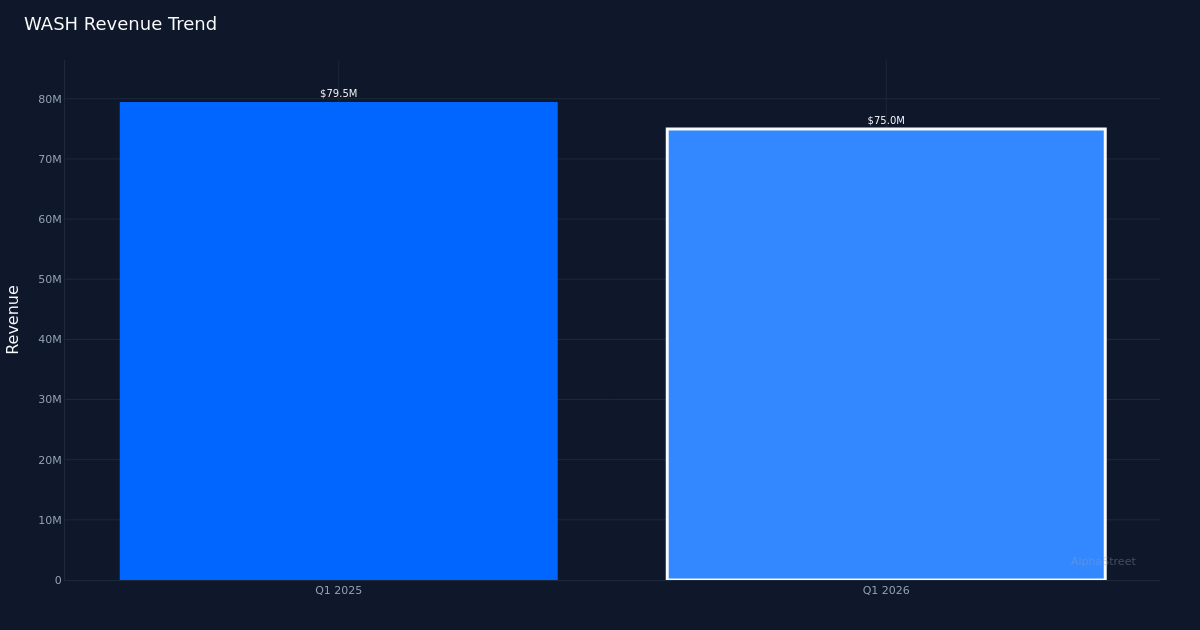

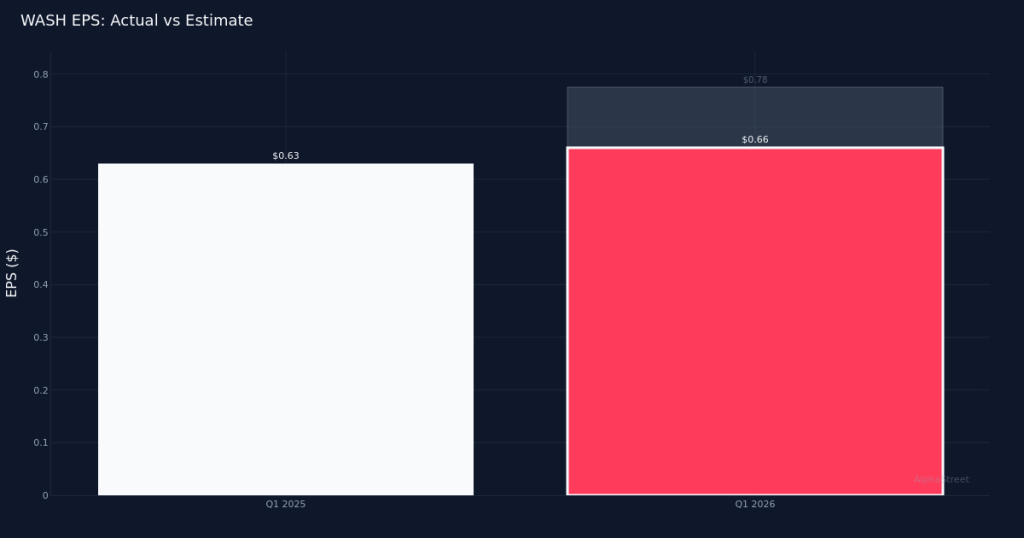

Earnings Miss. Washington Trust Bancorp, Inc. (NASDAQ: WASH) reported Q1 2026 diluted earnings per common share of $0.66, falling short of the $0.78 consensus estimate by 15.4%. The regional bank generated $75.0M in revenue for the quarter, down 5.6% from $79.5M in Q1 2025, reflecting persistent pressure on the company’s core lending operations. Net income totaled $12.6M for the period as the bank navigated a challenging rate environment.

