AlphaStreet Newsdesk powered by AlphaStreet Intelligence

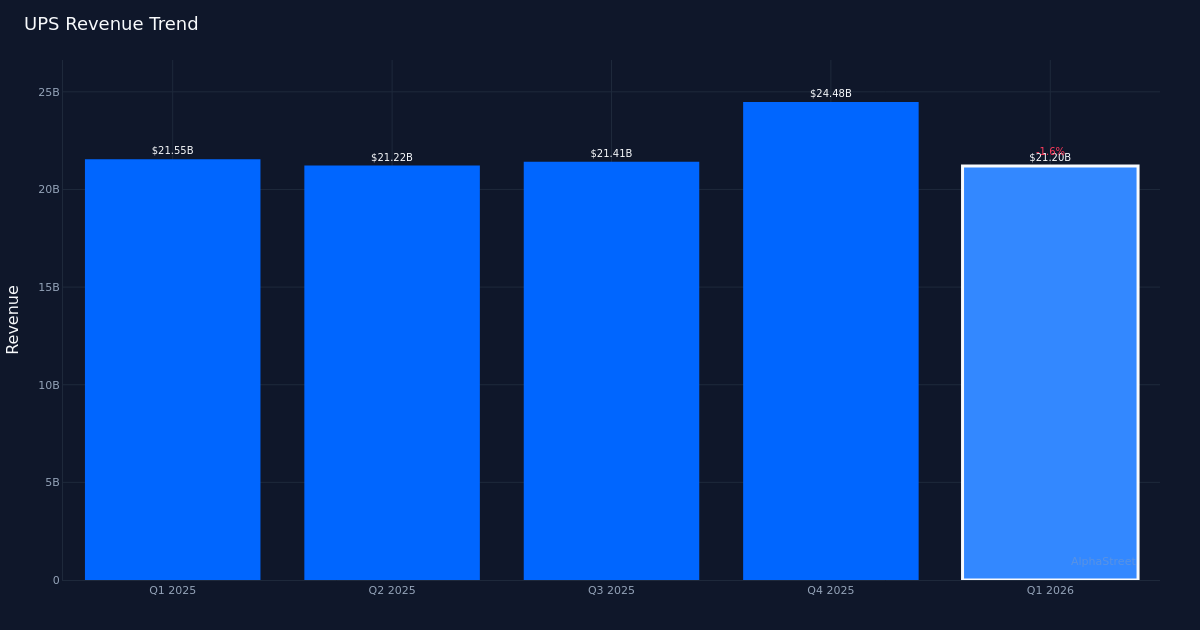

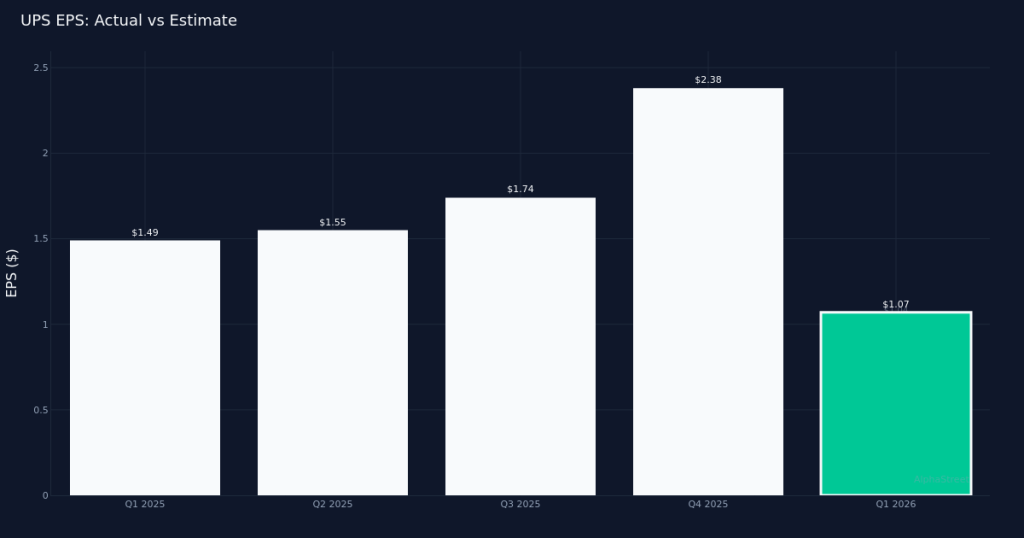

Narrow beat delivered. United Parcel Service, Inc. (NYSE:UPS) reported Q1 2026 non-GAAP adjusted earnings of $1.07 per share, topping the $1.04 consensus estimate by 2.9%. Revenue totaled $21.20B for the quarter, representing a 2.1% decrease from the $21.65B recorded in Q1 2025. Bottom-line profit came in at $906.0M as the integrated freight and logistics provider navigated a challenging volume environment while maintaining pricing discipline.

