Health insurance companies have been witnessing a decline in claims lately as non-urgent medical procedures are being deferred due to high inflation and pressure on personal finances. UnitedHealth Group (NYSE: UNH), a market leader in health insurance, is on a mission to provide comprehensive healthcare services through continued diversification. Government-supported health insurance plans have been a key growth driver for the company.

UnitedHealth’s financial performance in the early months of 2023 was strong, marked by positive data across the broad. But the results failed to impress the market, and the stock experienced weakness following the announcement last week. It looks like the market was expecting a bigger raise in full-year earnings guidance.

Investing in UNH

While the stock is relatively expensive, the recent dip has made it more affordable. It can be seen as a good entry point, considering the healthcare behemoth’s steady growth and experts’ bullish outlook on its future prospects. Currently trading slightly below its long-term average, the stock is likely to cross the $600 mark in the coming months. It is a relatively safe investment that would find many takers, if the recessionary fears persist prompting investors to look for less risky options.

Going forward, there will be a continued increase in the adoption of Medicare Advantage plans as more people retire. It is worth noting that health insurance plans like Medicare account for more than one-third of the company’s insurance business. At the same time, the Optum patient care division is expected to serve more than four million patients in fully accountable value-based care arrangements, which is nearly double that of the 2021 number.

Strong Numbers