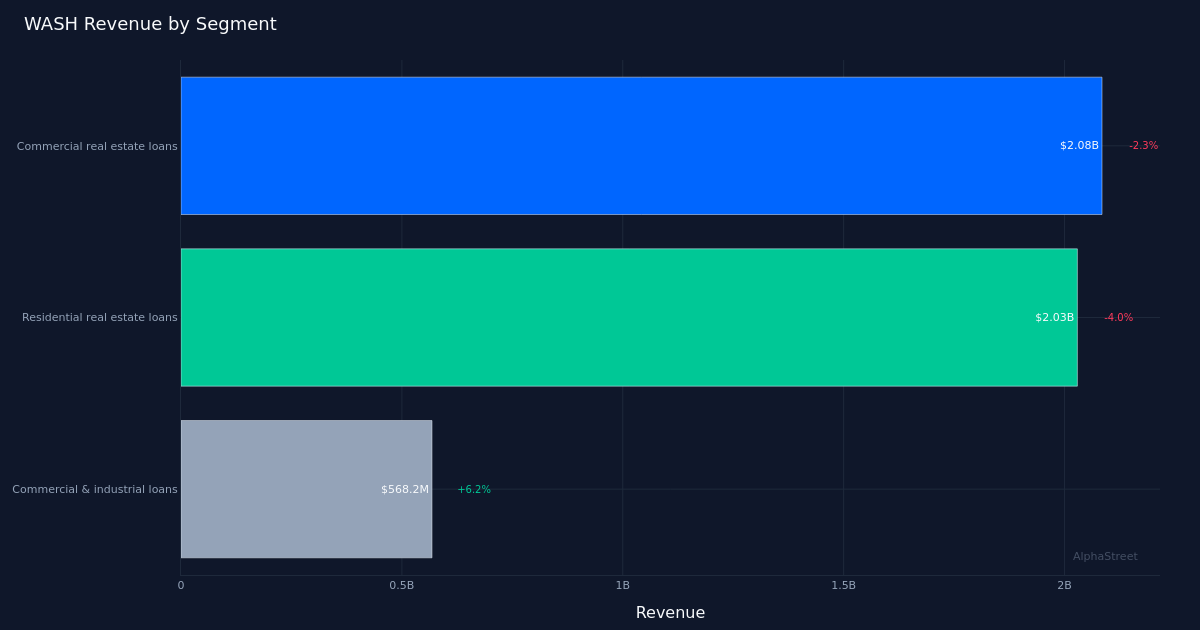

Revenue Headwinds. The top-line contraction underscores the headwinds facing Washington Trust’s loan portfolio, with commercial real estate loans—the company’s leading segment—generating $2.08B in revenue but declining 2.3% year-over-year. Net interest income, a critical metric for assessing a bank’s core profitability, came in at $40.5M for the quarter. The bank operated $5B total loans at quarter end, though the year-over-year revenue decline suggests pricing pressure or portfolio mix challenges are outweighing volume growth.

Quality Concerns. This miss appears fundamentally revenue-driven rather than driven by expense overruns, which arguably makes it more concerning for investors evaluating the bank’s competitive positioning. When a regional bank misses on shrinking revenues, it signals potential market share losses or structural margin compression that management cannot easily remedy through operational efficiency. The 5.6% year-over-year revenue decline paired with the commercial real estate segment weakness suggests the bank is facing pressure in its core commercial lending franchise, which typically drives profitability for regional institutions.

Muted Market Response. Shares traded largely unchanged following the earnings release, suggesting investors may have already priced in operational challenges facing regional banks amid a complex interest rate backdrop. The lack of a sharp sell-off could indicate that the Street views current challenges as industry-wide rather than company-specific, or that valuation had already adjusted downward in anticipation of a difficult quarter.

Analyst Positioning. Wall Street consensus stands at 4 buy, 4 hold, and 0 sell ratings, reflecting a balanced but cautious view on the bank’s prospects. The evenly split recommendations suggest analysts are divided on whether Washington Trust can accelerate revenue growth and return to earnings expansion, or whether regional headwinds will continue pressuring results in coming quarters.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.