Quality of results. The earnings beat came amid a top-line contraction, suggesting margin improvement drove outperformance rather than robust demand growth. However, revenue per piece climbed 6.5% for the quarter, indicating UPS successfully extracted higher yields from its existing customer base. This pricing power reflects the company’s strategic shift toward more profitable shipments and disciplined capacity management, though the sustainability of such gains warrants scrutiny as competitive dynamics evolve in the parcel delivery market.

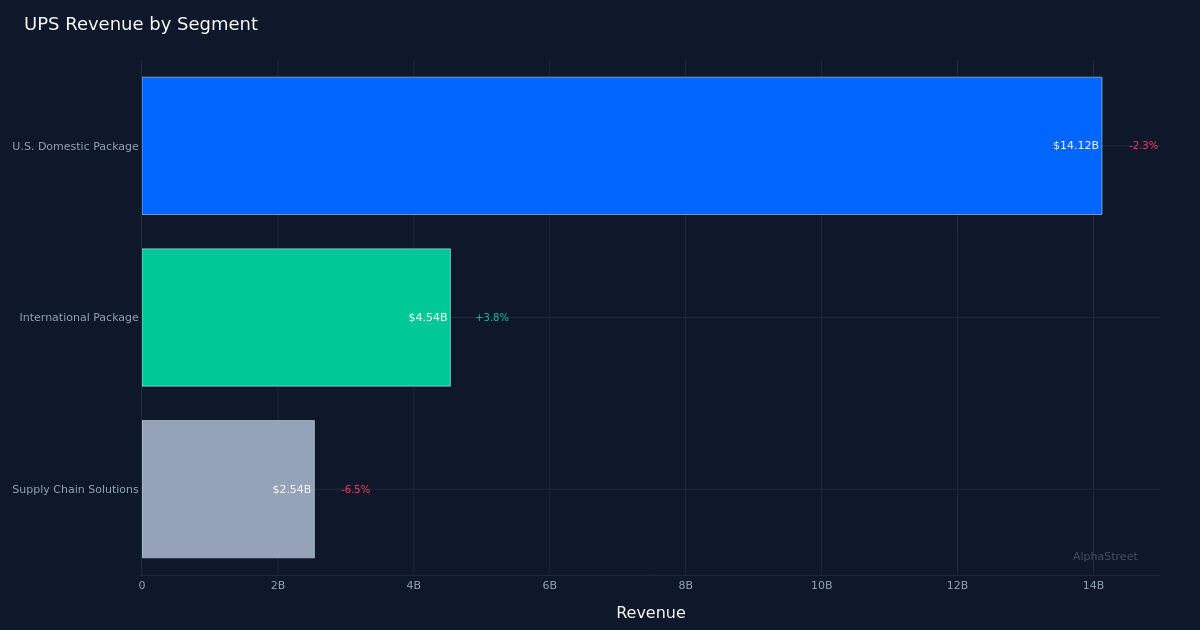

Segment performance mixed. U.S. Domestic Package led with $14.12B in revenue, though the segment declined 2.3% year-over-year. The domestic weakness underscores ongoing volume pressures as e-commerce growth rates normalize and businesses optimize shipping networks. The ability to maintain pricing strength in the face of volume headwinds demonstrates UPS’s service differentiation, but the segment’s trajectory remains critical given its outsized contribution to total revenue.

Full-year outlook established. Management set full-year revenue guidance at $89.70B, providing a specific target rather than a range. This figure implies roughly flat performance relative to run-rate trends if quarterly patterns hold. The precision of the guidance—typically companies offer ranges—suggests confidence in visibility, though it leaves limited room for upside surprise. Investors will scrutinize whether this reflects conservative planning or genuine demand ceiling concerns in the freight and logistics sector.

Market reaction positive. Shares rose 1.1% to $108.24 following the release, indicating investors viewed the earnings beat and pricing momentum favorably despite revenue decline. The modest gain suggests measured optimism rather than enthusiasm, appropriate given the mixed fundamentals. Wall Street consensus stands at 9 buy, 14 hold, and 4 sell ratings, reflecting a generally neutral stance on the stock as analysts weigh operational improvements against macro headwinds.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.