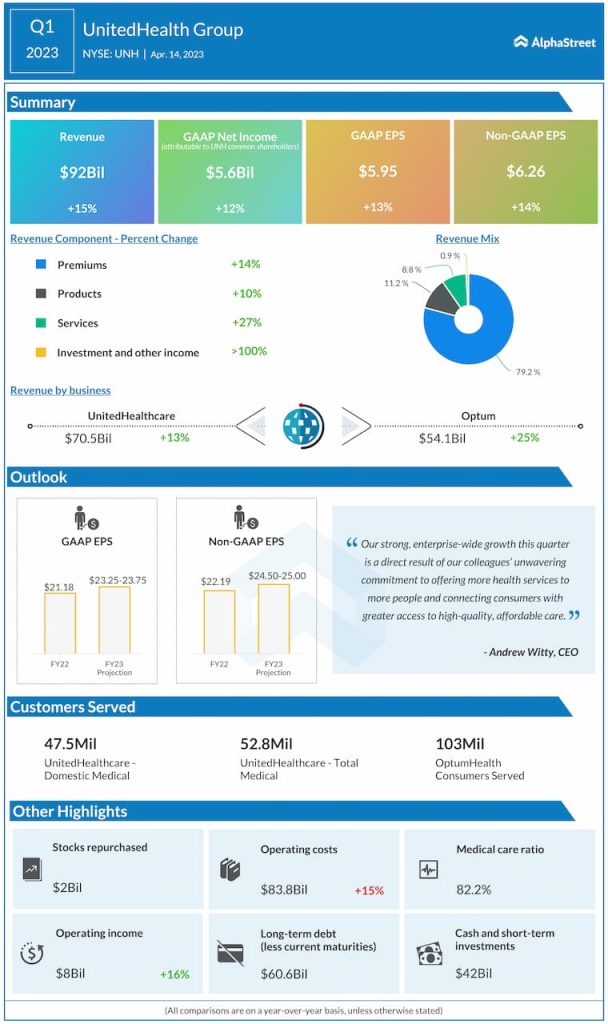

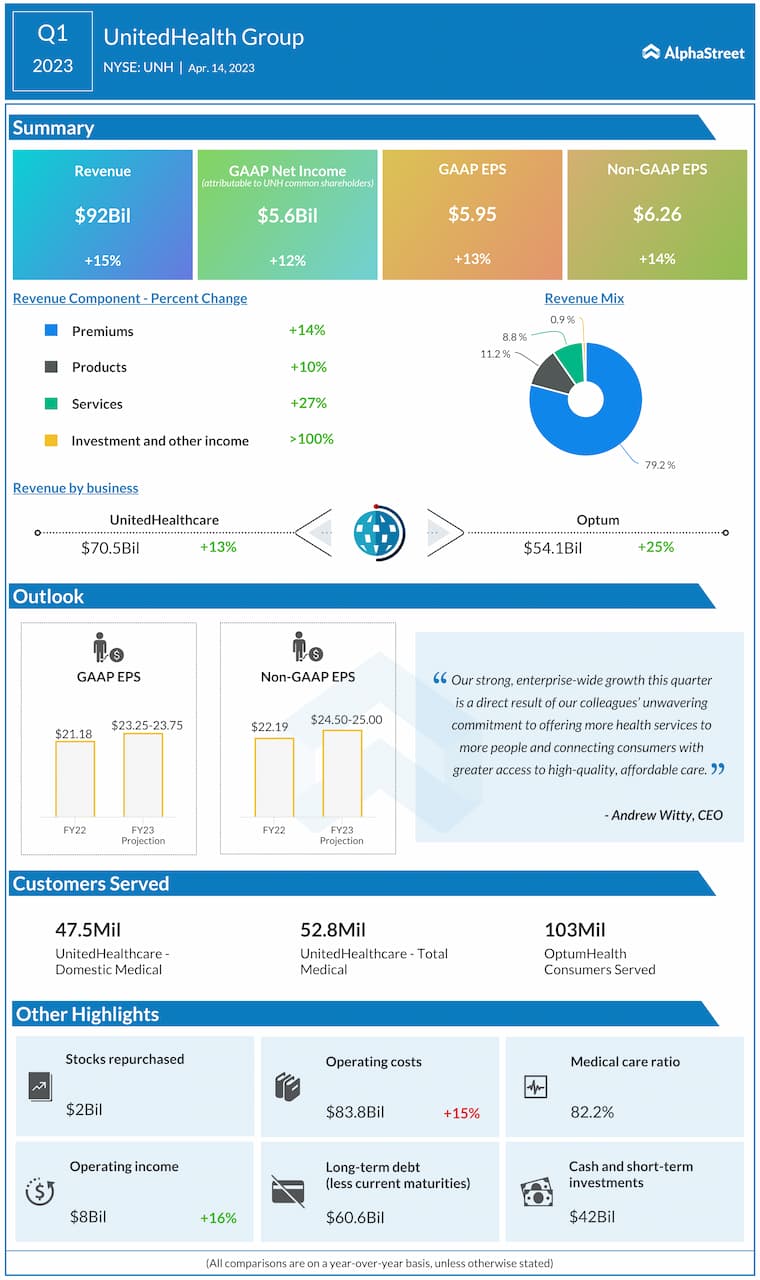

In the first quarter of 2023, both the UnitedHealth division and the Optum business expanded in double digits. That, combined with continued strong growth in the core Premiums segment, led to a 15% growth in total revenues to $92 billion, which also topped expectations. Net profit, adjusted for special items, advanced 14% annually to a record high of $6.26 per share. Over the years, the company has constantly impressed its stakeholders by delivering stronger-than-expected quarterly profit, and the trend continued in the first quarter.

From UnitedHealth’s Q1 2023 earnings call:

“Over the past year, we focused on improving the consumer experience across our company. This consumer orientation is foundational in support of each of our growth priorities, including our approach to value-based care. For example, this year we expect to serve more than 4 million patients in fully accountable, value-based care arrangements through Optum, about double where we were at the end of 2021. These patients will be members of UnitedHealthcare benefit plans or one of the many other plans served by Optum.”

Outlook

The company ended the quarter with an impressive cash flow of $16.3 billion and expects to maintain a strong cash position. Taking a cue from the encouraging business backdrop, the management raised its full-year outlook for adjusted net earnings to $24.50–$25.00 per share, with an estimated growth in Medicare memberships boosting the bottom line. Shares of UnitedHealth mostly traded sideways this year, before gaining strength ahead of last week’s earnings. But it changed course after the announcement and traded lower on Monday afternoon.