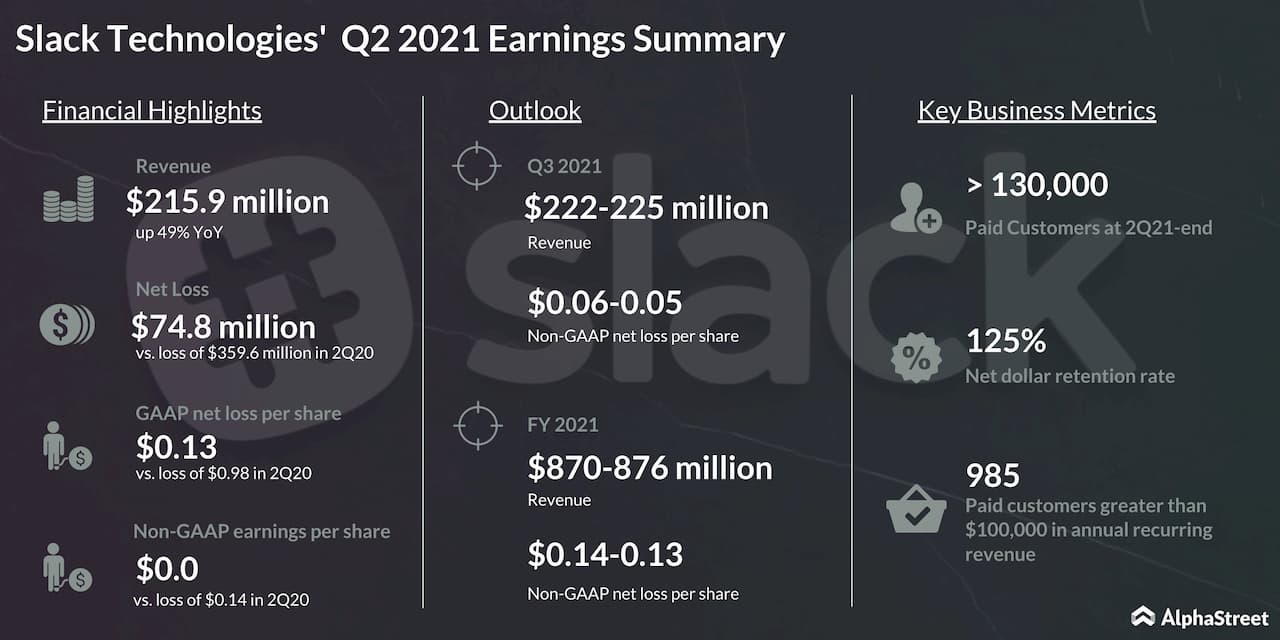

For the July quarter, Slack reported break-even earnings aided by a 49% increase in revenues to $216 million, which is in line with the growth rate recorded in the previous two quarters. It had more than 130,000 paid customers at the end of the second quarter, with a net dollar retention rate of 125%. The results also beat the market’s estimates.

The core product experience improves every quarter, with a particular emphasis on simplifying and removing friction from the process of creating or joining a new team. Our focus in this area has delivered results. Small changes create minor compounding tailwinds. We continue to invest here and expect Slack to get better and more obvious for new teams each quarter, driving increased yield from our self-service funnel.

ADVERTISEMENTStewart Butterfield, chief executive officer of Slack Technologies

Also read: Slack Technologies Q2 Earnings Transcript

Slack’s shares have witnessed significant volatility since last year’s unimpressive IPO, all along maintaining the downtrend. They suffered a fresh blow after the second-quarter report. At slightly above $25, the stock traded down 14% in the early hours of Wednesday’s session. In the past twelve months, it gained about 3%.