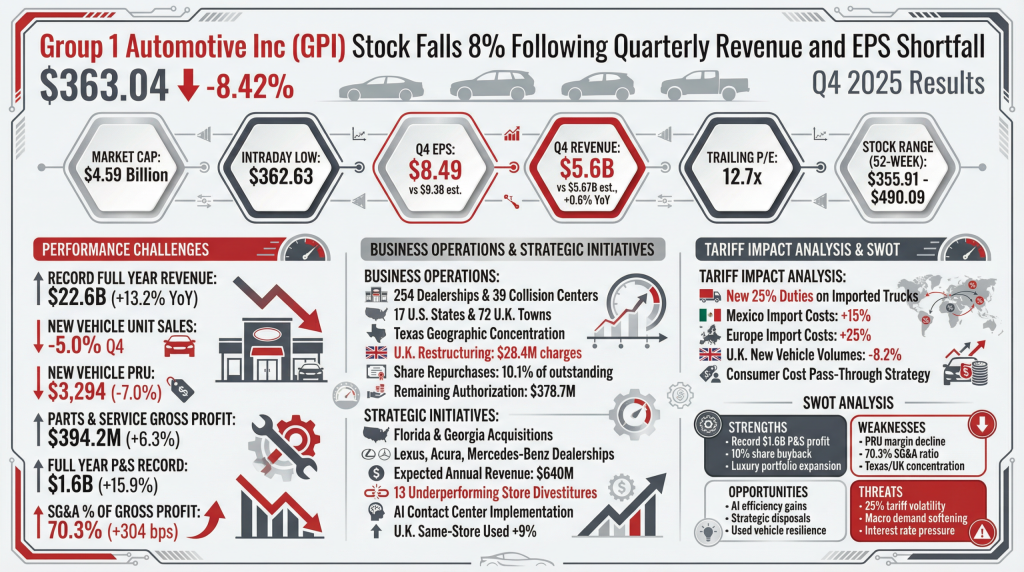

Strengths

- Record Parts & Service Growth: Record $1.6 billion full-year gross profit in high-margin aftersales provides a stable earnings cushion.

- Aggressive Capital Return: Repurchased 10% of shares in 2025, enhancing EPS support despite net income pressure.

- Diversified Luxury Portfolio: Recent acquisitions of Lexus and Mercedes-Benz dealerships strengthen presence in resilient high-income markets.

Weaknesses

- Margin Normalization: New vehicle PRUs are declining from pandemic-era peaks, impacting retail profitability.

- Rising SG&A: Expenses as a percentage of gross profit increased to 70.3%, signaling higher operational friction.

- Regional Concentration: Heavy exposure to Texas and the U.K. increases vulnerability to localized economic downturns.

Opportunities

- AI Implementation: Deployment of AI for customer contact center consolidation and accounting is expected to drive long-term SG&A efficiency.

- Strategic Disposals: Divestment of 13 underperforming stores allows for capital reallocation to higher-margin growth markets.

- Used Vehicle Resilience: U.K. same-store used vehicle revenues rose 9% in local currency, showing counter-cyclical strength.

Threats

- Tariff Volatility: Imposition of 25% duties on imported vehicles and parts poses a direct threat to gross margins and consumer demand.

- Macro-Economic Softening: Softening demand for new vehicles could lead to further volume declines in 2026.

- Interest Rate Pressure: High rates continue to impact floorplan financing costs and consumer affordability for retail auto loans.